Reports and updates on the Spanish mortgage market.

This report page gives you the latest data and analysis of the performance of the Spanish mortgage market in the latest year or half-year. If reports are available for previous periods you will see them listed in the tabs below. The latest report on the Spanish mortgage market will be featured in the first tab.

This report on the Spanish mortgage market is based on public data from sources such as the General Council of Notaries, the Bank of Spain (BoS) and the National Institute of Statistics (INE).

2025 H1

Spanish mortgage market report H1 2025

Overview

The Spanish mortgage market strengthened in the first half of 2025, with rising lending activity and moderating interest rates providing improved conditions for borrowers. Lending volumes increased meaningfully compared to last year and to long-term benchmarks, supported by a more favourable Euribor environment and renewed demand for fixed-rate products.

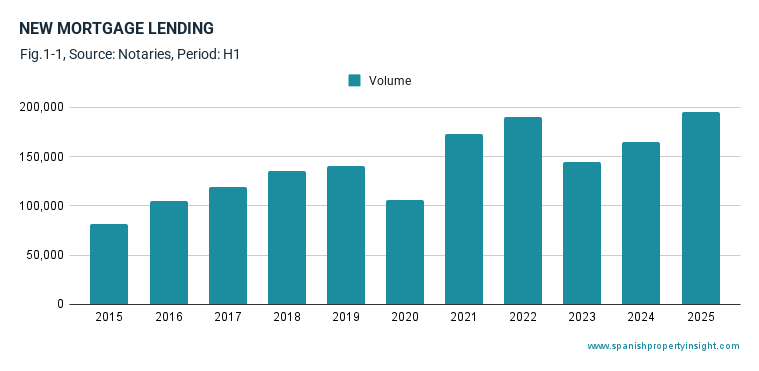

Lending volumes

There were 195,500 new mortgage loans in H1 2025 (Fig. 1-1), an increase of 19% year-on-year. Lending exceeded the ten-year average by 44%, and compared to the same period a decade ago was higher by 141%, underscoring how far the mortgage market has recovered from the post-crisis lows.

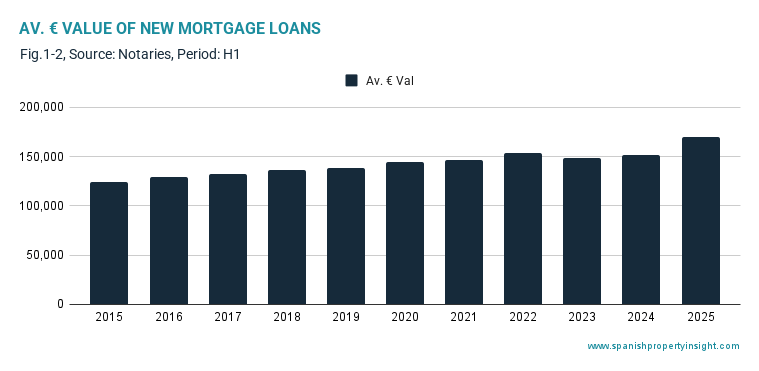

Average loan values

The average new loan value stood at €169,431 (Fig. 1-2), up 12% year-on-year, and 36% higher than in 2015. Rising loan values partly reflect higher property prices over the decade, but also continued demand for higher-value homes in large cities and coastal areas.

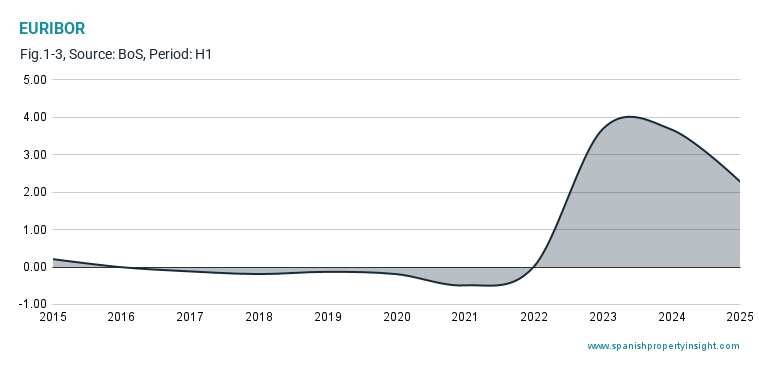

Euribor base rate

The average Euribor during the period was 2.27% (Fig. 1-3), representing a 38% decline compared to a year earlier. This easing contributed directly to lower mortgage rates across both fixed and variable products, and helped stimulate demand after a year of higher financing costs.

