This is a website for buyers, owners, and sellers of property in Spain, offering reliable information and resources to help you get things done with confidence. It is run by Mark Stücklin, author of the Spanish Property Doctor Column in The Sunday Times (2005-2008), and the book ‘Need to Know: Buying Property in Spain’ published by Collins.

This is a website for buyers, owners, and sellers of property in Spain, offering reliable information and resources to help you get things done with confidence. It is run by Mark Stücklin, author of the Spanish Property Doctor Column in The Sunday Times (2005-2008), and the book ‘Need to Know: Buying Property in Spain’ published by Collins.

I have written this report to provide you with a snapshot of the current state of the Spanish property market from an independent, non-sales perspective. It starts off with a look at the statistics, which can be a quite dry, but finishes off with some opinionated stuff to make the pulse quicken, so do stick with it.

Latest figures on the Spanish property market

First of all, let’s look at the numbers.

The most widely used housing market statistics for property prices in Spain are the quarterly figures released by the Spanish Ministry of Housing.

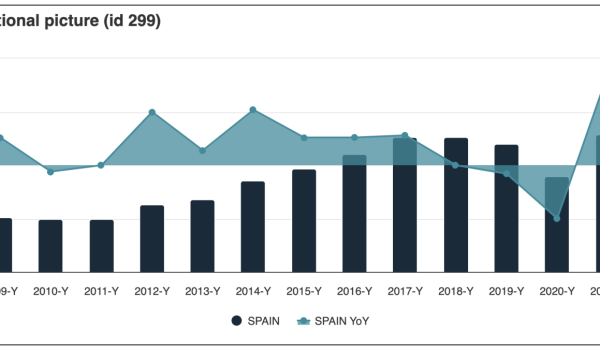

According to the latest figures for the end of the third quarter (Q3), average national Spanish property prices rose by 0.3%, which translates into an annual rise of 5.3%. This is a slowdown compared to Q2, when prices rose by 1.5% for the quarter, and 5.8% over 12 months.

Average Spanish property inflation rates have been steadily falling since a peak of 18.5% in 2003, to 9.8% a year ago, to 5.3% now. The general picture, on a national basis, is of a slow but steady fall in property inflation, which suggests a soft landing for the Spanish property market after a decade-long boom.

The following graph shows the trend of annualised property inflations rates every quarter since the start of the decade (Q100 = Q1 2000).

On a regional basis, the same pattern is being repeated, but with local differences.

The following table shows average property inflation rates, and average property prices in €/m2 for selected provinces and regions at the end of Q3 2007.

| REGION / PROVINCE | PRICE €/M2 | ANNUAL % CHANGE |

| Murica | 1,612 | 10.7% |

| Granada | 1,499 | 9.7% |

| Cordoba | 1,554 | 9.3% |

| Asturias | 1,749 | 8.8% |

| Extremadura | 1,028 | 7.9% |

| Cantabria | 2,089 | 7.5% |

| Cadiz | 1,849 | 7.3% |

| Pontevedra | 1,705 | 7.3% |

| Tarragona | 1,891 | 7.2% |

| Castellon | 1,760 | 7.0% |

| Sevilla | 1,718 | 7.0% |

| Balearics | 2,372 | 6.8% |

| Galicia | 1,511 | 6.7% |

| Andalucia | 1,753 | 6.7% |

| Almeria | 1,629 | 6.6% |

| Canaries | 1,809 | 6.4% |

| Tenerife | 1,744 | 6.4% |

| Las Palmas | 1,862 | 6.2% |

| Girona | 2,136 | 5.6% |

| NATIONAL AV. | 2,061 | 5.3% |

| Valencia | 1,548 | 5.1% |

| Catalonia | 2,395 | 5.1% |

| Barcelona | 2,688 | 4.7% |

| Valencian R. | 1,641 | 4.3% |

| Teruel | 1,007 | 4.3% |

| Malaga | 2,293 | 4.2% |

| Madrid | 3,005 | 3.1% |

| Alicante | 1.731 | 2.1% |

Source: Ministerio de Vivienda

Murcia has done the best over the last 12 months, with 10.7% annualised price growth, and Alicante (Costa Blanca) the worst, with just 2.1% annualised price growth to the end of Q3.

It is interesting to note that Malaga province (Costa del Sol) and Alicante province (Costa Blanca) – the two provinces that traditional attract the most attention from overseas buyers, and that have the highest number of second homes – delivered some of the lowest annual price increases, with 4.2% and 2.1% respectively. Along with Cadiz and Valencia province, Alicante was the only province to register a fall in prices in Q3 compared to Q2. That means prices are falling on the Costa Blanca, even according to the government’s notoriously wonky figures.

