- This topic has 44 replies, 9 voices, and was last updated 12 years, 8 months ago by

Anonymous.

Anonymous.

-

AuthorPosts

-

-

October 2, 2013 at 2:04 pm #57813

AnonymousParticipant

AnonymousParticipant

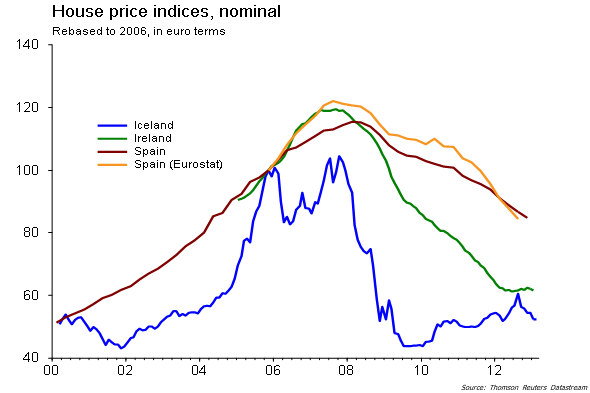

Base on official figures, of course. In reality house prices here have fallen 50pc, at least. We would be at the bottom if we had reliable stats. 😀

-

October 2, 2013 at 3:29 pm #118362Fuengi (Andrew)Participant

interesting.

did the site you got this from also have one going further back?

Wonder how the % would look if it started in 2000. -

October 4, 2013 at 10:01 am #118373ChoperaParticipant

Did they normalise the currencies for those prices? Measured in euros the UK market collapsed a lot more than that I think.

-

October 4, 2013 at 10:21 am #118375katyBlocked

According to this the UK. housing market lost 26%. With the last 12 month increases most have recovered to 2008 levels.

-

October 4, 2013 at 7:05 pm #118388The AustralianParticipant

well I can never find anything cheap in Greece, how is that?

-

October 7, 2013 at 7:43 pm #118396ChoperaParticipant

@katy wrote:

According to this the UK. housing market lost 26%. With the last 12 month increases most have recovered to 2008 levels.

But the pound is lower than it was against the euro before Lehman. I can’t remember how much lower – maybe up to 20% lower – so measured in euros UK prices are up to 20% down compared to 2008.

-

October 7, 2013 at 8:40 pm #118397katyBlocked

Can you explain what the euro to pound rate has to do with UK house prices 😕 In any case the rate was an average of about 1.20 throughout 2008. my opinion is that it doesn’t give a FF what the rate was, totally irrelevant!

-

October 8, 2013 at 8:13 am #118398angieBlocked

Chopera, katy is right, the fact that stg is lower against the euro does not affect UK house prices one iota. I should add that it might make them more attractive to those using Euros to buy them, theoretically an influx of buyers could push UK prices up. People in the UK still buy UK property in stg. Why would anyone measure their UK property in Euros? It only affects them if they use that same stg amount to buy properties in the Eurozone 🙄

-

October 8, 2013 at 11:44 am #118400AnonymousParticipant

The exchange rate isnt important in the way you guys are debating but it means the Uk has become poorer but at the same time it has boosted the uks ability to compete with other counties industries. Measuring exchange rates fluctuations in the short term may not show any real “truth” though.

-

October 8, 2013 at 11:48 am #118401ChoperaParticipant

@katy wrote:

Can you explain what the euro to pound rate has to do with UK house prices 😕 In any case the rate was an average of about 1.20 throughout 2008. my opinion is that it doesn’t give a FF what the rate was, totally irrelevant!

The thread is about international house price comparison (the clue is in the title and the graph in the op). There is a difference between comparing house prices measured nominally in their respective local currencies, and comparing house prices measured in the same currency. The thread is not specifically about UK house prices – I simply chose them as an example to make that point. I’ve looked at a few charts and it seems the pound has been 5-10% lower through 2013 than it was leading up to the Lehmans collapse. But the actual figure is irrelevant – my point is that it would be interesting to know whether the price changes in that graph were measured in local currencies or not.

