Summary of the Spanish mortgage market in the second quarter of 2019 – interest rates, mortgage costs, and mortgage market lending volumes in Spain.

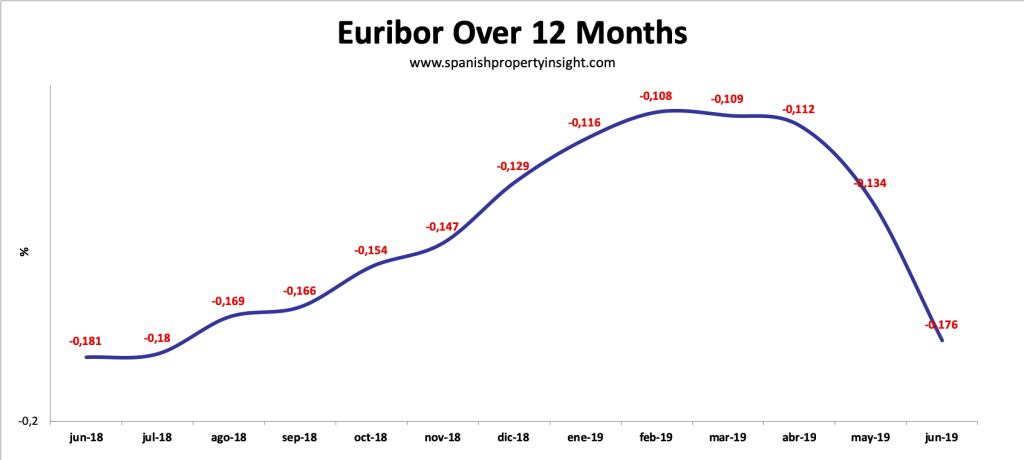

12-month Euribor, the base rate used to calculate interest payments on most mortgages in Spain, came in at -0.176 on average in June, almost the same as it was a year ago, but more than 30% down in a month as Euribor nosedived 67 basis points in the second quarter of the year.

As a result, borrowers in Spain with annually resetting Spanish mortgages will see their repayments rise by around €0.26 per month for a typical €120,000 loan with a 20 year term.

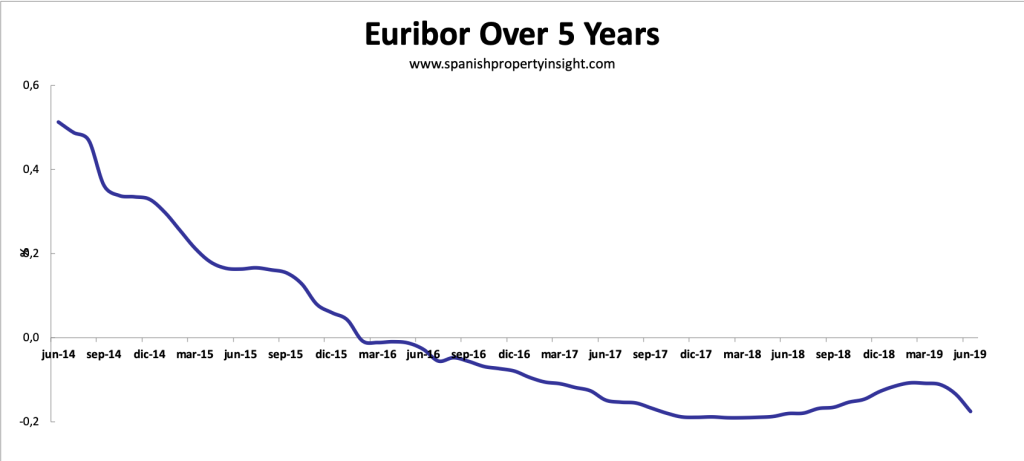

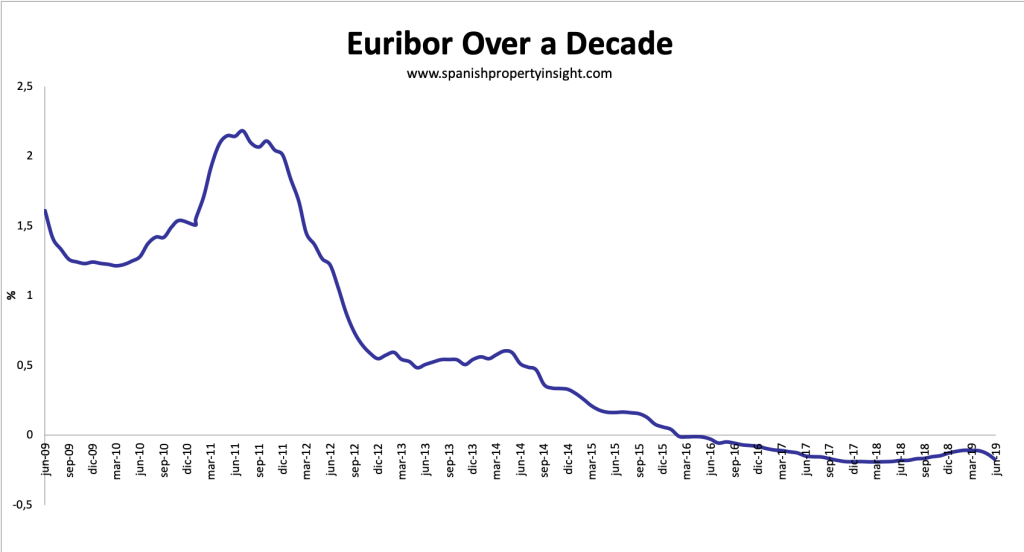

Euribor has now been in negative territory since February 2016 as a result of the ECB’s loose monetary policy intended to keep the wheels from spinning off the Eurozone economy.

Euribor began to creep higher last year as central banks in the West tentatively signaled the end of a long period of loose monetary policy started in response to the financial crisis and great recession. But that trend came to an abrupt end this year, with Euribor falling in each of the last four months, and plunging 31% in May alone.

Why the sudden reversal? “The prolonged presence of uncertainties related to geopolitical factors, the rising threat of protectionism and vulnerabilities in emerging markets is leaving its mark on economic sentiment,” said Mario Draghi, Governor of the European Central Bank.

Draghi didn’t mention that in the US, President Trump has been badgering the Fed for months to reduce interest rates, and seems to be getting his way. Where the US goes, the rest will follow. You could argue that Trump has managed to lower interest rates globally, because it suits him to do so, and that’s all he cares about. The institutional damage he is wrecking is profound.

Mortgage lending volumes in April 2019

Provisional data from Spain’s Notaries Association shows new residential loans up 5.1% to 24,228 signings with an average value of €135,084, down 1.1%.

The left-hand chart below shows how mortgage lending has been growing since 2014 but is still around 75% below what it was in 2007. And the chart on the right shows how LTVs have fallen to around 74%, whilst close to 50% of buyers now use a mortgage, up from 30% in 2013. These charts suggest there is no risk of a credit-fueled housing bubble inflating anytime soon.

Related news: New Spanish mortgage regulations drive up costs for borrowers