Given that the general consumer price inflation rate in Spain is now 3.6%, this means that real capital gains from property in Alicante and Madrid were negative, and only just positive in Malaga.

There is one big problem with these figures, which is that many experts doubt their accuracy. The government’s figures are based on valuations done by certified appraisal companies, primarily for mortgage lenders. Appraisal companies have a powerful incentive to inflate valuations so that the mortgage lenders who pay them can lend more. Therefore the government’s figures probably overstate prices, which is why the Housing Ministry is thinking of stopping publishing figures in future. The present figures may not be very accurate, but at least they give one an idea of price trends, which is better than nothing.

Anyway, back to the market. Figures from other sources confirm the slowdown seen in the Spanish government’s figures.

According to the Spanish real estate portal idealista.com, which publishes quarterly changes in property asking prices in leading Spanish cities, asking prices in Q3 fell in Barcelona by 0.5%, in Madrid by 0.9%, and Valencia by 0.7%. According to asking prices figures from the Spanish property portal Kyero.com, average national asking prices fell by 0.6% in Q3 (though with wide difference between regions and types of property), whilst figures from the portal Fotocasa show prices falling by 1.6% in Q3. Anecdotal evidence suggests that prices falls are much bigger in some popular coastal areas such as the Costa Blanca and the Costa del Sol.

Housing starts

It is important to keep an eye on housing starts because they tell you how much property will be coming onto the market in future. Too much new property can create a glut that drives down prices and destroys wealth.

According to Spain’s college of architects, there were 144,900 planning approvals in Q2, and 361,785 in the first half of the year.

In Q2 planning approvals fell by 33% compared to Q1, and by 37% compared to the previous year (Q2 2006). Some of the most dramatic falls were Andalusia (64%, and 79% in Almeria province), Catalonia (57%), The Canaries (25%), Valencian Region (16%), and Madrid (43%). On the other hand planning approvals increased by 2% in Murcia, and 21% in the Balearics. Planning approvals in Murcia increased by 48% in Q1, but then fell to 2% in Q2, so Murcia had a surge followed by a big fall. The Balearics is the only region with strong growth in planning approvals all year, with 11% in Q1, followed by 21% in Q2.

The ministry of housing also publishes figures on residential construction activity. Whereas the architect’s figures are for planning approvals, not all of which proceed to construction, the ministry of housing figures are for actual housing starts. Looking at these, there have been 286,487 housing starts in first half of year, an 11% fall on last year, and 139,732 housing starts in Q2, a fall of 17% compared to Q2 2006.

So the pattern of falling activity is clear from both sets of data, though the fall is much more dramatic in the architect’s figures than in the government’s figures. Because the architect’s figures record an earlier stage of the process, we can expect them to feed through to the government’s figures in subsequent periods.

The ministry of housing also gives figures on completed properties. There were 297,000 completed properties in the first half of the year, roughly the same as the same period last year, which was a record year. This implies a huge number of newly finished properties coming onto a market that has now gone cold, though not all these properties are for sale, as many will have been bought off plan.

Overall the picture is one of a dramatic fall in housing starts in Q2, as developers respond to the fall in demand, the exception being the Balearics, where housing starts have risen strongly all year. A 20% to 30% fall in housing starts, as implied by these figures, will sooner or later translate into lower economic growth, rising unemployment, and falling consumption, which could create a negative feedback loop for the Spanish property market.

A massive housing overhang in Spain?

In the section above I have discussed the latest figures for housing starts, which show a dramatic fall in activity. These are contrasted with completions, which are still steady, and near record levels (completions reflect housing starts some 12 to 24 months earlier).

Now I would like to draw your attention to a new report from the Centre for European Policy Studies entitled ‘Bubbles in real estate? A Longer-Term Comparative Analysis of Housing Prices in Europe and the US’ by Daniel Gros. This report argues, amongst other things, that there is a massive glut of properties in Spain, and that this will lead to a sharp downturn in residential construction activity. Based on the figures above, it looks like this is beginning to happen.

Rather than paraphrase the report, I am just going to quote the sections that I found most relevant to Spain.

“The experience of Germany and Japan shows that a real estate boom can leave a long-lasting legacy if the boom leads to a housing ‘overhang’, i.e. if simply too many houses are built. Given that buildings depreciate very slowly, a housing overhang can lead to a long-term weakness in construction activity. In Germany, for example, a combination of higher prices and very strong government subsidies led to an extraordinary expansion of the construction sector in the years following unification. At its peak (1995), construction activity amounted to 14.5% of GDP, and over the next ten years it then fell back to a little above 8.5% of GDP.”

Note: for construction investment as % of GDP, Spain is around 18.5%, compared to 8.5% for Germany, and 10.5% for France.

