The empty pipeline of new homes is to blame for the crash in new home sales, claims the Spanish Association of Builders and Developers (APCE in Spanish). And banks refusing to finance developers are to blame for the lack of new projects.

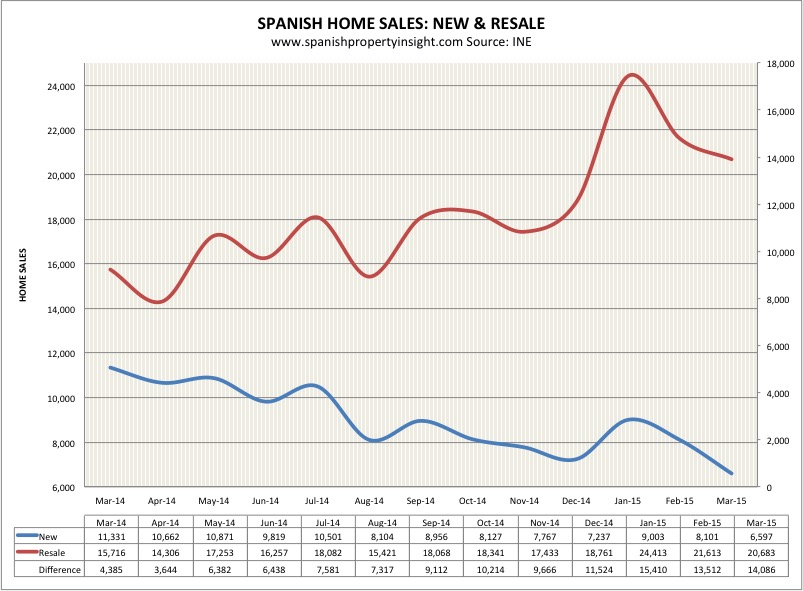

The number of new homes sales recorded in the Property Registry for March was down 42 per cent over 12 months, according to the latest Spanish property market figures from the National Institute of Statistics (INE). New home sales have been in freefall for the last year or more.

“It’s highly likely that there are fewer sales because there are fewer developments being started,” said Carolina Roca (pictured), a representative of the APCE executive committee, and vice-president of the Madrid developers’ association Asprima, in comments to the Spanish press.

Roca says that during 2014, construction began on less than 35,000 properties in Spain, arguing that “we’ve had the brakes on for too long” during the long slump in residential development.

Pointing out that resale transactions are rising fast (up 32 per cent in March according to the INE’s figures) Roca argues the real reason why new home sales are collapsing is because developers can’t get financing to start new projects. “If new builds aren’t started but resale properties are being sold it’s because developments have financing difficulties,” she said.

Developers report that, although banks are now starting to lend mortgages to homebuyers again, they still won’t lend development mortgages to promoters trying to get a new scheme off the ground.

Thanks to the lack of financing available, Roca is gloomy about the prospects for developers in the near term. Banks still have too much exposure to development loans left over from the boom, she says.

That means the supply of new developments for sale in Spain will remain constrained for some time to come, creating an interesting opportunity for the few developers that do have access to capital.

Commenting on recent data suggesting that Spanish house prices have started to recover, Roca said it was a good sign, but lamented that it market driven by resale transactions “doesn’t create economic activity or generate employment”.

David says:

I think it’s a good thing that Banks are not lending development mortgages to Promoters, this caused a lot of the previous problems, Promoters often went bust, a new Promoter would take over, what was once agreed often changed. I’ve never heard of house building where anyone can be called a Promoter often with no knowledge, other than in the Spanish boom. Then it happened that many developments had legal issues over specifications and cut back on their spend but unfortunate buyers seemed to be locked in with the new Promoter. Another nightmare waiting to happen if it starts again.

Why not registered Developers as in the UK?

Campbell Ferguson says:

Could it not be that the previous height was artificial, recording the portfolio sales as sales of new homes? Now that the bulk of these has gone, there will be an apparent slowdown in sales. However, from my businesses experience we have never had so many instructions for building surveys, which are a guide to the strength of the market for the sale of individual properties.

The statistics need to be looked at in detail in order to avoid opinions being based on inappropriate data.

Bede says:

As SPI simply reports the articles about property and doesn’t usually take a view on them we get the usual conflicting mixed bag of ‘Recovery Boosts Demand’ and ‘Growth Stalls’ articles with a smattering of graphs and statistics than can be in conflict with one another as well. So, what’s to be made of all this? Well, apart from the obvious interested parties like the developers, estate agents, the government and, now, the ‘vulture’ investment funds trying to talk up the market there are some statistics that are more or less reliable (albeit with timing differences) and these show a different picture. One of this week’s articles even mentioned a one month increase in the consumption of cement as evidence of a recovery! Don’t they know that town halls have a flurry of road and pavement relaying immediately prior to local elections and this peters out shortly after the votes have been cast?

The reality is that demand is weak and getting weaker as there is no recovery in employment. The emigration of Spaniards, the conversion of full-time jobs into part-time ones and the people who stop ´signing on´ because they receive no benefits all give the idea that the situation is improving but, in fact , it isn’t. Add to this the decline in average salaries and the reluctance of banks to give high loan-to-value mortgages for all but their own over-priced, repossessed properties and the future still looks bleak. There is a glimmer of hope from foreign buyers, but they make up such a small part of the market and buy where there is such an excess of supply that there will be no new development needed to satisfy this sector. The often repeated ‘recovery’ in the Spanish economy relates almost solely to the tourist and car production, for export, sectors that are helping maintain negligible positive economic growth that barely filters down to lower classes.

I could have posted this reply to any one of this week’s articles and it would be just as valid. But I chose this one as it shows the statistics of the INE that are taken directly from the Property Registry so, although they might be a month out of date, i.e. sales registered in March were probably mostly made in February, they are arguably the best source of information. The main problem, however, is that these stat’s do not separate the sales to investment funds and so they don’t give an idea of what has been bought to live in, to rent or for use as a second home. In short, the number of real people buying houses is less than the statistics show but we don’t know by how much less.

So what is the conclusion to all of this? It’s clear that sales of new homes are still in free-fall although the increasing switch to second-hand properties may signify that there is only the rubbish left to buy – still masses of it, by the way – but the total of new and old is still rumbling along at a rate of about 26,000 properties per month with one month of ‘dead cat bounce’ at the end of last year. There is no recovery in the property sector, nor any signs of one,and, logically, why would a developer risk building something new when the cost of building is higher than the sales value in many cases?

Finally, Ms. Roca’s comment that resale transactions ‘’don’t create economic activity or generate employment’’ is incorrect in the current situation. Whilst new development may do these things the ‘new build’ properties in the above graph are mostly not new at all, but first time sales of properties probably completed several years ago. So these don’t create economic activity or jobs either. At least when someone sells a second-hand property, assuming it’s not a bank repossession, they may go out and spend the money one way or another and put some minor stimulus into a moribund economy.