Periodic reports on the North Costa Blanca property market (Alicante province, Valencia)

This page offers data-driven reports on the North Costa Blanca property market, consolidating key data from public sources to highlight the latest trends and developments. Illustrated with charts and infographics, these reports provide critical insights into the North Costa Blanca residential real estate market, with a focus on flagship municipalities such as Calpe, Denia, Javea, and Benidorm. These reports are written for foreign investors, property buyers, vendors, professionals, and journalists looking for insight into the Alicante province / North Costa Blanca property market to help inform big decisions with important financial consequences.

North Costa Blanca property market overview

The North Costa Blanca is a prime destination for international property buyers looking for second homes, holiday properties, or investment opportunities. Renowned for its picturesque coastline, Mediterranean lifestyle, and welcoming expatriate community, the region attracts a significant share of Spain’s foreign property transactions. As one of the most dynamic housing markets in the country, a focused report on the North Costa Blanca property market is invaluable for anyone with an interest in this region.

Located in Alicante province, Valencia, the North Costa Blanca stretches from Calpe to Denia and beyond. Known for its wide range of housing options, from high-end villas to charming coastal apartments, the market offers unique opportunities and challenges worth analysing. Key municipalities like Calpe, Denia, Javea, and Benidorm are among the most sought-after areas for buyers and investors.

The reports cover a wide range of topics to provide a comprehensive understanding of the market, including:

- Home sales across Alicante province and key municipalities.

- Foreign buyers: market share, residency status, and second-home investments.

- New-build properties: sales, pricing trends, and index data.

- House prices: general trends and specific insights into flagship municipalities like Denia and Javea.

- Mortgage lending: base rates, borrowing costs, and their influence on the market.

- Housing starts and key factors affecting supply and demand.

Subscribing to Spanish Property Insight provides full access to exclusive data and insights, empowering you to make informed decisions about property investments, sales, or purchases in the North Costa Blanca. Stay ahead of the market—subscribe today to access the latest North Costa Blanca property market reports.

Want one-time access to the latest report without subscribing?

Fill in the form below to get access to this valuable report without subscribing. A secure link and password will be sent to you by email.

2025 H1

Fill in the form above for one-off access without subscribing.

2024 Full Year

The Alicante & Costa Blanca housing market in 2024 demonstrated solid momentum, supported by strong overall sales, robust price growth in resale properties, and renewed construction activity. While foreign demand remained dominant, its market share gradually declined, indicating a modest shift toward domestic buyers. New-build sales performed particularly well in volume, though average prices fell, signalling changing buyer preferences or market adjustments. Meanwhile, the mortgage market softened slightly amid relatively high but stabilising interest rates. This report examines the main market trends and performance indicators shaping Alicante’s residential property landscape over the year.

Sales performance

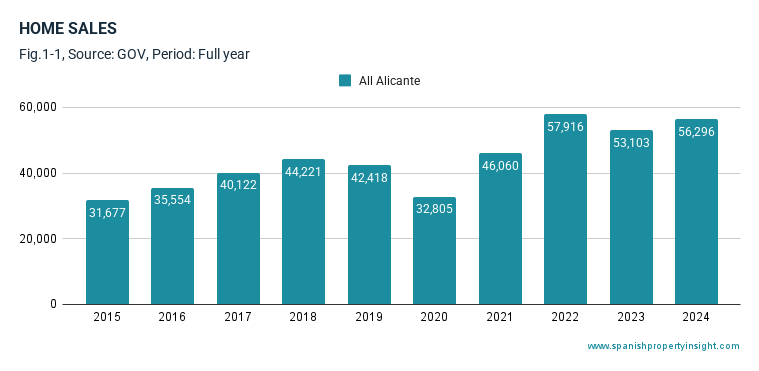

In 2024, home sales in Alicante totalled 56,296 transactions, representing a year-on-year increase of 6% (Fig. 1-1). This is a marginal 0.3% above the ten-year average, and up 78% compared to a decade ago, indicating long-term growth momentum in the regional housing market.

