Periodic reports on the Costa Brava property market (Girona province, Catalonia)

This page offers data-driven reports on the southern Costa Brava property market, consolidating key data from public sources to highlight the latest trends and developments. Illustrated with charts and infographics, these reports provide critical insights into the Costa Brava real estate market, with a focus on flagship municipalities such as Begur and Pals. These reports are written for foreign investors, property buyers, vendors, professionals, and journalists looking for insight into the Girona province / Costa Brava property market to help inform big decisions with important financial consequences.

Costa Brava property market overview

The Costa Brava is a prime destination for international property buyers looking for second homes, holiday properties, or investment opportunities. Renowned for its stunning coastline, charming towns, and vibrant expatriate community, the region attracts a significant share of Spain’s foreign property transactions. As one of the most dynamic housing markets in the country, a focused report on the Costa Brava property market is invaluable for anyone with an interest in this region.

Located in Girona province, Catalonia, the Costa Brava stretches from Blanes in the south to the French border in the north. Known for its diverse housing options, from luxury villas to coastal apartments, the market offers both unique opportunities and challenges worth analysing. Key municipalities like Begur, Pals, Palafrugell, Palamos, and Platja d’Aro are among the most sought-after areas for buyers and investors.

The reports cover a wide range of topics to provide a comprehensive understanding of the market, including:

- Home sales across Girona province and key municipalities.

- Foreign buyers: market share, residency status, and second-home investments.

- New-build properties: sales, pricing trends, and index data.

- House prices: general trends and specific insights into flagship municipalities like Begur, and Pals.

- Mortgage lending: base rates, borrowing costs, and their influence on the market.

- Housing starts and key factors affecting supply and demand.

Subscribing to Spanish Property Insight provides full access to exclusive data and insights, empowering you to make informed decisions about property investments, sales, or purchases in the Costa Brava. Keep on top of the market—subscribe today to access the latest Costa Brava property market reports.

Want one-time access to the latest report without subscribing?

Fill in the form below to get access to this valuable report without subscribing. A secure link and password will be sent to you by email.

2025 H1

Girona province / Costa Brava housing market: H1 2025

Fill in the form above for one-off access without subscribing.

2024 Full Year

The southern Costa Brava housing market in 2024 continued to demonstrate its appeal as a top destination for both domestic and international buyers, particularly among lifestyle seekers and second-home investors. Sales activity remained positive, supported by resilient demand and a growing interest in high-quality coastal properties. While the foreign buyer segment showed signs of shifting dynamics, with fewer non-resident purchases, overall market fundamentals stayed strong. Rising prices, increased developer activity, and a competitive resale market highlighted the region’s stability amid broader economic challenges. This report offers a detailed analysis of the property market trends across Costa Brava over the past year.

Sales performance

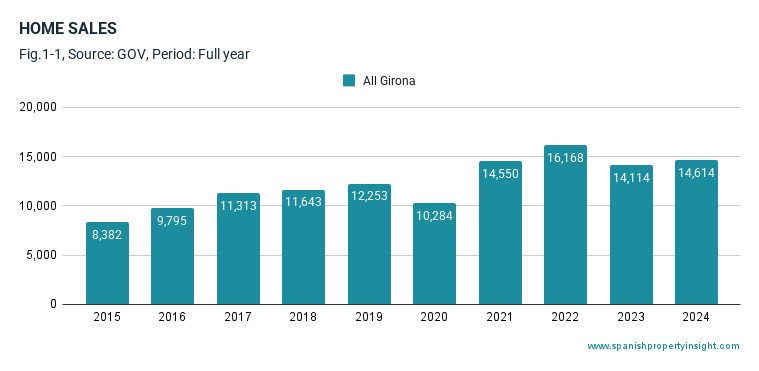

The Girona province housing market (home to the southern Costa Brava) experienced modest growth in 2024. A total of 14,614 homes were sold, representing a year-on-year increase of 4% (Fig. 1-1). This figure is 19% above the ten-year average and marks a strong long-term growth of 74% over the decade.