-

October 8, 2013 at 12:56 pm #118402ChoperaParticipant

@angie wrote:

Chopera, katy is right, the fact that stg is lower against the euro does not affect UK house prices one iota. I should add that it might make them more attractive to those using Euros to buy them, theoretically an influx of buyers could push UK prices up. People in the UK still buy UK property in stg. Why would anyone measure their UK property in Euros? It only affects them if they use that same stg amount to buy properties in the Eurozone 🙄

The point I’m trying to make is that the comparison of international house prices is affected by the currency. Another example, according to the graph house prices have in the UK are roughly the same in pounds compared to 2008, and house prices in Switzerland have risen by 25% in Swiss Francs in the same period. But the pound has gone down from being worth about 2 Swiss Francs to being worth about 1.5 Swiss Francs now. So in “real” terms house prices in Switzerland have risen by nearer 35% compared to house prices in the UK. Again the amounts are not important, I’m just trying to illustrate a point.

-

October 8, 2013 at 5:21 pm #118403katyBlocked

Your logic is flawed. On that basis then we could calculate that prices in Spain rose when the pound dropped a third in value 🙄 There are a few different currencies in that graph which would make it totally meaningless. The only truth we know is that house prices are rising in most of the UK and this is the only fact that 98% of Britains need to know. Has nothing to do with the Euro/Dollar/Dirham etc.

-

October 9, 2013 at 3:01 am #118404AnonymousParticipant

I’m with Chopera on this one. If you have a basquet with difference currencies and for example the pound has lost or gained its value against a majority of them it would be wrong not to factor that into it when compairing the state of the real estate sector. Normal people may not care but in the long run they will be affected by it. For example the loss in value of once currency might mean lesser competition power in the world.. less jobbs…higher interest when the situation goes to far etc.

-

October 9, 2013 at 8:27 am #118405angieBlocked

I’m with katy on this on 😛 , Brits living in the UK with UK properties don’t see falls in Stg terms other than regional differences, ie London prices compared to run down area prices.

House prices may well be at 2008 levels in many parts of the UK, but they are rising now in most areas and have been this year. Further these Gov’t schemes will probably generate more demand than supply, rises expected plus a strong Euro is the reason why many French and other nationalities are buying UK property as a safer bet.

We sold UK property in 2007 and made a 29% (after transaction costs) profit in stg, bought and sold in 2008 and made just over 30% (ATC) profit, bought in 2010 and value has risen 20% so far according to 4 agents, I don’t see that as depreciating funds, our Bank balance has risen, compared with what it would have in many other countries. BTW no capital gains tax either if your main home unlike much of EU. Profit is made by buying right and low transaction costs 🙄

A fact is that had you invested the equivalent Stg sum in Spanish, French, Greek, Italian (and many EU) property during the boom years, your investment will have dropped considerably unless in prime spots. Had you invested same sum in UK and German property your money would still be intact or risen. Only inflation paper loss.Meanwhile, despite stg down against the Euro, we have a lot more stg to buy euros/dollars etc if we wanted, and could take advantage of crashed property markets too 🙄

-

October 9, 2013 at 10:10 am #118406zoroParticipant

Any self respecting publication when reporting on price fluctuations for any commodity will use the currency in which those commodities are traded. For international commodities such as oil and gold this would be dollars.

For UK property it would be GBP, for Eurozone properties it would be EUR and for US properties it would be USD etc. etc. To do otherwise would be particularly stupid and futile as they would not be measuring price fluctuations of that commodity but instead would be measuring that AND currency fluctuations.The report that Mark posted originally came from a company called Knight Frank referred to here: http://www.portfolio-property.com/article/view/id/441

They report on the global property market and they state elsewhere on the Knight Frank website:

“The Knight Frank Global House Price Index established in 2006 is the definitive means for investors and

developers to monitor and compare the performance of mainstream residential markets across the world. The index

is compiled on a quarterly basis using official government statistics or central bank data where available.”As you might expect, such sources will report in their own currencies e.g. the BOE or British Government measure price changes in their jurisdiction in GBP not EUR unless explicitly stated otherwise.

However I do think it is an interesting point to consider how the devaluation of one currency affects the price of commodities in another; especially Spanish property. For instance I am pretty certain that the loss of value of the GBP against the EUR must have affected the Euro price if only because of the dampening of UK demand it would have caused. Conversely UK, and especially Central London, property prices have surely been propped up by making them look attractive to foreign buyers in their own currencies.