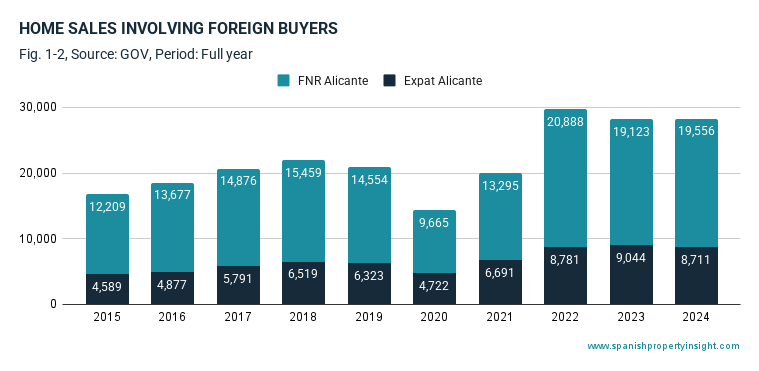

Sales to foreign buyers made up just over 50% of all transactions—a total of 28,267 homes were bought by overseas purchasers, an increase of less than 1% year-on-year (Fig. 1-2). Within this international segment:

- 8,711 homes were purchased by foreigners residing in Spain (expats), marking a small decline of 4% year-on-year.

- 19,556 purchases came from non-resident foreigners (FNRs), a group that typically includes second-home buyers and investors. This subsegment increased by 2%.

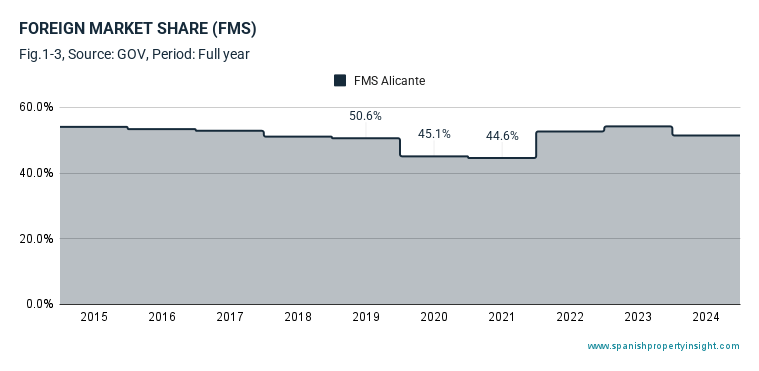

Foreign buyers have historically represented the bulk of demand in this province, but while this group still accounts for 51% of market share, this figure has declined slightly from 54% the year prior (Fig. 1-3), suggesting a slight rebalancing of the market in favour of domestic buyers.

New-build sales were particularly dynamic, with 6,386 new homes changing hands—an annual growth rate of 16% (Fig. 1-4). This figure is 73% above the ten-year average, demonstrating strong developer activity and demand for recently completed properties. Over a ten-year horizon, new home sales are up 28%

North Costa Blanca sales

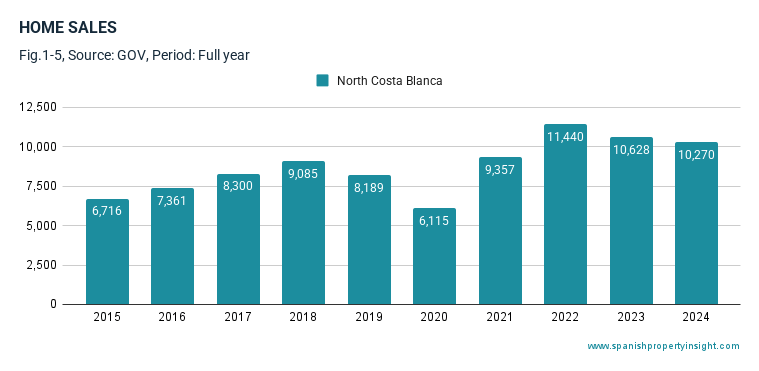

Zooming in on the municipalities* of the North Costa Blanca, a hotspot for foreign buyers and retirees, there were 10,270 sales in 2024—a small dip of 3% year-on-year (Fig. 1-5). Nevertheless, this subregion has seen a 53% rise in total home sales over the past decade, underlining its enduring appeal.

House price trends

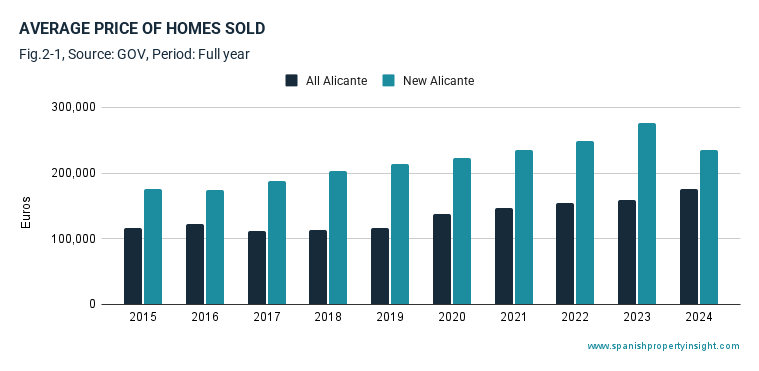

The average sale price of a home in Alicante in 2024 was €176,283, reflecting a robust annual increase of 11% (Fig. 2-1). This rise demonstrates continuing buyer confidence and strong demand for property in the region. However, new-build properties experienced a contrasting trend: the average price of new homes declined by 15% year-on-year to €235,365, indicating potential changes in buyer preferences or market correction from previous highs.