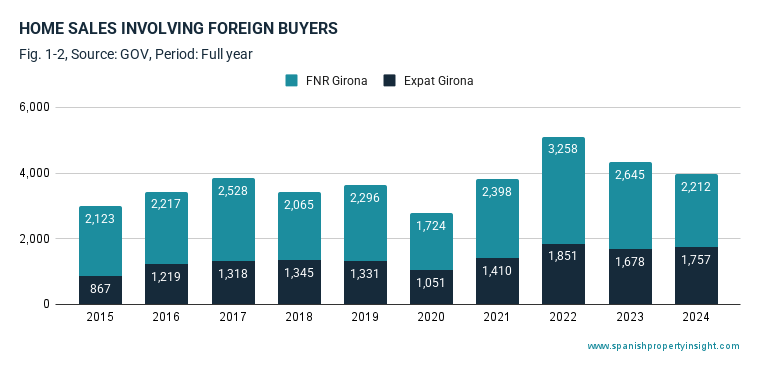

Sales involving foreign buyers totalled 3,969, registering a year-on-year decline of 8%. However, this segment is still 6% higher than the ten-year average and has grown 33% over the past decade. Within this group, 1,757 were purchases by foreign residents (expats), up 5% year-on-year, while 2,212 were foreign non-residents (FNR), down 16% from the previous year (Fig. 1-2). Over ten years, expat purchases increased by 103%, highlighting the rising appeal of this area for long-term foreign residents. In contrast, demand among foreign second-home and investment buyers rose only 4% over the same period.

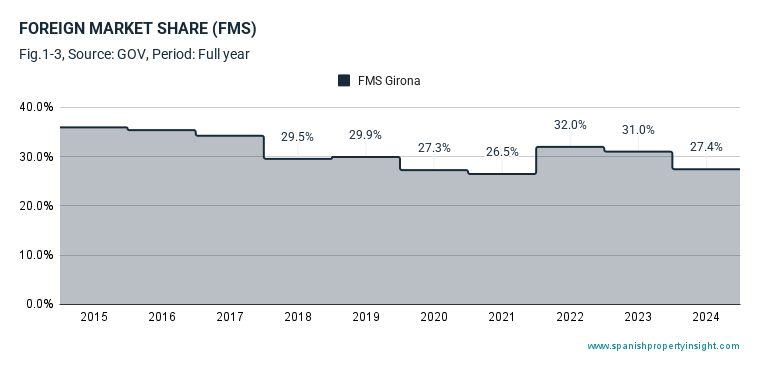

Foreign buyers held a 27% share of the local housing market (Fig. 1-3), a decrease from 31% the previous year, suggesting a mild contraction in international buyer demand as a proportion of total activity in the region.

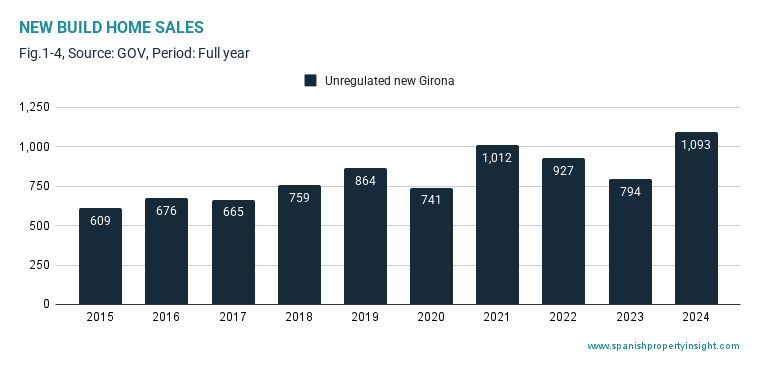

New build sales showed notable growth. There were 1,093 new homes sold in 2024, a jump of 38% year-on-year (Fig. 1-4). This volume is 79% above the ten-year average and 34% higher than a decade ago, reflecting renewed developer activity and sustained demand for modern housing stock.