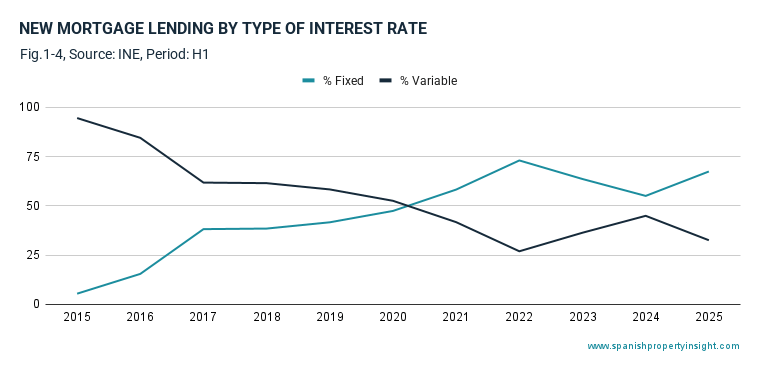

Fixed vs variable-rate preferences

Fixed-rate mortgages continued to dominate. 67% of new loans were fixed-rate in H1 2025, with 33% on variable rates (Fig. 1-4). This represents a rebound in fixed-rate demand after a temporary dip in 2023 and 2024, when rising fixed-rate pricing narrowed the gap with variable loans.

The ten-year trend shows a structural shift: fixed-rate penetration rose from 5% in 2015 to 67% today, while variable-rate products fell from 95% to 33% over the same period. As illustrated in Fig. 1-4, the transition accelerated from 2020 onwards as banks promoted fixed rates and consumers sought stability during periods of rate volatility.

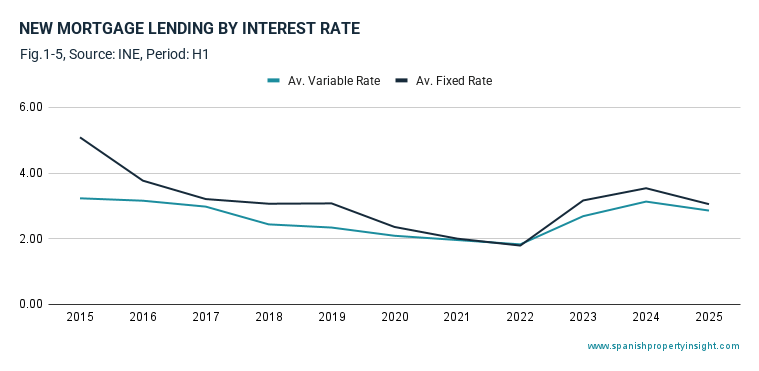

Mortgage interest rates

Mortgage rates eased significantly in H1 2025 (Fig. 1-5). The average interest rate on new loans was 2.98%, down 11% year-on-year.

- Fixed-rate loans averaged 3.05%, falling 14% year-on-year.

- Variable-rate loans averaged 2.86%, down 9%.

Despite the decline, fixed-rate pricing remains only modestly higher than variable rates, which helps explain the recovery in fixed-rate market share this year.

The ten-year comparison indicates that overall mortgage costs are still lower than in the mid-2010s, when average rates were above 3%. Even so, today’s rates remain higher than the ultra-low period of 2021–22, when mortgages averaged below 2%.

Conclusion

The first half of 2025 brought a notable improvement in mortgage-lending conditions. Loan volumes increased strongly, borrowing costs eased as Euribor retreated, and fixed-rate products regained their appeal. The market remains structurally more stable than a decade ago, with a strong bias towards fixed-rate borrowing and healthier lending activity across the board.

2024 H1

Spanish mortgage lending was strong in the first half of 2024, which helps to explain why home sales and prices have also been buoyant this year.

There were 163,859 new mortgages signed in the first half of the year, up 14pc on the same period last year, and 21pc above the ten-year average for the period, according to data from the Spanish notaries’ association, and illustrated in the chart above. It was the third-highest level of new mortgage lending in the last decade, behind only the post-pandemic boom years of 2021 and 2022.

The average value of new mortgage lending was the second-highest on record, with the average new mortgage loan in H1 coming in at €150,545, up 1pc on last year and 7pc on the ten-year average (next chart). So both the volume and value of new mortgages rose in the first six months, putting more investment capital at the disposal of home buyers in Spain.

Spanish mortgage interest rates in H1 2024

The strong mortgage market performance comes despite a radical change in the interest-rate environment since the start of 2022, as shown in the next chart. Mortgage base rates (Euribor 12M) have been steady or declining since the start of 2024. Euribor closed the first half at 3.650, down 8.9pc compared to the same period in 2023. The average rate of Euribor in H1 was 3.672, down 1pc compared to the previous year.

According to data from the National Institute of Statistics (INE) regarding new mortgage lending the average fixed rate in the first five months of the year was 3.56pc, and the average variable rate was 3.16pc, with both rates starting to decline after a year and a half of increases, as illustrated by the next chart.

By type of interest rate, in the first five months of 2024 55pc of new mortgages had a fixed rate and 45pc a variable rate, compared to 63pc and 37pc respectively in 2023, so fixed rate mortgages have been losing ground in the higher interest-rate environment, as shown by the final chart below. Fixed rate mortgages are more interesting when borrowers expect interest rates to go up, not down.