-

October 9, 2013 at 10:27 am #118407ChoperaParticipant

@katy wrote:

Your logic is flawed. On that basis then we could calculate that prices in Spain rose when the pound dropped a third in value 🙄

No but we could say that the relative value of houses in the UK dropped by a third, compared to Spain. Of course someone living in the UK holding pounds won’t notice it to begin with, and won’t really care. However the longer term effect of devaluing your currency is to create inflation, and that will devalue your house if you are holding pounds. Since 2008 the UK has had inflation running at say 3% each year, the cumulative effect of which would have been to devalue house prices in real terms (i.e. inflation adjusted) by about 16%.

@katy wrote:

There are a few different currencies in that graph which would make it totally meaningless. The only truth we know is that house prices are rising in most of the UK and this is the only fact that 98% of Britains need to know. Has nothing to do with the Euro/Dollar/Dirham etc.

But when it comes to comparing house prices between countries, which is what we are doing in this thread, it is has a lot to do with the exchange rate. And even if you still insist on ignoring what this thread is about and instead harping on about UK house prices and what Britons need to know (even though this is a Spanish property forum) most people who have a basic understanding of economics want to know how much of those price rises are due to monetary inflation and how much are due their real value going up, i.e. they want to know the inflation adjusted change in value.

-

October 9, 2013 at 11:04 am #118408ChoperaParticipant

@zoro wrote:

Any self respecting publication when reporting on price fluctuations for any commodity will use the currency in which those commodities are traded. For international commodities such as oil and gold this would be dollars.

For UK property it would be GBP, for Eurozone properties it would be EUR and for US properties it would be USD etc. etc. To do otherwise would be particularly stupid and futile as they would not be measuring price fluctuations of that commodity but instead would be measuring that AND currency fluctuations.…

You report price fluctuations in international commodities in the same currency, and if you are reporting on international house prices you should also stick to the same currency. The reason national house prices are reported in their local currencies is because property isn’t traded internationally. But if you want to make an international comparison of property prices you need to do it in the same currency. Or if you prefer, you can compare them in terms of gold or some other commodity or index.

-

October 9, 2013 at 11:09 am #118409katyBlocked

@Chopera wrote:

. And even if you still insist on ignoring what this thread is about and instead harping on about UK house prices and what Britons need to know (even though this is a Spanish property forum) most people who have a basic understanding of economics want to know how much of those price rises are due to monetary inflation and how much are due their real value going up, i.e. they want to know the inflation adjusted change in value.

That’s a bit rich…you are the one that brought the UK and the daft currency difference into it 👿 Even though it is a Spanish property forum. I would imagine anyone looking at Spanish property right now would be only interested in how property has fallen in Spain. Most punters want a home in the sun not a lesson in elementary economics!

Clearly the above graph is in percentages with information from each country.If we take your daft theory then we can deduce that Spanish property hasn’t dropped much at all for the average Brit 🙄 🙄 😆

-

October 9, 2013 at 11:12 am #118410katyBlocked

@Chopera wrote:

You report price fluctuations in international commodities in the same currency, and if you are reporting on international house prices you should also stick to the same currency. The reason national house prices are reported in their local currencies is because property isn’t traded internationally. But if you want to make an international comparison of property prices you need to do it in the same currency. Or if you prefer, you can compare them in terms of gold or some other commodity or index.

You are crazy

This is a Spanish property forum not an international investors forum

This is a Spanish property forum not an international investors forum -

October 9, 2013 at 11:34 am #118411zoroParticipant

@Chopera wrote:

You report price fluctuations in international commodities in the same currency, and if you are reporting on international house prices you should also stick to the same currency. The reason national house prices are reported in their local currencies is because property isn’t traded internationally. But if you want to make an international comparison of property prices you need to do it in the same currency. Or if you prefer, you can compare them in terms of gold or some other commodity or index.

Irrespective of what you think reporters should or shouldn’t stick to – respected publications abide by well understood rules; unless stated otherwise, reported price fluctuations are based on the currency in which those commodities are traded. If Knight Frank wished for some obscure reason to convert all prices into Euros they would state that and the exchange rate they used. That is not the case. You are making a ridiculous and unfounded assertion that Knight Frank should pander to your ideas of how commodities should be compared. They are measuring percentage changes of property prices NOT exchange rate fluctuations. If you think they are wrong to do that tell the author.

