The IMF has published a report on four European housing markets including Spain, concluding that the Spanish property market has bottomed out, but risks remain.

“This report examines the experiences of four European countries that have had large house-price declines in recent years,” explains the introduction to the report. “In particular, it examines the experiences of Denmark, Ireland, the Netherlands, and Spain—four countries in which the house-price cycle has been especially large and that share a similar institutional environment (a common monetary policy and the EU’s institutional framework)—with a view to exploring how policies can best support economic recovery in the wake of a house-price bust.”

“Denmark, Ireland, the Netherlands, and Spain all experienced a large house-price cycle in recent years. Each country experienced a large run-up in house prices during 2000–07, driven in part by easy financial conditions and accompanied by debt accumulation. These booms came to an end around the time of the 2007–09 global financial crisis. Real house prices in all four countries subsequently declined by 25 percent or more (Box 1). House-price declines were largest in Ireland and Spain, in part due to more overbuilding during the boom.“

Compared to past housing busts, real house prices in Spain are below previous trends, private consumption and real fixed investment are way below, but real credit is still way above, though not as bad as the other countries analysed.

Here are the other main findings of the report with regard to Spain, and a link to full report in English for those who want more detail.

- Standard valuation metrics suggest that house prices may have reached or be nearing a trough in the countries analysed

- Low real interest rates justify current valuations, but rates are likely to rise in future, which would put further downward pressure on house prices

- In Spain, a large overhang of vacant houses—especially outside major urban areas—could also cause price-to-rent and price- to-income ratios to undershoot their long-run equilibriums. (Note: outside observers like the IMF don’t realise the stock is mostly in the wrong place, where there is no demand. It’s a problem for bank balance sheets, but not for the market in areas where people want to live.)

- The housing bust has left Spain with the worst output gap of all the countries analysed, and one of the worst gaps in the developed world

- Spain has the lowest debt ratio among the four countries (though the incidence of distress is amplified by Spain’s very high unemployment rate), reflecting in part relatively less saving via pension assets.

- Spain has a high non-performing loan ratio, but not half as bad as Ireland

- Low interest rates in the crisis have helped many Spanish borrowers stay afloat, thanks to Spain’s high prevalence of variable-rate mortgage

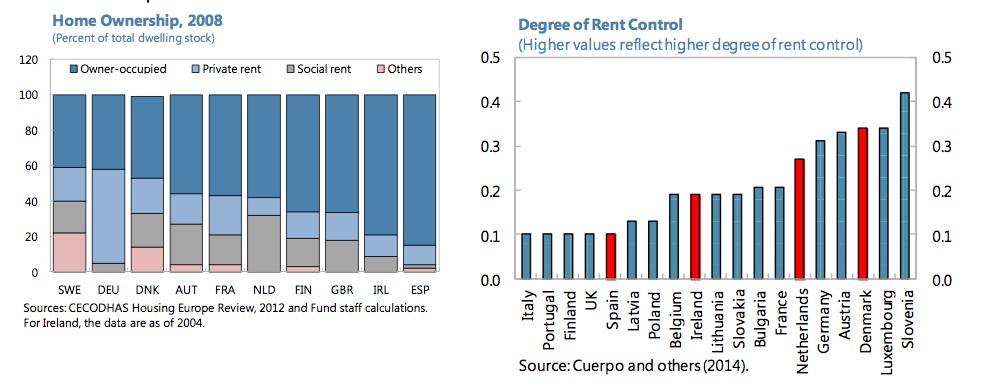

- Spain now scores high on rental market flexibility, whereas rent controls were much more stringent before the crisis. This should stimulate rental demand and reduce the risk of a housing bust in future. That said, Spain is still the country with the highest level of owner-occupiers.

The IMF recommends measures to reduce the output gap, debt overhang, and liquidity constraints, including tax and pension reforms.

IMF MULTI-COUNTRY REPORT

+ HOUSING RECOVERIES: CLUSTER REPORT ON DENMARK, IRELAND, KINGDOM OF THE NETHERLANDS—THE NETHERLANDS, AND SPAIN