Variable mortgages in times of ultra-low interest rates seem like a great deal for borrowers, but are they luring people into a false sense of security, and setting the scene for a disaster down the line?

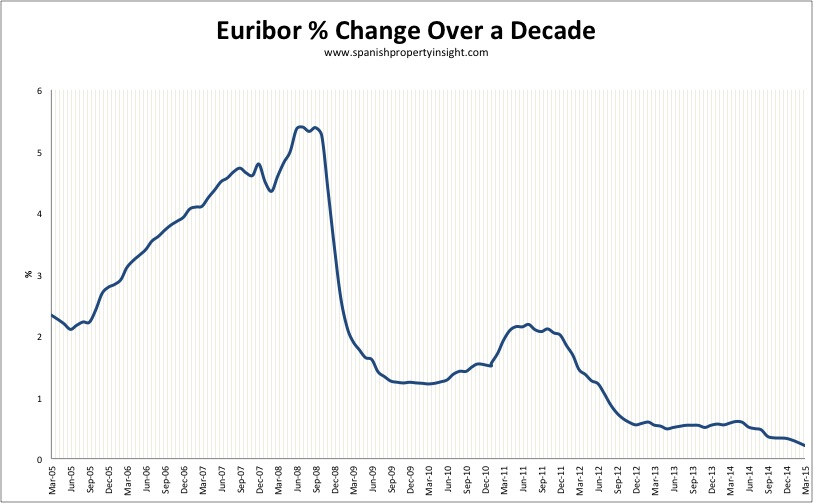

Mortgage interest rates in Spain have never been this low, as illustrated by the chart above. As the European Central Bank (ECB) floods the system with liquidity, Spanish banks are falling over themselves to lend to creditworthy clients, who are now spoilt for choice. But with Euribor at a historic low of 0.177%, some borrowers would be plunged into default if interest rose to a more normal level, not forgetting they rose to 5% in 2008. If that happened again, many families would be unable to make their mortgage payments, reports the Spanish press.

According to the National Institute of Statistics (INE), 92.5 per cent of new mortgages approved in 2014 were variable rate, and just 6.5 per cent were fixed rate. So were Euribor to rise, so would monthly mortgage repayments for the vast majority of Spanish borrowers.

That is exactly what happened in 2008, when Euribor rose to 5.4 per cent, as the ECB tried to cool the asset bubble of the moment. Many Spanish families defaulted on their loans, and saw their homes repossessed. In some cases, monthly mortgage repayment bills rose from €700 to €1,400, and to make matters worse, millions of people started losing their jobs.

Variable-rate mortgages are risky, but that doesn’t seem to deter Spanish borrowers from preferring them over costlier but less-risky fixed-rate mortgages. At a time when base rates are close to zero, Spanish borrowers have saved a fortune on financing costs, and it’s no exaggeration to say this has helped keep many families afloat.

At least there are some signs that borrowers are starting to see the merits of lower-risk fixed-rate mortgages. 7 per cent of borrowers now choose this option, up from only two per cent in 2007.

It helps that banks are starting to offer attractive fixed rate mortgages as low as 2.5 per cent (from Kutxabank). The four best fixed-rate mortgages are already below four per cent, something that was unheard of just a few years ago. That compares to the best variable rates of just under 2 per cent.

Spanish borrowers benefit in times of cheap money, but pay dearly when rates go up. German borrowers, on the other hand, prefer fixed rates with less risk, but pay twice as much as Spaniards, around 3.6 per cent according to research by Bankia, a Spanish lender. Spaniards pay lower rates than German, French, and Italian borrowers, but focus more on variable-rate mortgages with higher risk. In the chart below, Spanish rates are in light green, and German rates in dark Green.

So Germans and other Europeans are more risk-averse, and pay more to borrow, whist Spaniards are more interested in getting the lowest borrowing costs today, even if there is a risk of higher costs tomorrow. It seems that Spaniards tend to look just at the short term when the make their borrowing decisions. Storing up problems for the future.

alan says:

Some mortgage repayments rose from 700 euros to 1400 euros on a 5.4% increase, I don’t quite understand this. Wouldn’t that be a 100% increase? BBVA gave me a list of patients changes according to Euribor rate rises and they are nothing as drastic as this.

Mark Stücklin says:

Alan, thanks for querying this, as I see it’s not very clear. Euribor rose to 5.4% in 2008, an increase of 14% in a year, and 123% in three years. I got the monthly mortgage repayment increase from an article at Idealista (http://www.idealista.com/news/finanzas-personales/hipotecas/2015/04/21/736295-peligro-el-93-de-los-espanoles-estan-pidiendo-hipotecas-con-bomba-de). I assume it was referring to an increase over about that three year period, which would definitely have hammered quite a few household budgets.

GarySFBCN says:

I do agree that this could disaster for everyone if interest rates rise.

When I bought in Barcelona in 2012, it was very difficult to get a mortgage, even though I was paying 40% of the total in cash, had an excellent credit history and solid income. Only 1 bank offered a fixed-rate mortgage and it was 8%, and they quickly withdrew that offer.

Concluding that Spaniards are more interested in lower borrowing costs based upon the number of fixed-rate mortgages may not entirely accurate, especially if fixed-rate mortgages are not available or have such ridiculously high interest on what is cheap money for the banks.