-

October 9, 2013 at 11:43 am #118412angieBlocked

Sorry but I don’t follow your logic chopera. 😕

Here is a graph from The Economist magazine on global house prices.

http://www.economist.com/blogs/dailychart/2011/11/global-house-prices

If you click on each country, you can see the huge boom and bust of 2 countries particularly, both Euro countries, Spain and Ireland. Both boomed unrealistically and have experienced the most prolonged and sharpest falls which are ongoing it seems.

Click on other countries including UK and you see a steady rise in values, not the huge price drops. My feeling is this is based on more demand than supply, unlike Spain, although Ireland’s is a conundrum there.

With the UK’s measures in place, Help to Buy, Funding for Lending etc I would be using my Euros to buy what looks safer ie UK property for the next 2-3 years. (a) It’s a rising market with limited supply. (b) A strong Euro means UK property is more attractive as you buy more Stg. (c) Transaction costs don’t kill the deal for buying and selling certainly up to £250k, and even up to £500k.

-

October 9, 2013 at 12:57 pm #118414AnonymousParticipant

You can already buy a two bedroom apartment in Alicante for 20,000 euros and I expect that in three years time when the American economy collapses, The UK economy collapses and the Spanish economy collapses that you will be able to buy a two bedroom apartment in Spain for as little as 10,000 Euros or in Spanish Pesetas for as much as 20 trillion Pesetas given the devaluation of the Spanish currency when Spain finally drops out of the Euro.

-

October 9, 2013 at 2:13 pm #115762AnonymousParticipant

I know its totally irrelevant in the grand scheme of things but this is an real example of a sale in Sweden “mine and I want to brag a little;)” and to show how much or little these sort statistics mean when it comes to localized markets.

Fourth biggest city in the country 150k something population.

Bought a 72sqm one bedroom apartment in the center of town a few weeks after lehman brothers collapsed for 100k euros. Renovated for 15k. Sold two months ago for 210k euros. Agent fees 3, 8k euros and we dont have any taxes on apartments here. My share of the apartment complex indirect debt for that apartment was 78k “has gone up quite a lot because of modernizations in the last 10 years” euros. So in reality the new owner now bought it for 288k euros. Its around 100% in gain in less than 5 years. Monthly fee everything included 400 euros.

I bought a 60sqm one bedroom apartment 10 miles from the first place in a small town for 2k euros in identical condition with only 12k of indirect debt “which has gone down in the last fifteen years because of a well run economy”. This apartment was sold fifteen years ago for 15k euors. It was cheaper to buy and own this place than to rent storage space for my stuff and I also have somewhere to live. I dont care if its worth nothing in a years time “which I doubt”. 2, 5 miles to nearest cityof a 140k populace. The indirect debt is not personal so I can in the worst case scenario just hand the keys back to the complex. 290 euros everything included. People live and pay around 550 euros a month for rental in bad condition just 100-200m from here and there are no vacancies.. In less than 10 months they would be saving money by buying.

I dont really understand how the variations ca be this extreme and anyone that believes prices will sky rocket forever in our cities will be in for a rude awakening. People are buying cars and going on vacations on their spare equity. No one is paying off on their loans. The economy is doing ok compared to the rest but people are pretending like its never going to change.. We are heading for a crash is my guess.

-

October 9, 2013 at 3:41 pm #118416ChoperaParticipant

@zoro wrote:

…

Irrespective of what you think reporters should or shouldn’t stick to – respected publications abide by well understood rules; unless stated otherwise, reported price fluctuations are based on the currency in which those commodities are traded. If Knight Frank wished for some obscure reason to convert all prices into Euros they would state that and the exchange rate they used. That is not the case.I have made absolutely no comment on how prices should be reported. I have simply made a comment on how prices should be compared. Of course house prices in a particular country should normally be reported in the currency of that country, my point is that when you come to comparing those prices with those of another country that has reported prices in a different currency, you should take that into account.

@zoro wrote:

You are making a ridiculous and unfounded assertion that Knight Frank should pander to your ideas of how commodities should be compared. They are measuring percentage changes of property prices NOT exchange rate fluctuations. If you think they are wrong to do that tell the author.

