Spain’s housing market is booming, but compared to Portugal it still looks relatively grounded. If there’s a genuine property bubble forming in Southern Europe, the latest evidence suggests Portugal is the more likely candidate.

After years of rapid house price growth across Southern Europe, concerns about overheating are starting to grow. But while Spain often gets dragged into discussions about tourism, foreign buyers, and affordability pressures, the data increasingly suggests Portugal is in a league of its own.

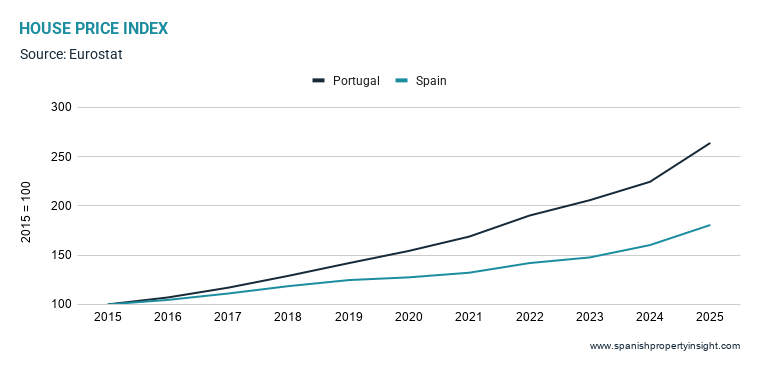

The latest European house price figures for Q4 2025 show Portugal with the strongest growth in this comparison of European markets: prices up almost 19% year-on-year and an extraordinary 73% over the last five years. Spain, by comparison, is up a still-hefty but far more moderate 46% over the same period.

According to a recent European Commission report on housing in the EU (“Housing in the European Union: Market Developments, Underlying Drivers, and Policies,” published by the European Commission’s Directorate-General for Economic and Financial Affairs), Portugal is now estimated to have the most overvalued housing market in Europe, with prices around 35% above what the Commission considers fair value (according to press reports).

Portugal’s housing market looks stretched

The Commission identifies several drivers behind Portugal’s runaway prices:

- Tourism and short-term rentals

- Foreign investment

- Institutional investors

- Weak construction supply

- Bureaucratic planning delays

- Extremely low levels of public housing

Spain faces some of those same pressures, particularly in hotspots like Barcelona, Málaga, Ibiza, and parts of the Costa del Sol. But Portugal appears far more exposed.

The scale of price growth alone tells the story. Portuguese prices have surged at a pace more associated with boom markets in Eastern Europe than mature Western European economies.

Meanwhile, Portugal’s housing politics are becoming increasingly tense. Rising rents, affordability protests, political pressure, and demands for more intervention are all signs of a market under strain. Of course, the same is true of Spain, though to a lesser extent.

That combination—rapid price inflation, political backlash, and mounting affordability problems—is often what late-cycle property booms look like.

Spain still looks comparatively balanced

That doesn’t mean Spain is cheap, or risk-free. Far from it.

Some Spanish markets are clearly expensive by historical standards, especially Madrid, the Balearics, Marbella, and prime Barcelona. Overtourism and short-term rentals are also contributing to housing tensions in certain areas.

But nationally, Spain still looks more balanced than Portugal for several reasons.

First, Spain has a much larger and more diversified housing market. Portugal is a relatively small market where international demand can distort prices much more easily.

Second, Spain still has considerably more housing stock and development capacity than Portugal, even if construction remains below what the country needs.

Third, Spain’s price growth, while strong, has not detached from economic reality to the same degree. Wage growth, population growth, tourism demand, and foreign buyer interest all help explain the market’s resilience.

And finally, Spain simply offers more choice.

For foreign buyers looking for lifestyle property, Spain provides a huge range of coastal, urban, rural, and island markets at very different price points. Portugal, by contrast, has become increasingly concentrated around a relatively small number of high-pressure locations like Lisbon, Porto, and the Algarve.

Could Portugal’s problems benefit Spain?

Potentially yes.

If buyers begin to perceive Portugal as overheated, overpriced, or politically unstable from a housing perspective, some demand may rotate back towards Spain.

That is particularly relevant for northern European buyers looking for second homes or retirement properties. Spain increasingly looks like the safer relative bet: still desirable, still growing, but not yet displaying the same degree of apparent overvaluation flagged by the European Commission.

In that sense, Spain may currently occupy the sweet spot in Southern Europe’s property cycle: strong enough to outperform much of Europe, but not yet so overheated that alarm bells are ringing in Brussels.