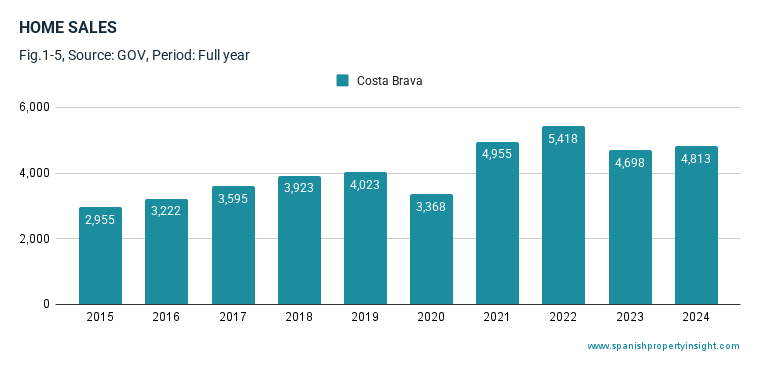

In the Costa Brava municipalities – a key destination for both domestic and international buyers – there were 4,813 transactions in 2024, up 2% year-on-year (Fig. 1-5). This reflects an increase of 17% compared to the ten-year average and a 63% rise over the past decade. See the methodology below for a list of municipalities included in this analysis.

House price trends

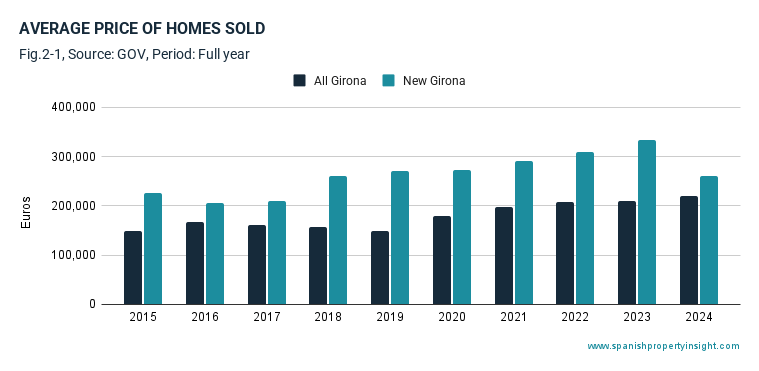

According to data from the Spanish Housing Ministry, the average sale price of properties in Girona province in 2024 was €219,101 (Fig. 2-1), marking a 5% rise over the previous year.

The average price of new build homes in Girona province in 2023 was €260,308, representing a sharp 22% year-on-year decline. This drop could suggest a price correction or potential oversupply in the new build segment. However, it is important to interpret this figure with caution. New builds made up a relatively small part of the market—just 1,093 sales out of 14,600 total transactions—which means the average price is based on a limited data set. As such, a single new development at lower price points, or other one-off factors, can have a disproportionate impact on the average, making the decline potentially an anomaly rather than a sustained trend.

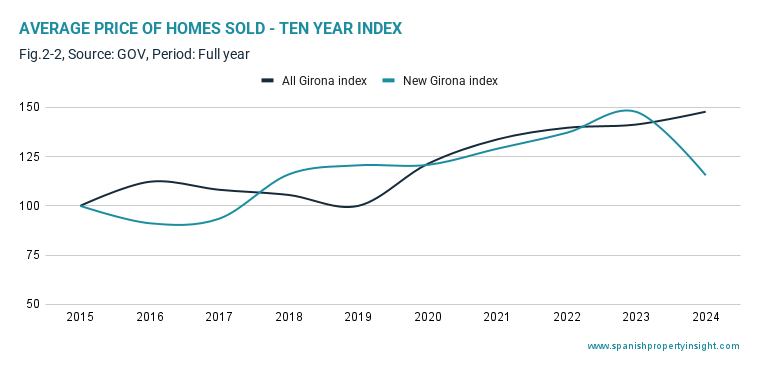

A ten-year price index shows that overall property prices in Girona have risen by 48%, while new build property has only increased by 16% (Fig. 2-2). This suggests that resale properties have appreciated more significantly over the decade, likely due to a mix of increasing scarcity in central urban areas, improved desirability, and stronger demand in well-located second-hand stock. In contrast with the broader market, new build prices showed much lower growth over the period, thanks entirely to a big decline in 2024, which could reflect a shift in construction toward secondary locations where prices tend to be lower, or increased competition among developers. However, as new builds account for a small share of the market, the average price is more sensitive to the characteristics of specific projects. With just over 1,000 sales recorded, the segment is susceptible to volatility. A single development with lower pricing or temporary market dynamics can easily skew the figures. As such, the 22% price decline observed in 2023 may not signal a structural trend but rather a one-off deviation caused by the small sample size.