You seem to half get it and then you don’t. If you don’t want exchange rate fluctuations to influence the price comparison then don’t compare price changes in different currencies. It really is that simple. It doesn’t matter which currency you use, or whether you measure them compared to the price of a can of beans, just make sure the price change quoted is measured in terms of the same reference. And I’m sure the author knows this.

-

October 9, 2013 at 4:15 pm #118417ChoperaParticipant

@angie wrote:

Sorry but I don’t follow your logic chopera. 😕

Here is a graph from The Economist magazine on global house prices.

http://www.economist.com/blogs/dailychart/2011/11/global-house-prices

If you click on each country, you can see the huge boom and bust of 2 countries particularly, both Euro countries, Spain and Ireland. Both boomed unrealistically and have experienced the most prolonged and sharpest falls which are ongoing it seems.

Click on other countries including UK and you see a steady rise in values, not the huge price drops. My feeling is this is based on more demand than supply, unlike Spain, although Ireland’s is a conundrum there.

With the UK’s measures in place, Help to Buy, Funding for Lending etc I would be using my Euros to buy what looks safer ie UK property for the next 2-3 years. (a) It’s a rising market with limited supply. (b) A strong Euro means UK property is more attractive as you buy more Stg. (c) Transaction costs don’t kill the deal for buying and selling certainly up to £250k, and even up to £500k.

Thank you Angie, there are several graphs there and they help illustrate my point.

The first graph “house price index” shows nominal prices measured in the local currency. If you zoom into 2008 – 2013 using the slider at the bottom, you should see that UK nominal house prices (for example) dipped in 2009 then recovered and have been pretty steady since 2010. Now compare them to Japanese house prices over the same period and you should see that Japanese nominal house prices have fallen steadily.

Now click on the next tab called “Prices in real terms” and it shows a different story since 2010. In the UK real house prices have been steadily falling, but look at Japanese real house prices. They have also fallen but in real terms they have fallen by less than those in the UK.

The difference is that the “prices in real terms” take into account inflation, and the UK has had more inflation over the same period than Japan.

So which is the better comparison? The nominal house price index or the house prices in real terms? Well I think it’s the house prices in real terms that paint a clearer picture because they strip out inflation, i.e. fluctuations in the value of the currency compared to various consumer goods. Another way of taking inflation into account is to strip out fluctuations in the value of the currency compared to other currencies, i.e. measure house price changes in the same currency.

-

October 9, 2013 at 6:09 pm #118418AnonymousParticipant

Chopera you should also include that almost all nations have chsnged their ways to measure inflation. Its understating it these days. So in real terms those numbers would be higher

-

October 9, 2013 at 8:35 pm #118420ChoperaParticipant

@Ardun wrote:

Chopera you should also include that almost all nations have chsnged their ways to measure inflation. Its understating it these days. So in real terms those numbers would be higher

Yes there’s a lot of smoke and mirrors when it comes to inflation. In theory and in isolation, inflation simply depends on the amounty of money in circulation in an economy. The more money in peoples’ pockets (either via lending or via money printing) the more inflation there will be. And similarly if there’s more money in a particular currency in circulation then that currency will devalue against other currencies. At first glance people think “so what”, it doesn’t matter if things are more expensive if I’ve got more money in my pocket to pay for them. And they especially like it if they have debts, since debts generally get devalued by inflation. However this encourages people to keep taking on more debt and a bubble is created.

However inflation isn’t measured in terms of the amount of money in circulation but rather the price of certain goods. In the UK at least they don’t include the price of what for most people is the most expensive good (houses) so the housing boom went rather unnoticed in the inflsation figures (which I think is the point you want me to make). Furthermore a lot of the goods are imported. Which means inflation measurements are influenced by the economic policies of other countries, and not just the amount of money in circulation. What has happened in the UK over recent years is imported inflation, but there hasn’t been much monetary inflation. There was plenty of money printing, but that money so far hasn’t found its way into the UK economy (the banks hoarded QE money rather than lending it out) however the pound devalued against other currencies and the prices of imported goods went up. This meant that things became less affordable – prices went up, but not because people had more money in their pockets. This isn’t the type of monetary inflation that devalues debts either. This is also why the UK government has been so keen to get banks lending again.