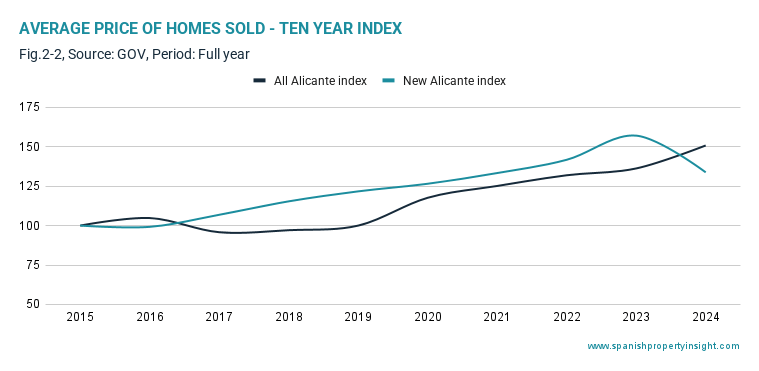

Looking at long-term changes, price indices illustrate diverging trends between general and new-build properties. Over the past decade, all property prices have increased by 51%, while new-build prices have gone up by just 10% (Fig. 2-2). This indicates that resale homes have outperformed new builds significantly—by over 40 percentage points—in terms of price appreciation. Several factors could be driving this differential:

- An evolving preference for properties in consolidated urban or coastal areas where resale properties dominate.

- Competitive pricing strategies by developers or changing cost inputs in new build projects.

- A greater share of smaller or lower-specification new builds compared to earlier years.

Jávea case study

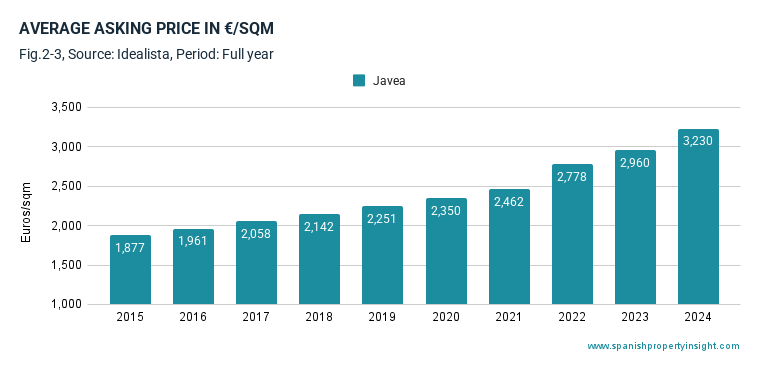

In Jávea (Xàbia)—one of the North Costa Blanca’s most sought-after towns—the average asking price stood at €3,230 per square metre, an annual increase of 9% (Fig. 2-3), according to data from property portal Idealista. Over five years, asking prices in Jávea have grown by 43%, and by 72% in ten years (nominal terms). This mirrors the high demand and limited supply in this popular lifestyle destination.

Mortgage market

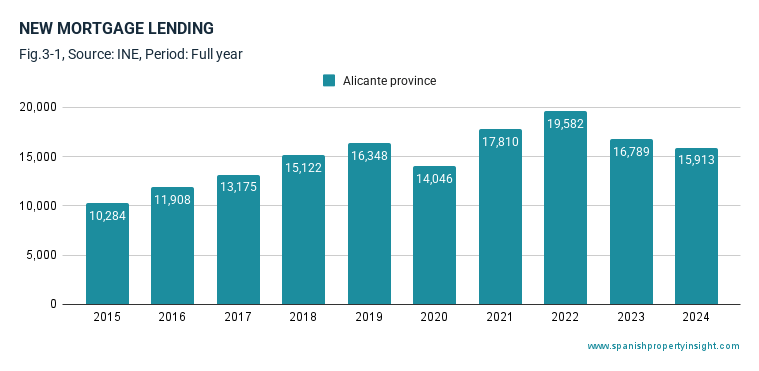

In 2024, a total of 15,913 new mortgages were signed in Alicante province (Fig. 3-1), down 5% year-on-year. However, compared to the ten-year average, mortgage activity increased modestly by 5%, and was up 55% over the decade, suggesting a stable financing environment over the long term.

