Keen to lend mortgages again, Spanish banks are fighting for the most creditworthy borrowers with ever cheaper mortgages, which should help stimulate demand for housing.

In the depths of the Spanish economic crisis, which was underpinned by a spectacular property bust, banks would only lend Spanish mortgages to buyers who were taking over one of their repossessed properties, and even then the rates weren’t great. Spanish lenders were being squeezed by write downs, over-exposure to real estate, and limited access to capital.

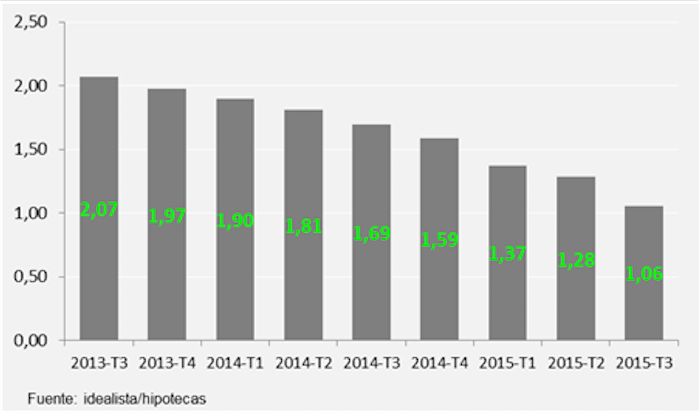

How times change. Spanish banks are desperately keen to lend to mortgage again, as can be seen from the dramatic way that differentials have plunged in the last two years.

Research by the Spanish property portal Idealista.com, based on its own Spanish mortgage business, shows that the differential Spanish lenders charge on new mortgages, the difference between the mortgage rate and the Euribor base rate, which is also the lender’s gross margin, has shrunk from an average of 2.07% in the third quarter of 2013, to 1.06% today (see chart above). So mortgage rates have come down by around 50% in two years, at least according to data provided by Idealista (who claim to get better rates than other mortgage service providers).

Banks are under pressure to increase their income from mortgage lending, at a time when the overall value of mortgage loans is still falling thanks to repayments and writedowns. That means banks are watching their mortgage loan income fall, which has sparked off a price war for market share in the new loans business.

One lender – the Dutch bank ING – has just launched the cheapest variable rate mortgage in the market, with a differential of just 0.99% above Euribor.

Not only are mortgage costs falling; property prices have also fallen dramatically since the Spanish property bubble burst in 2007, in many cases by 50% or more. So buyers using mortgage financing today get the benefit of cheaper mortgages and lower property prices, all of which might help lift the property market in Spain.

However, cheap differentials are not the whole story when it comes to working out the cost of a mortgage. Borrowers also need to look at the cost of other products that lenders try to bundle up with mortgages, such as insurance and banking services. These can sometimes bump up the cost of a mortgage substantially.

Neil says:

Are mortgages generally very portable in Spain? I have had a mortgage with Santander for nearly 10 years, and was under the impression that I can’t really shop around for a deal like we can in the UK ? False perception or reality? appreciate comments. Thanks.

Mark Stücklin says:

Neil, the mortgage market in Spain is nothing like the UK. A mortgage here is basically for the duration. Switching costs are high, and the savings you might make take years to offset the costs of change. Spanish lenders aren’t interested in taking over someone else’s risk. It’s an uncompetitive market, which is how the lenders like it. You can shop around, but I doubt you will find a deal that makes it worth it. Please let me know if you try and find out different.

Julian says:

Hello Mark, what about additional borrowing? We have been with BBVA for 7 years but in that time have completely redeveloped property using only our own funds. Taking your point above about switching not being common in Spain does the same apply to remortgaging?

Mark Stücklin says:

Julian, remortgaging should be easier, but they always hit you with costs.