“During 2005, the rate of construction of new dwellings in Spain (over 50 per 1,000 households) was more than six times higher than in Germany (around 8-9 per 1,000).”

“The Spanish value appears to be out of line with any estimate of a steady-state rate of building. Assuming that a typical house (or more realistically an apartment block) lasts 50 years (which corresponds to a depreciation rate of 2%), a rate of construction of new dwellings of 20 per 1,000 households would keep the stock of dwellings constant (per household). The current rate of construction in Germany is much below this measure of what would be a steady state, corresponding to the underinvestment measured above. By contrast, the rate of construction in Spain is almost three times higher than this benchmark value, suggesting that the country is rapidly accumulating a housing overhang.”

“Even if one takes into account the relatively rapid rate of growth of population (and households) in Spain over the last years, which amounted to about 1-1.5% per annum over the last decade, the conclusion would not change. At this rate of population growth, one would expect that in equilibrium (i.e. if this growth were to continue forever) the rate of construction of new dwellings should be 30-35 per 1,000 households,6 much below the current value.”

“A downturn in housing prices might depress consumption somewhat, but not construction investment. By contrast, in Spain and Ireland, construction investment has increased to levels (18-20% of GDP) not seen in any other OECD country except Japan. In these two countries, lower housing prices are likely to be associated with a sharp and prolonged drop in domestic demand. Germany provides the mirror image to these two cases in that construction activity in Germany has now for some time been below average. All in all one can thus conclude that the coming downturn in housing prices should not have a strong impact on the eurozone average, but it is likely to lead

to serious tensions within the area.”

And the conclusion is….

“Spain and Ireland face a massive housing overhang and thus probably a sharp deceleration of construction demand.”

And finally…

This month I haven’t had time to do a proper survey of property professionals such as estate agents, developers and lawyers in different parts of Spain, so I can’t give you much news from the frontline of the market. But based on the conversations I have had with people in the business it is fair to say that the market is tough. It varies from region to region, and some are making a better fist of it than others, but overall it is a struggle. Many agents are going out of business, some high profile developers have hit the wall (more to follow, in my opinion), and the Spanish press has taken to talking about the property ‘crisis’. But at the same time I know of at least one developer having a record year. It just goes to show that with the right product, at the right price, with good marketing, and good service, success is possible even in a difficult market. Part of the problem is that most Spanish developers who would like to sell to overseas buyers haven’t a clue what they are doing.

What is clear across all regions is that buyer behaviour has changed. Buyers today are well informed, doing their research, and not rushing into anything. They are still interested, despite all the bad news about Spain, but realise they can now afford to look around for something that really suits them and represents good value. Most have an idea that the market is adjusting, and some are waiting to see if prices fall in the next year or two before buying.

Some agents complain of increasing numbers of buyers with unrealistic price expectations; clients who have read something, or seen something on the telly about a Spanish property market crash, and come out to Spain with no money assuming that desirable properties are being given away. The market may be tough, but not that tough. Furthermore, quality always has its cost. And the tougher the market gets, the less quality you find as vendors with something good to sell simply withdraw from the market until it improves. A lot of crap has been built recently in Spain, and I expect the price for crap to fall significantly. But if you want good property, the kind of stuff worth buying, then you will still have to pay the price.

So is now a good time to buy? I expect the market to get tougher, maybe a lot tougher, so there is no hurry. If you don’t mind buying some of the rubbish that has been built, then hold on, as prices could fall significantly. But even if you hold on and then buy cheap it still won’t be a good investment because crap is never a winner unless you are in the manure business. But if you want quality property, and you are ready to buy, there I would certainly recommend starting you search now, as buyers will be in a strong position over the next 12 to 24 months. If you want to buy on a new development, then be sure to deal only with reputable and solvent companies. They are the ones that will flourish in this market, whilst the rest cut costs, cut corners, or even go under.

There will be much wailing and gnashing of teeth, but a downturn is exactly what the doctor ordered for the Spanish property market. In my opinion the boom has been more of a bane than a boon for Spain.

Why? Because during the boom:

- anyone could make money regardless of quality or honesty

- some of the most undeserving people made fortunes misselling rubbish (some who have diversified into ‘emerging markets’ continue to do so),

- cowboys took over

- developers had no incentive to understand their clients or differentiate their product

- the Spanish coast was turned into a wall of cement resembling one big NCP car park

- town hall corruption took root

- the Spanish economy turned into a real estate junkie.

It’s time for some cold turkey, but the Spanish property market should emerge healthier and stronger for it.

© Mark Stucklin (Spanish Property Insight)

SPI Member Comments

Facebook Comments