The Mallorca housing market in 2024

The Mallorca housing market in 2024 presented a picture of cautious resilience, with overall sales holding steady and price growth remaining strong, particularly in premium and newly built segments. While foreign demand remained a key driver, a slight shift in the composition of international buyers was observed, alongside a slowdown in new-build transactions. Mortgage activity posted modest gains, supported by easing interest rates, and housing starts rose sharply, suggesting growing developer confidence. This report examines the key trends and market indicators shaping Mallorca’s real estate landscape during the year.

Sales performance

Home sales in the Balearic Islands totalled 15,485 units in 2024, representing a year-on-year (YoY) increase of 2% (Fig. 1-1). Over ten years sales are up 20%, however, compared to the ten-year average, overall activity was down 3%, which is the more important figure for putting last year’s results in context.

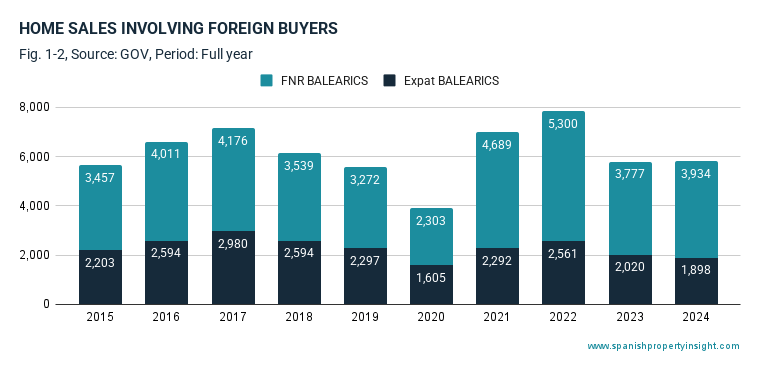

Foreign buyers remained a significant presence in the market. Within this group, foreign non-residents (FNR) accounted for 3,934 transactions—an increase of 4% over the previous year—while foreign residents (expats) completed 1,898 purchases, reflecting a 6% decline year-on-year (Fig. 1-2). Overall foreign demand was 5% below it’s ten-year average. Over the last ten years, demand from foreign residents has fallen by 14%, whereas FNR purchases have increased by the same margin, pointing to a shift toward second-home acquisitions and lifestyle investment rather than full-time relocation.

In total, there were 5,832 sales involving foreign buyers in 2024, representing just under 38% of all transactions (Fig. 1-3). This marks a slight reduction in the foreign market share compared to 39% the previous year, but international demand remains well above historic norms.

New-build home sales

New-build properties experienced weaker performance during the year. A total of 1,264 newly built homes were sold in 2024, marking a 21% decrease year-on-year and 5% below the ten-year average (Fig. 1-4). Over the long term, this segment has contracted by 11%, suggesting underlying issues such as planning restrictions, land scarcity, development lead times, or affordability barriers.

Mallorca maintained its position as the region’s most active market, with 12,011 homes sold in 2024—a 3% increase compared to the previous year (Fig. 1-5). Although slightly below the decade average, this still reflects a strong 26% rise in sales activity since 2014, highlighting Mallorca’s enduring appeal to both local and foreign buyers.

House price trends

The average sale price of homes in the Balearics reached €431,740 in 2024, reflecting a strong annual increase of 14% (Fig. 2-1). Prices for newly-built property were notably higher, averaging €599,895, with a YoY growth rate of 19%.

This continued appreciation aligns with longer-term trends: over the past ten years, the price index for all properties has nearly doubled, rising from 100 to 194.2 (Fig. 2-2). The index for new homes increased even further to 231.9, indicating that over the last decade, new-build prices have risen 19% more than the overall market.

This discrepancy suggests heightened demand or limited supply in the new-build segment—likely driven by higher construction costs, land constraints, or preferences for modern amenities.

Calvià case study

In Calvià, one of the Balearics’ most desirable municipalities, the average asking price stood at €6,420 per sqm, up 8% from the previous year (Fig. 2-3). Over five years, asking prices there have climbed by 59%, and the ten-year price index soared to 249.5, reflecting steep long-term appreciation. Calvià provides a useful benchmark for asking prices in Mallorca’s most desirable areas, highlighting its status as a premium destination for both domestic and international buyers.

Mortgage market

There were 6,826 new mortgages signed in the Balearics during 2024, constituting a 5% annual increase (Fig. 3-1). This figure is broadly in line with the ten-year average and represents a 42% increase over the past decade.

The average Euribor rate stood at 3.27% in 2024 (Fig. 3-2), down from a peak of 3.86% in 2023, reflecting the European Central Bank’s (ECB) shift towards more dovish monetary policy following aggressive tightening in earlier years. Compared to its historic low of -0.49% in 2021, current rates are considerably higher, although markets have priced in further moderation in 2025 as inflation expectations ease across the eurozone. Lower borrowing costs may support mortgage activity and purchasing power in the coming quarters, especially if rate cuts materialise as expected.

Housing starts

A total of 3,352 housing starts were recorded in the Balearics in 2024, a significant annual increase of 20% (Fig. 4-1). This volume also exceeded the ten-year average by 24% and more than doubled from levels a decade ago, up by 105%. The increase in planning approvals suggests that developers are becoming more confident about future demand, or that efforts are being made to meet persistent housing shortages.

Summary

- Overall sales grew modestly by 2% in 2024, while foreign buyer activity softened slightly in market share.

- New-build sales slumped 21% year-on-year, although prices in this segment rose more sharply than existing homes.

- Foreign non-resident demand continues to outpace that of foreign residents, reflecting strong interest in second-home investments.

- Prices in the Balearics rose 14%, with new home prices increasing 19%.

- Mortgage lending grew 5% amid falling Euribor rates, aligned with ECB monetary easing.

- Planning approvals surged, with housing starts more than doubling over ten years.

Conclusion

The Mallorca housing market in 2024 exhibited moderate sales growth, strong price inflation, and a rebound in construction activity. Foreign demand remains robust, particularly among non-residents, although the segment’s market share declined slightly. Soaring prices—especially for new builds—combined with lower interest rates and a surge in housing starts suggest a market positioned for continued activity, albeit with potential affordability constraints. Looking ahead, the market’s trajectory will depend on the pace of new supply, the evolution of interest rates, and the resilience of both domestic and international demand.