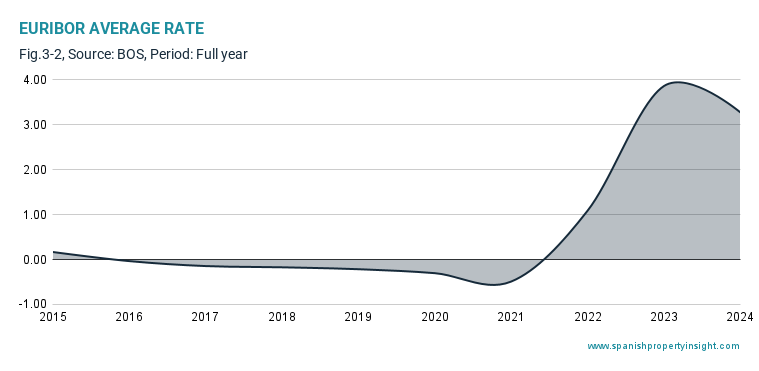

Euribor, the benchmark interest rate underpinning most Spanish mortgages, averaged 3.27% over the year (Fig. 3-2). This is 15% lower than the 2023 average, when the rate peaked at 3.86%. Conversely, it’s significantly elevated relative to the all-time low of -0.49% reached in 2021.

The 2024 decline in Euribor reflects a shift in European Central Bank (ECB) monetary policy. After rapid tightening through 2022 and 2023 to combat inflation, the ECB signalled a pause and potential easing in response to moderating price pressures and a softer economic outlook. As a result, borrowing costs began to stabilise, alleviating some affordability concerns and supporting the mortgage market, albeit cautiously.

Housing starts

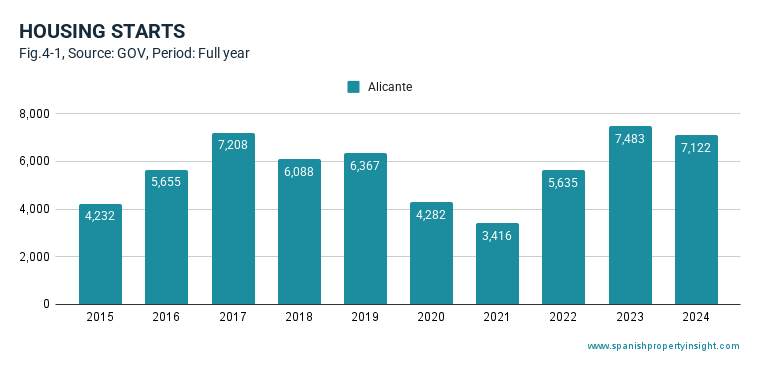

Planning approvals for new housing projects in Alicante reached 7,122 units in 2024 (Fig. 4-1), a modest decline of 5% compared to the previous year. Still, this figure is 24% above the ten-year average and reflects substantial growth of 68% over the decade. Developers remain active, supported by continued buyer interest and sustained foreign investment, particularly in coastal resorts.

While annual volumes are down slightly, the long-term trend remains positive, pointing towards a reasonably healthy development pipeline that is adjusting to short-term fluctuations in demand and financing availability.

Summary

- Total home sales in Alicante rose by 6% to over 56,000, driven by continued demand, particularly in established markets.

- Foreign buyers accounted for 51% of sales but saw their market share decline from the previous year.

- New-build sales surged by 16%, while prices for new properties fell 15%, suggesting a shift in buyer value perceptions.

- Resale properties outperformed new builds in price appreciation over the decade—up 51% versus 10%.

- Mortgage activity eased slightly but remains historically strong. Euribor softened from 2023 highs amid shifting ECB policy.

- New housing starts were down 5% year-on-year but remain well above historic averages.

Conclusion

The Alicante housing market in 2024 remains resilient and dynamic, characterised by robust transaction volumes, rising resale prices, and continued—though moderating—international interest. Foreign buyers, while still dominant, are showing slightly less traction, leaving more space for domestic demand to reassert itself. The price divergence between new builds and resales raises important questions about long-term buyer preferences and the evolving value proposition of different property types.

From a macro perspective, the easing of Euribor suggests improved affordability ahead, which could stimulate demand further—especially if the European Central Bank proceeds with expected rate reductions. Amid fluctuating yet fundamentally solid fundamentals, Alicante’s property market appears poised for continued, albeit more nuanced, growth.

