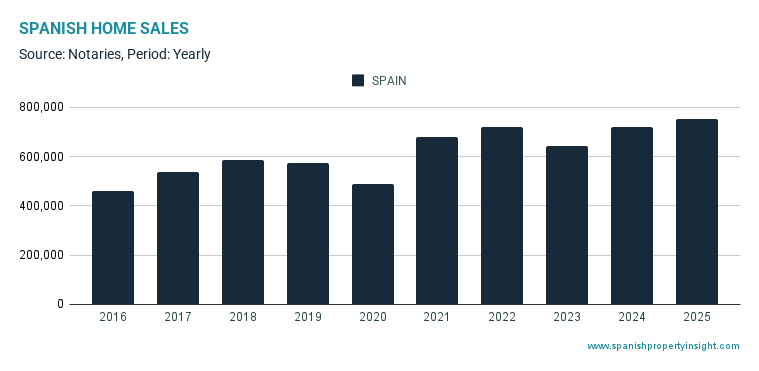

Spain’s housing market had a remarkably strong year in 2025, with sales reaching their highest level since the boom years before the financial crisis. Prices also pushed above the previous peak in nominal terms, though in real terms the market still has some way to go.

According to the latest figures from the Notaries Association, there were 752,661 home sales in Spain in 2025, up 4% on the previous year and the highest level recorded since 2007, at the peak of the last real estate boom.

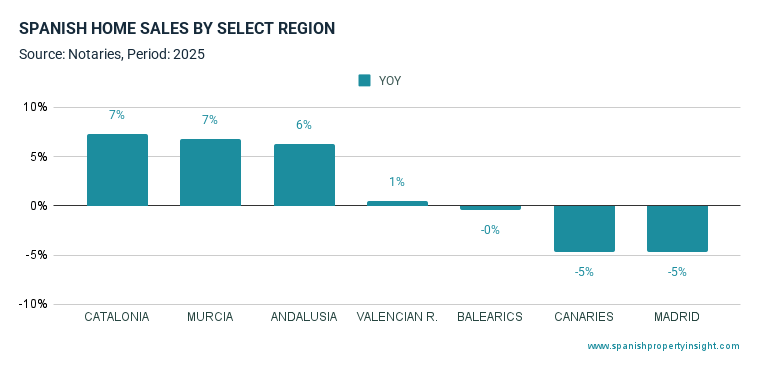

Demand was strong across much of the country, particularly in regions popular with foreign buyers. Catalonia and Murcia both recorded sales growth of 7%, followed by Andalusia at 6%. The Valencian Region saw more modest growth of 1%, whilst activity declined slightly in some areas, including Madrid and the Canary Islands.

The headline figure puts the Spanish market close to the levels last seen during the property bubble of the mid-2000s, though the structure of demand today is very different.

Prices break past the old peak – at least on paper

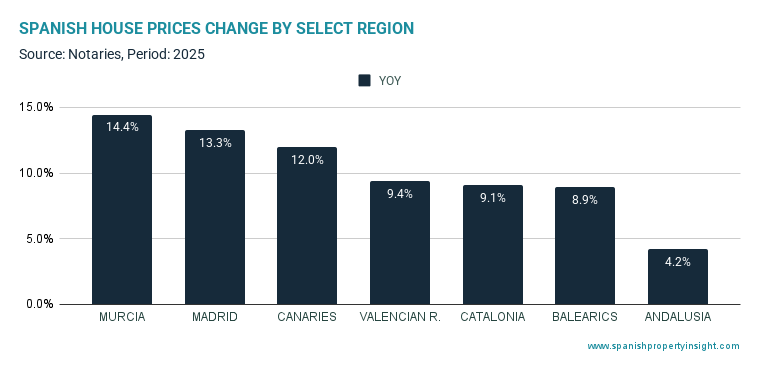

Prices also continued to rise strongly in 2025. The national average reached €1,902 per square metre, an increase of 7.5% year on year.

This means prices have finally surpassed the previous nominal peak of €1,790 per square metre reached in 2007. However, inflation over the intervening years means that, in real terms, the market is still below the previous high.

Adjusted for inflation, the current average price of €1,902 per square metre is roughly equivalent to about €1,430 in 2007 euros. That puts today’s market still around 20% below the real peak reached during the bubble.

Regional price growth varied widely. Murcia led the country with a 14.4% increase, followed by Madrid and the Canary Islands with double-digit growth.

Strong demand but a different type of boom

Taken together, the figures show a market in robust health. Sales are at their highest level in 18 years and prices are rising steadily.

Demand is being driven by several structural factors. Spain’s population is growing rapidly thanks to immigration, echoing one of the drivers of the previous boom. Foreign demand is also at record levels, while domestic demand remains strong.

Lending conditions have also been supportive. Although interest rates are higher than the ultra-low levels of the previous decade, the average Euribor 12-month rate was still only 2.223% in 2025.

Crucially, however, mortgage lending today is far more conservative than during the bubble years. This is not a credit-fuelled boom driven by reckless lending, but rather a market supported by solid underlying demand.

Another factor pushing people towards buying is the shortage of rental housing in major cities. Rent controls and other government interventions have significantly reduced supply in the formal rental market, leaving many households with little choice but to buy if they can possibly afford it.

What happens in 2026?

Looking ahead, demand is likely to remain robust. Spain continues to encourage immigration and there is no immediate reason to expect a sharp tightening of credit conditions.

However, it may be difficult for prices to continue rising at the recent pace. At some point buyers will be priced out, especially given that much of Spain’s housing stock is ageing and requires investment to upgrade. There are already early signs that the market may be cooling. Preliminary data from the Land Registrars indicate that home sales fell by around 7% year-on-year in January, the sharpest drop since June 2024.

The biggest structural constraint remains supply. The pipeline of new homes is limited, and government regulations, planning delays, taxes, and bureaucracy continue to hold back construction.

For that reason, the most plausible scenario for 2026 is a moderation in the pace of the market rather than a downturn. Sales may cool as buyers react to higher prices and limited supply, but there are currently no obvious signs of the kind of imbalance that preceded the last crash.