Over the past five years, prices for all residential properties have grown by 48%, while new build prices declined slightly by 4%, reinforcing the trend that the resale market is driving overall value growth in the region.

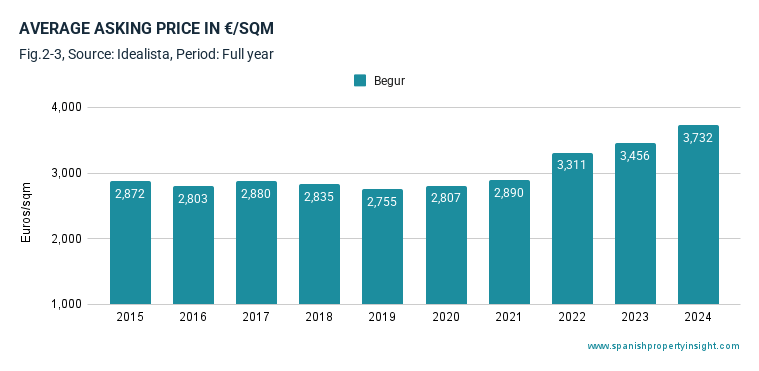

Asking price data from the property portal Idealista supports this view, with advertised prices averaging €2,357 per square metre in 2024 – up 6% from the previous year (Fig. 2-3), and 18% higher than five years ago. Over ten years asking prices increased 35% in nominal terms. This figure reflects vendor expectations and market sentiment, strengthening the narrative of long-term capital appreciation in the region.

Mortgage market

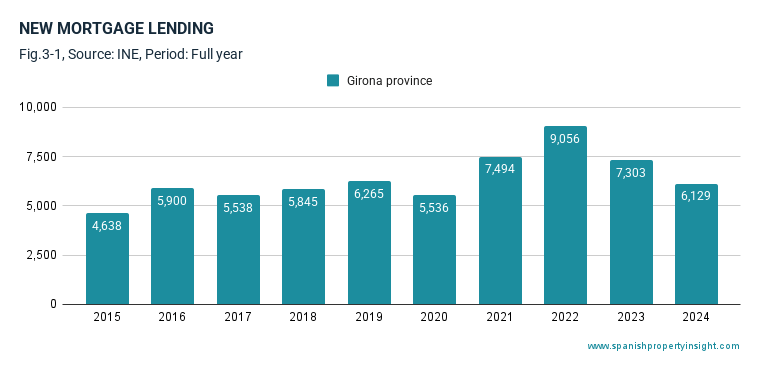

A total of 6,129 new mortgages were signed in Girona during 2024 (Fig. 3-1), which represents a 16% decline compared to the previous year. This is 4% below the ten-year average but remains 32% higher than in 2014, indicating broad-based credit growth over the longer term despite short-term contraction.

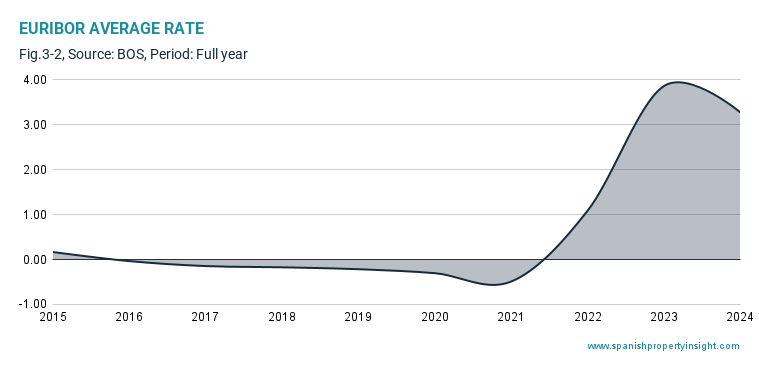

The average Euribor rate during the year was 3.27% (Fig. 3-2), slightly below the 2023 peak of 3.86% but significantly above the negative rates seen in 2021, when Euribor dropped as low as -0.49%. The current level reflects a stabilisation phase in European monetary policy following a cycle of aggressive rate increases by the European Central Bank (ECB) to combat inflation. Market expectations at the end of the year suggested that interest rates may have peaked, with the possibility of gradual reductions starting in 2025, depending on inflationary dynamics across the eurozone.

