The Spanish press was full of news yesterday about the slump in British demand post-Brexit, but regular readers of SPI will have know about this since February.

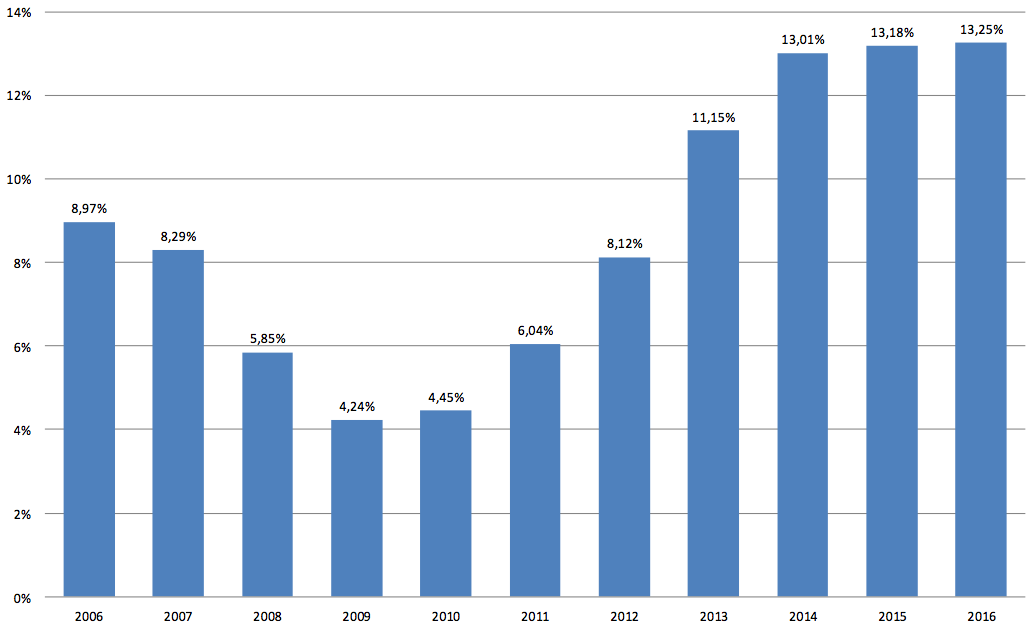

The trigger for the sudden interest in foreign demand was the publication this week of The Spanish Registrars Association’s annual report on the housing market. This revealed that foreign demand now accounts for a record 13.25% of the Spanish housing market, significantly higher than the 8.97% clocked up in the boom year of 2006.

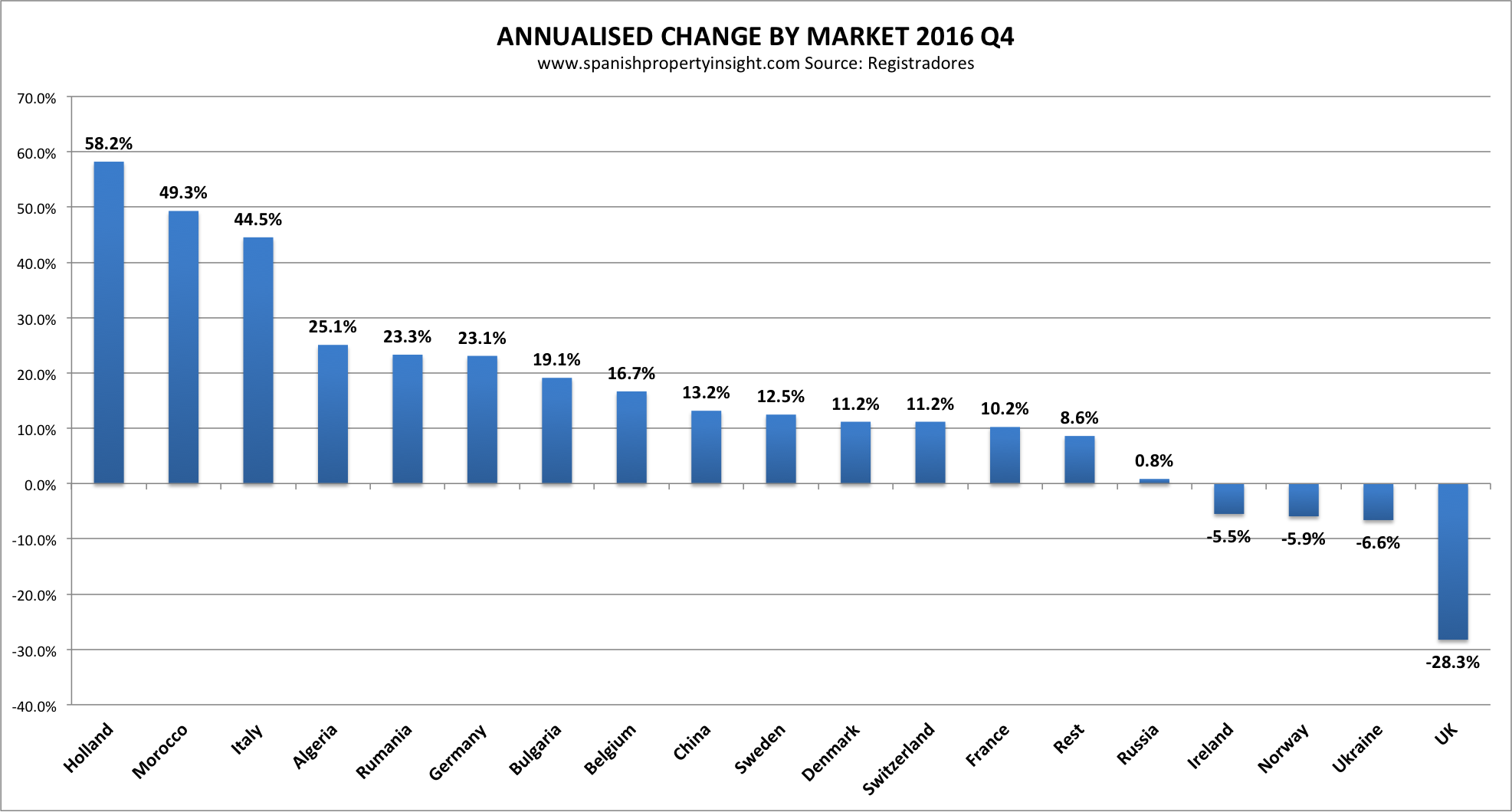

The other big story in the registrars’ figures was the retrenchment in British demand, which fell from 21% of foreign demand in 2015, to 19% in 2016, something the registrars attributed, quite rightly, to Brexit. This shows a “declining trend in relative importance [of British demand] since Brexit,” say the registrars, “in contrast to what happened before, when quarter after quarter its relative importance increased, taking advantage of the strong Pound.” The registrars lament the “reduction in demand from our biggest market.”

The retrenchment in British demand has been given considerable attention in the Spanish press, and also got a fair bit of coverage in the international media. You would think this news had taken us by surprise. But I wrote about this back in February, when the registrars published their quarterly figures for Q4. Knowing, as I do, that the registrars publish their annual report at a leisurely pace (we are almost into May), I always make an effort to dig the figures out of every quarterly report and give my readers a reliable picture of annual foreign demand about three months before the story hits the news wires.

If you consider growing demand for property in Spain to be a good thing, then the positive news is that demand is growing from an ever-increasing number of countries, with the notable exceptions of Norway, Russia, and Denmark. But the annual report from the registrars paints a picture of retrenchment in British demand, which they only mention as losing relative importance. In reality British demand has slumped, at least if the figures for Q4 2017 are anything to go buy (-28%).