-

October 9, 2013 at 8:47 pm #118421katyBlocked

In spite of all that above the UK is doing considerably better than most eurozone countries. I thought you didn’t want to talk about the UK…it is a Spanish Property Forum after all 😆

-

October 10, 2013 at 7:50 am #118422ChoperaParticipant

@katy wrote:

In spite of all that above the UK is doing considerably better than most eurozone countries. I thought you didn’t want to talk about the UK…it is a Spanish Property Forum after all 😆

I have happily talked about the UK economy compared to the eurozone on threads dedicated to that subject, including threads where you have butted in and accused them of being boring, which is indeed what you are being right now.

-

October 10, 2013 at 7:58 am #118423zoroParticipant

Firstly you said:

@Chopera wrote:You report price fluctuations in international commodities in the same currency, and if you are reporting on international house prices you should also stick to the same currency .

And then you said:

@Chopera wrote:I have made absolutely no comment on how prices should be reported. .

Oh really?

So it seems I mistakenly thought you were commenting on the meaning of the Knight Frank statistics when in fact you were commenting on something else entirely i.e. an imaginary report on the “true” value of property as opposed to the actual prices. Got it!!! I think I’ll leave it there 😆

-

October 10, 2013 at 8:29 am #118424ChoperaParticipant

@zoro wrote:

Firstly you said:

@Chopera wrote:You report price fluctuations in international commodities in the same currency, and if you are reporting on international house prices you should also stick to the same currency .

And then you said:

@Chopera wrote:I have made absolutely no comment on how prices should be reported. .

Oh really?

So it seems I mistakenly thought you were commenting on the meaning of the Knight Frank statistics when in fact you were commenting on something else entirely i.e. an imaginary report on the “true” value of property as opposed to the actual prices. Got it!!! I think I’ll leave it there 😆

The second comment relates to how prices should be reported in isolation, i.e. how they should be published in each country. I have made no criticism of house prices being reported in local currencies. The first comment relates to how international prices should be compared. I’ve said this half a dozen times on this thread.

BTW Have you read my response regarding the Economist graph Angie posted? Can you see how house prices comparisons can be extremely misleading if you don’t take into account things like inflation and currency fluctuations? Can you see that one graph shows UK prices “doing better” than Japan over the last 5 years while the other shows them doing worse?

-

October 10, 2013 at 9:15 am #118425angieBlocked

In reality the property markets of Spain and the UK are completely different, they can’t be compared. I don’t believe the Euro is what they are valued in, in which case, those with Euros knowing the currency is 20-25% higher than Sterling, should be snapping up UK property as it is a rising market for now, plus again the transaction costs are so much lower and have to be taken into account. I’ve given 3 examples of our property purchases in the UK over this period and our funds have risen considerably and tax free.

The UK property market has been far more stable than most EU countries over this period IMO 🙄

Graphs can be difficult to follow, but using this graph, only 3 countries have bucked the steady trend upwards of property prices, South Africa still booming alone, Spain and Ireland boom and bust, all the others appear to have risen (or flatlined) with normality without the massive falls, this isn’t to say that some are still overvalued compared to rents.

Personally still have to agree with Zoro and katy there chopera, I look at things in hard cash, the currency I use, also Japan doesn’t come into my equation there 🙄

-

October 10, 2013 at 9:45 am #118426katyBlocked

@Chopera wrote:

@katy wrote:

In spite of all that above the UK is doing considerably better than most eurozone countries. I thought you didn’t want to talk about the UK…it is a Spanish Property Forum after all 😆

I have happily talked about the UK economy compared to the eurozone on threads dedicated to that subject, including threads where you have butted in and accused them of being boring, which is indeed what you are being right now.

So you have, (talked about the UK economy). Why did you then post

And even if you still insist on ignoring what this thread is about and instead harping on about UK house prices and what Britons need to know (even though this is a Spanish property forum)

Is it only yourself who is entitled to talk about the UK. What you find boring is that your reasoning was being questioned 😆

-

October 10, 2013 at 11:36 am #118428ChoperaParticipant

@angie wrote:

In reality the property markets of Spain and the UK are completely different, they can’t be compared. I don’t believe the Euro is what they are valued in, in which case, those with Euros knowing the currency is 20-25% higher than Sterling, should be snapping up UK property as it is a rising market for now, plus again the transaction costs are so much lower and have to be taken into account. I’ve given 3 examples of our property purchases in the UK over this period and our funds have risen considerably and tax free.