Housing starts

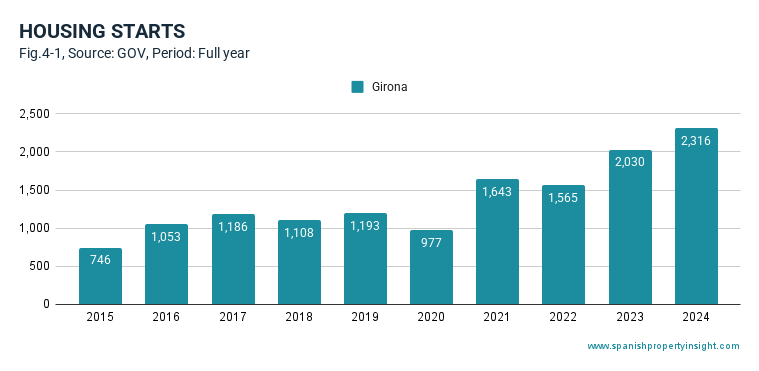

Planning approvals for new residential construction rose to 2,316 in 2024 (Fig. 4-1), a 14% increase on the previous year. This figure is 68% higher than the ten-year average and more than triple the level recorded a decade ago. The data reflects strong confidence among developers, as well as pent-up supply-demand imbalances, particularly in high-demand coastal areas such as the Costa Brava.

Market drivers

Although not specified in the available data, some key market drivers during the period likely include:

- Continued interest from domestic buyers benefitting from wage increases and resilient employment.

- Strong lifestyle and tourism appeal in Costa Brava municipalities for both short-term lets and long-term residence.

- Decreasing affordability pressures in high-growth urban markets like Barcelona, prompting demand spillover into Girona and surrounding areas.

- Higher borrowing costs dampening investor activity, particularly among foreign non-resident buyers.

Summary

- Home sales in Girona rose 4% year-on-year, with long-term growth of 74% over the past decade.

- Foreign buyer activity declined 8% overall, with sharp divergence between expat growth (+5%) and non-resident decline (-16%).

- New build sales climbed 38%, while general property prices rose 5% on average.

- New mortgage volumes fell 16%, reflecting the impact of elevated borrowing costs.

- Euribor averaged 3.27%, marking a softening trend after 2023’s peak.

- Housing starts reached 2,316, up 14% year-on-year and strongly above historical averages.

Conclusion

The Girona housing market in 2024 remained resilient, supported by strong local demand and growing developer activity. While higher interest rates have dampened foreign non-resident and investor segments, the expat and local buyer base continues to drive market momentum. With signs of interest rate stabilisation and continued buyer interest in coastal municipalities, the region seems positioned for continued, if moderate, growth in 2025.

2024 H1

Girona province and Costa Brava property market report: H1 2024

Sales performance

In the first half of 2024, Girona province (home to the Costa Brava) recorded 7,254 home sales, reflecting a slight year-on-year increase of 0.2% (Fig. 1). This represents a similar 0.2% rise compared to the ten-year average. Over the past decade, the market has experienced a cumulative growth of 91.1%, demonstrating robust long-term development.

Foreign buyers

Sales involving foreign buyers totalled 1,939 transactions, a 14.2% decline year-on-year. Compared to the ten-year average, however, this segment has grown by 9.9%, with a ten-year increase of 40.3%. Among these (Fig 2):

- 868 sales were by foreign residents in Spain (expats), marking a 0.5% year-on-year increase.

- 1,071 sales were by foreign non-residents (FNR), representing a 23.3% decrease year-on-year.

The overall market share of foreign buyers was 26.7%, down from 31.2% in the same period a year ago and below the ten-year high of 36.4% (Fig. 3). This indicates a declining contribution of foreign buyers, particularly in the non-resident segment.

New build homes

The new build market saw significant growth, with 667 sales, a 86.3% year-on-year increase. This was a 64.2% rise compared to the ten-year average, and over the decade, new build sales have surged by 156.5% (Fig. 4). This highlights increasing demand for new developments, driven by both domestic and international buyers.

Costa Brava municipalities

In the Costa Brava region specifically, 2,404 sales were recorded in municipalities of the Costa Brava (Fig. 5), a 0.5% year-on-year rise, and the second-highest level on record. Compared to the ten-year average, this marks a 21.4% increase, with cumulative growth of 81.9% over the past decade.

