The latest figures from Spain’s notaries reveal that foreign demand for property in Spain held up in the first half of 2025, even as locals surged back into the market.

A total of 71,155 home purchases involved a foreign buyer, up 2.5% on the same period last year and 26.5% above the ten-year average. Over five years, foreign demand has more than doubled. Meanwhile, local buyers increased their purchases by 10%, to almost 300,000 homes, lifting domestic demand to its highest level since before the pandemic.

As a result, the foreign share of the housing market slipped slightly to 19.3% (from 20.4% a year earlier), still comfortably within its ten-year range but now trending lower as the home market strengthens.

Biggest markets: steady at the top

The UK remained the largest foreign market with 5,731 purchases, followed by Germany (4,756), Italy (4,513), and France (3,980). Together, these four countries accounted for roughly one-third of all foreign sales.

Winners and losers

Portugal led the growth chart with a remarkable +24% year-on-year increase, followed by the Netherlands (+19%) and the USA (+15%), all posting double-digit gains. These reflect both lifestyle migration and the strength of their currencies against the euro.

At the other end of the table, demand from Russia (-17%), Poland (-11%), and Argentina (-7%) fell sharply, continuing a multi-year retreat. The once-mighty Belgian market also slipped (-5.5%), while Scandinavian demand softened slightly as affordability and currency pressures bit.

The takeaway

Foreign demand remains historically strong, but its share of Spain’s housing market is being diluted by a domestic rebound. The data suggest a maturing post-pandemic cycle: international interest remains broad, yet cooling in some traditional source markets as others — notably Portugal, the Netherlands and the US — pick up the slack.

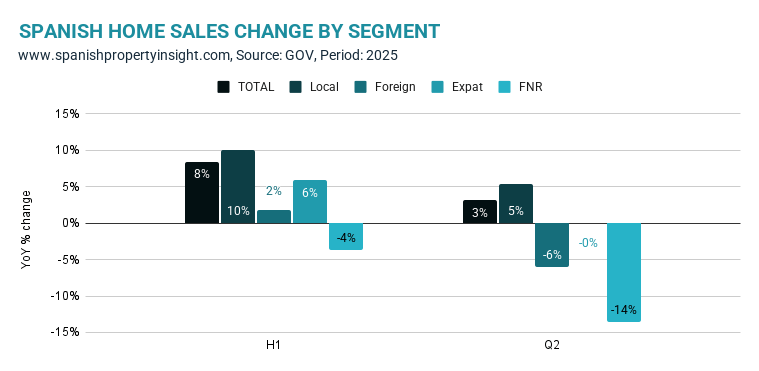

A closer look at the timing

It’s also worth noting that these notary figures cover the first half of the year. Recent data from the Housing Ministry, which provides a quarterly breakdown, paints a less upbeat picture (see chart below). While foreign demand was marginally higher in the first six months as a whole (like the notary figures), the second quarter saw a notable downturn — led by a 14% drop in purchases by foreign non-resident second-home buyers. Put simply, the notary report stops just short of showing a downturn that took hold in the second quarter — meaning the apparent strength in H1 masks a softer trend beneath the surface.

Want to know more about this market?

Do you want to get the full picture? See SPI’s in-depth reports on key international markets and buyer segments in Spain’s property market to know what’s really going on.