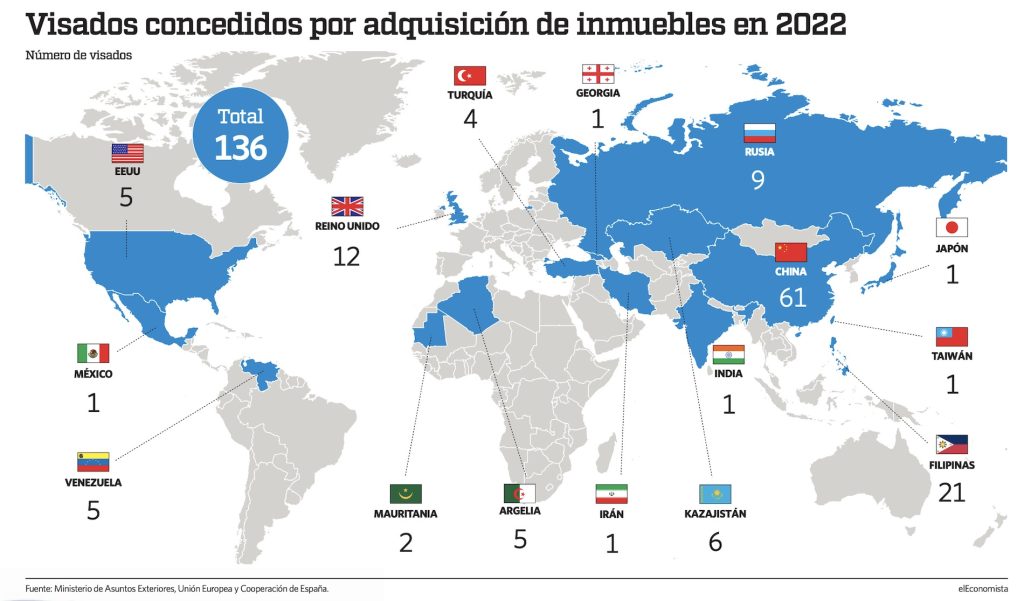

The notaries have just published their report on foreign demand for property in Spain in the second-half of 2022, confirming data from the land registrars showing that last year was a record year for foreign investors. Now that all the data is in for 2022, this kicks of a series of articles analysing the foreign segment in depth for anyone with an interest in the market.

Introduction to this report

The Spanish notaries’ association (Consejo General del Notariado) have just published their latest half-yearly report on foreign demand for property in Spain covering the second-half of 2022, which gives a full-year picture when combined with the H1 2022 report, and can be compared to figures from the land registrars’ association (Colegio de Registradores).

This article will use data from these sources to build a picture of overall foreign demand for property in Spain in 2022, the trend in preceding years, the breakdown between expat and second-home demand, and the change in the foreign market share (FMS). In subsequent articles we’ll look at demand per country, spending per market, purchases by region, and the headwinds and tailwinds helping and hindering foreign demand, before wrapping up with conclusions and what we might expect from 2023.

Overview of Foreign demand in 2022

The latest data from the notaries reveals there were 143,629 Spanish home sales involving a foreign buyer last year, up 29% on 2021, and the biggest number on record, as illustrated by the next chart showing yearly sales to foreign buyers according to both the notaries and the registrars, with a significant difference between the two sources (94,482 sales according to the registrars, up 55% year-on-year) but both showing 2022 as the best year on record by a wide margin. So the data is unequivocal: 2022 was a boom year for Spanish real estate sales to foreigners, almost 50% higher than 2019, up 150% in 10 years, and more than double the last boom-time peak of 2007.

However, looking at sales last year on a half-yearly or quarterly basis, illustrated in the next two charts showing, on the left, quarterly sales from the registrars, and on the right, the annualised change in half-yearly sales, there are clear signs of demand growth running out of steam. If the trend taking shape in the second-half of last year continues this year, foreign demand will continue to cool in the first half of 2023, and even start contracting (having gone from +54% in H1 to +10% in H2 2022).

Expats vs. foreign non-residents (FNR)

The notaries publish data breaking down foreign demand into residents and foreign non-residents (FNR). The resident market includes expats from rich countries like the UK, France and Germany, and economic migrants from poor and middle-income countries like Morocco, Ecuador and Romania, buying in very different segments. The FNR market is almost all from rich countries buying second-homes and investments.

In recent years the expat market has been bigger (around 60% in 2019 and 2020) but the FNR market has been growing faster such that last year FNR demand increased to 45% of the foreign market, whilst expat demand fell to 55% of the market. FNR demand grew by 44% last year, compared to 18% growth in expat demand. The next two charts show overall demand broken down by type, and annual growth for each type. The key point here is that the stellar growth in foreign demand last year was mainly driven by FNRs (buying second-homes) not expats.

Foreign market share (FMS)

As local (Spanish) demand only increased by 1.8% last year whilst foreign demand increased by 29%, the market share of foreign buyers increase to a record high of 21% of the Spanish property market. In other words, just over one in five buyers of Spanish homes last year came from abroad, and injected much needed foreign capital into the Spanish economy.

The FMS was as high as 43% in the Balearics and 38% in the Canaries, causing resentment in some quarters. Growing resentment exploited by political parties is one of the factors that could influence the evolution of foreign demand this year and moving forward, and will be considered in the headwinds / tailwinds analisis to come. There are signs that that the Balearic government’s efforts to discourage foreign investors are already starting to bear fruit, with foreign demand down 14% in H2 last year, the only region to see a decline in foreign investment in that period.

Foreign demand vs. local demand

To wrap up this article looking at overall foreign demand for property in Spain last year, this final chart illustrates the comparative fortunes of local and foreign demand since the real estate crash of 2007. Whilst local demand has still not recovered to where it was that year (35% below) foreign demand has more than doubled.

All articles in this series

Subscribe for Insight

Buying and owning property in Spain is a big decision—don’t go in blind. SPI provides premium content you can trust: exclusive reports, expert guides, and our Data Hub. Subscribe now for access to exclusive content to help you make confident, well-informed choices in the Spanish property market.