Price trends

The average price of homes sold in Girona province during H1 2024 was €218,915, representing a 6% increase year-on-year. (Fig. 6) The average price of newly built homes was €301,000, a 1% decline year-on-year, suggesting potential shifts in supply or buyer preferences.

Long-term price index

Over ten years, the price index for all properties in Girona has risen from 100 to 151, and 149 for newly-built homes.

But in just the last five years:

- Prices for all properties have grown by 51%.

- New build prices have risen by only 8%, indicating slower growth in this segment.

Interpretation: The divergence between overall price growth and new build trends may reflect increased supply of affordable new developments or shifting buyer focus towards resale properties.

Mortgage activity

In H1 2024, 3,332 new mortgages were signed in Girona province (Fig. 8), a 14.2% year-on-year decline (Source: INE). Compared to the ten-year average, this represents a 1.2% increase, and over the decade, mortgages have grown by 44.3%.

The average Euribor rate during the period was 3.67 (Fig. 9), slightly lower than the previous year’s high of 3.69 in 2023. This rate remains significantly higher than the decade-low of -0.49 recorded in 2021. The elevated Euribor reflects tighter monetary policy by the European Central Bank (ECB) aimed at combating inflation. However, markets anticipate stabilisation or slight reductions in 2025, depending on inflation trends.

Housing starts

The period saw 1,490 housing starts, based on planning approvals (Fig. 10). This represents a 72.9% year-on-year increase and a 99.2% rise compared to the ten-year average. Over the past decade, housing starts have surged by 367.1%.

A ten-year index of housing starts (Fig. 11) illustrates a marked increase, underscoring strong developer confidence and alignment with demand for new housing stock.

H1 2024 Girona / Costa Brava report – key takeaways

- Stable overall sales: Modest growth in total transactions highlights resilience, despite a decline in foreign non-resident activity.

- Foreign market shift: Reduced foreign market share indicates changing dynamics, particularly among non-residents, while expat demand remains stable.

- New build boom: The sharp increase in new build sales and housing starts underscores robust development activity.

- High mortgage rates: Elevated Euribor levels reflect ongoing ECB monetary tightening, potentially dampening borrowing activity in the short term.

- Price trends: Divergent growth in prices for resale and new build properties offers insights for developers and investors.

Methodology and geographic focus

- Sant Feliu de Guíxols

- Santa Cristina d’Aro

- Castell–Platja d’Aro

- Calonge

- Palamós

- Mont-ras

- Palafrugell (including Llafranc, Calella de Palafrugell, and Tamariu)

- Begur

- Pals

- Torroella de Montgrí (including L’Estartit)

This geographical focus ensures that the analysis in the following sections accurately reflects the market dynamics of the southern Costa Brava

The Costa Brava comprises the coastal municipalities of Girona province, specifically located in the counties (comarcas) of La Selva, Baix Empordà, and Alt Empordà. Because much of the publicly available data is aggregated at the provincial level, this report uses figures for Girona province to analyse general trends in sales, prices, mortgage lending, and housing starts in the area where the Costa Brava is located.

To provide a more focused view, we also drill down into sales data for the Costa Brava municipalities themselves and examine house prices in one or two representative locations to get a clearer picture of pricing trends at the local level.

The Costa Brava can be divided into two distinct sections: northern and southern. This report focuses on the southern Costa Brava, which is the best known and most popular part of the coast, especially among second-home buyers and international investors.

When it comes to sales in the southern Costa Brava, the report uses data for the following municipalities:

In the comarca of La Selva:

- Blanes

- Lloret de Mar

- Tossa de Mar

In the comarca of Baix Empordà:

- Sant Feliu de Guíxols

- Santa Cristina d’Aro

- Castell–Platja d’Aro

- Calonge

- Palamós

- Mont-ras

- Palafrugell (including Llafranc, Calella de Palafrugell, and Tamariu)

- Begur

- Pals

- Torroella de Montgrí (including L’Estartit)

This geographical focus ensures that the analysis in the following sections accurately reflects the market dynamics of the southern Costa Brava

Disclaimer

These reports are prepared in good faith using publicly available data. While efforts are made to ensure accuracy, no guarantees are provided regarding the completeness, reliability, or suitability of the information for any purpose. Use of this information is at your own risk.