This is exactly what happened to the London market – you missed the stories about Greeks buying up London property in their rush to get their cash out of Greece? Taking advantage of the collapse in sterling? Along with a whole host of other foreign buyers? I also posted on here several times how expats in Spain trying to sell their Spanish property to move back to the UK could have taken advantage of the collapse in sterling, slashed their asking price by 30%, sold and moved back to the UK with no real loss in terms of pounds. With the subsequent rise in sterling they would have got their money back relative to the euro as well. There was an obvious escape route there but they missed it. Their loss, not mine.

Personally I agree that UK property is looking a buy right now – which is fine by me as I have a lot more invested in UK property than I do in Spanish property. Personally I’m investing in UK equities this year (I already mentioned that on this forum as well) but all of this is irrelevant. I’m talking about how house prices should be compared, I didn’t given any opinion on where each market was heading – I made no predictions. To illustrate the issue about using different currencies I happened to compare the UK market with the Spanish one as I thought that most relevant to this forum, but I could have picked any two markets measured in different currencies to illustrate my point (the Japanese one turned out to be a better example). However it seems some posters on this thread are incapable of looking at this objectively – the example I chose implied that the UK market might not have performed as well as the initial graph implied, when compared to other markets, and suddenly they feel the need to talk up the UK market.

@angie wrote:

The UK property market has been far more stable than most EU countries over this period IMO 🙄

Graphs can be difficult to follow, but using this graph, only 3 countries have bucked the steady trend upwards of property prices, South Africa still booming alone, Spain and Ireland boom and bust, all the others appear to have risen (or flatlined) with normality without the massive falls, this isn’t to say that some are still overvalued compared to rents.

Personally still have to agree with Zoro and katy there chopera, I look at things in hard cash, the currency I use, also Japan doesn’t come into my equation there 🙄

You don’t take inflation into account? You think that if a market rises by 10% and yet there is inflation of 20% then that market has performed well? And once again, I used Japan to illustrate a point about how house prices should be compared – even though you have no interest in Japanese house prices, surely you have the mental ability to use them to understand a point. I have no personal interest in the Weimar repuplic or in Zimbabwe either, but I’m still able to look at what went on there to improve my understanding of economics. And besides, you posted the graph, I just went with it. And yet again, I’m not disputing where markets are heading, I’m only debating how they should be compared.

-

October 10, 2013 at 11:47 am #118429ChoperaParticipant

@katy wrote:

@Chopera wrote:

@katy wrote:

In spite of all that above the UK is doing considerably better than most eurozone countries. I thought you didn’t want to talk about the UK…it is a Spanish Property Forum after all 😆

I have happily talked about the UK economy compared to the eurozone on threads dedicated to that subject, including threads where you have butted in and accused them of being boring, which is indeed what you are being right now.

So you have, (talked about the UK economy). Why did you then post

And even if you still insist on ignoring what this thread is about and instead harping on about UK house prices and what Britons need to know (even though this is a Spanish property forum)

Is it only yourself who is entitled to talk about the UK. What you find boring is that your reasoning was being questioned 😆

Your latest posts haven’t been questioning my reasoning, they’ve been a pathetic attempt to change the subject at hand because you either don’t understand the subject or you don’t have the guts to accept that I had a point all along.

-

October 10, 2013 at 2:24 pm #118430katyBlocked

My latest posts have asked you why you said I was

” harping on about UK house prices and what Britons need to know (even though this is a Spanish property forum)”

You brought up the UK as an example of your flawed calculations. I shall say again. if you are going to bring up the UK. then be sure follow on posts will quote the same. I also find it very boring since you joined in with you supposed economic theories about the UK I suggest you read Zoros posts again and then quit harassing me 😈 😈

-

October 10, 2013 at 3:11 pm #118431angieBlocked

I do take inflation into my equation chopera, on a personal level my finances are up well over UK (the one I’m interested in) inflation rates despite you saying that UK property prices had fallen 20% or more in euro terms, however I think many of us don’t reckon property is calculated worldwide in euros 😕 Just out of interest chopera, supposing STG one day went back to 1.50-1.64 euros, would you consider that your Spanish properties were worth less than they already have fallen already using your same analogy for UK property?