*Municipalities analysed in this report include: Benissa, Benitachell, Calpe, Denia, Javea, Teulada, Alfàs del Pi, Altea, Benidorm, Finestrat, and Villajoyosa.

2024 H1

The first half of 2024

Sales performance

In the first half of 2024, there were 29,366 home sales in the North Costa Blanca housing market, marking a 6% year-on-year increase (Fig. 1-1). This figure represents a 35% rise compared to the ten-year average and a nearly 90% increase over ten years, underlining the market’s robust long-term growth.

There were 14,961 home sales involving buyers from abroad, representing a year-on-year increase of 1%. Compared to the ten-year average, this marks a growth of 38%, and over the decade, sales have risen by 88%. By residency status, these transactions included 4,692 foreigners living in Spain (expats) and 10,269 foreign non-residents (FNR) purchasing second homes and investment properties (Fig. 1-2). The year-on-year change for expat buyers was a decline of 1%, while FNR purchases grew by 2%. Over ten years, purchases by expats have increased by 107%, while those by FNR buyers rose by 80%.

The market share of foreign buyers (FMS) in this area was 51% (Fig. 1-3), down from 54% in the same period a year earlier and below the ten-year high of 54%.

New-build sales saw a notable surge, with 3,217 transactions, a 27% increase year-on-year and a 67% growth over the past decade (Fig. 1-4). This reflects the region’s ongoing appeal for buyers seeking modern properties.

In the municipalities of the North Costa Blanca, there were 5,464 home sales, reflecting a year-on-year decline of 2% (Fig. 1-5). However, compared to the ten-year average, this represents an increase of 26%, and over the decade, sales have grown by 62%.

Prices

The average price of homes sold in Alicante during the period was €168,678, representing a 10% increase year-on-year (Fig. 2-1).

For new builds, the average price was €286,843, up 12% year-on-year (Fig. 2-2).

Over ten years, a price index reveals a rise from a baseline of 100 to 148 for all properties and 168 for new properties (Fig. 2-3).

Over the last five years, prices have risen by 48% for all properties and 37% for new builds, demonstrating steady upward momentum in the market in recent years.

Javea case study

In Jávea, the average asking price for property in H1 2024 was €3,184 per square metre, reflecting a 9% annual increase (Fig. 2-4). Over five years, prices have risen by 42%.

A ten-year index (Fig. 2-5) shows varied growth across the region, with Jávea reaching 173, compared to 162 in Denia, so price has also be driven by local factors.

Mortgages

There were 8,130 new mortgages signed in Alicante province, a 9% decline year-on-year (Fig. 3-1). However, this figure represents a 6% increase compared to the ten-year average and a 61% rise over the past decade, showing long-term resilience in lending activity.

The average Euribor rate during the period was 3.67% (Fig. 3-2), a slight decline from last year’s high of 3.69%. While still elevated compared to pre-2022 levels, Euribor remains far above the pandemic-era lows of -0.49% seen in 2021. European Central Bank (ECB) monetary policy, characterised by tighter interest rates to combat inflation, is expected to keep rates stable or higher in the short term, maintaining upward pressure on borrowing costs.

Housing starts

There were 2,999 housing starts in H1 2024, reflecting a 33% decline year-on-year (Fig. 4-1). Although this figure is 2% above the ten-year average and 34% higher than a decade ago, it remains below the pre-pandemic levels of 2017–2019, indicating a lag in new supply.

Summary: key takeaways

- Sales growth: Transactions increased by 6% year-on-year, with strong participation from foreign buyers.

- Foreign market share: Despite a slight dip, foreign buyers still represent over half of the market.

- New builds surge: Sales of new properties grew by 27% year-on-year.

- Price momentum: Average prices increased by 10% for all properties and 12% for new builds.

- Mortgage trends: Borrowing activity remains robust despite rising interest rates.

- Housing starts lagging: Construction activity has yet to fully recover from the pandemic’s impact.

Conclusion

The North Costa Blanca housing market remains a robust and dynamic segment, with strong price growth, high foreign buyer activity, and solid new-build sales. While mortgage activity has softened slightly due to higher interest rates, the long-term trajectory points to sustained demand and upward price pressure. However, the lag in housing starts could constrain supply, potentially accelerating price growth in the coming years.

Municipalities analysed in this report include: Benissa, Benitachell, Calpe, Denia, Javea, Teulada, Alfàs del Pi, Altea, Benidorm, Finestrat, and Villajoyosa.

Disclaimer

These reports are prepared in good faith using publicly available data. While efforts are made to ensure accuracy, no guarantees are provided regarding the completeness, reliability, or suitability of the information for any purpose. Use of this information is at your own risk.