I’ve often said that Brits who bought in Spain when we did could recover much of their perceived loss in property value if they converted back to STG, so not such bad news for them.

TBH even I didn’t know why you first mentioned UK prices which has led on to this debate, but you should be pleased that you have more invested in UK property than in Spanish property especially during the last 5 years or so. I posted the graph to show how most markets appear to have risen steadily and evenly in many countries it mentions, but not so in Spain and Ireland, nor South Africa which has shown not to crash, yet! 🙄

I need a stiff drink and a diploma in economics someone 😛

-

October 11, 2013 at 12:28 am #118433AnonymousParticipant

To me it just seems a lot of you are being extremly hostile against Chopera. In this thread he has behaved in a good way and argued his case well.

-

October 11, 2013 at 8:36 am #118434angieBlocked

Ardun, I’m just putting my case, you know, debating, and I think he and I just see things differently on this topic, sometimes we agree on things, sometimes not, like you do too 😕 You have exaggerated your quote ‘a lot of you’ 😕 🙄 I did have a few good glasses of red wine (Spanish) though 8)

-

October 11, 2013 at 9:59 am #118436katyBlocked

@Ardun wrote:

To me it just seems a lot of you are being extremly hostile against Chopera. In this thread he has behaved in a good way and argued his case well.

Everyone is entitled to an opinion, it is not being hostile to refute it. He brought the hostility in to the debate by accusing me of harping on about the UK when he himself had brought up the UK into the debate. Anyway as he says he is bored with it now and so bloody well am I

-

October 11, 2013 at 3:17 pm #118438AnonymousParticipant

Same same have a great weekend;).

-

October 11, 2013 at 4:36 pm #118440angieBlocked

Samma samma har en stor helg ❗

-

October 14, 2013 at 11:34 am #118457zoroParticipant

@Ardun wrote:

To me it just seems a lot of you are being extremly hostile against Chopera. In this thread he has behaved in a good way and argued his case well.

Yes, he has, except that he seems to have confused “price” as used in the title of this this thread, with VALUE.

The report that kicked off this thread is an objective report and simply measures price increases in percentage terms in each country during the period specified and therefore MUST use the currency in which the houses were priced. If the report had been directed at Americans or Germans then maybe for the sake of convenience they would have used USDs or EURs and stated the exchange rates used but they didn’t. There’s an end to it.

If on the other hand the discussion is about value then that would have been a subjective report and it’s perfectly legitimate to throw in any number of variables you want e.g. currency fluctuations, inflation and if you want to go on you could add taxes, interest rates, insurance costs etc. etc. to demonstrate, in the author’s opinion, which market has shown the variation in value.

-

October 28, 2013 at 5:37 am #118568The AustralianParticipant

From the Financial Times:

%22%20transform%3D%22translate(1.2%201.2)%20scale(2.30469)%22%20fill-opacity%3D%22.5%22%3E%3Cellipse%20fill%3D%22%230d07a7%22%20cx%3D%22124%22%20cy%3D%22163%22%20rx%3D%2291%22%20ry%3D%2291%22%2F%3E%3Cellipse%20fill%3D%22%239e720b%22%20rx%3D%221%22%20ry%3D%221%22%20transform%3D%22matrix(14.0306%20-27.26851%2055.29516%2028.45128%20175.7%2057)%22%2F%3E%3Cellipse%20rx%3D%221%22%20ry%3D%221%22%20transform%3D%22rotate(124.6%2023.5%2021.4)%20scale(185.04416%2050.06878)%22%2F%3E%3Cellipse%20rx%3D%221%22%20ry%3D%221%22%20transform%3D%22matrix(-8.89364%20-24.97624%2037.51537%20-13.35862%20108%20154.2)%22%2F%3E%3C%2Fg%3E%3C%2Fsvg%3E)

-

October 28, 2013 at 9:33 am #118569AnonymousParticipant

Aussie, thanks for the chart, but I wouldn’t pay it too much attention. FT, The Economist, etc. all base their charts on official Spanish house-price figures, which are pie-in-the-sky. In reality Spanish house prices are down 50pc or more.

-

-

AuthorPosts

This is a Spanish property forum not an international investors forum

This is a Spanish property forum not an international investors forum

- The forum ‘Spanish Real Estate Chatter’ is closed to new topics and replies.