The Malaga housing market in 2025, including the West Costa del Sol

Sales

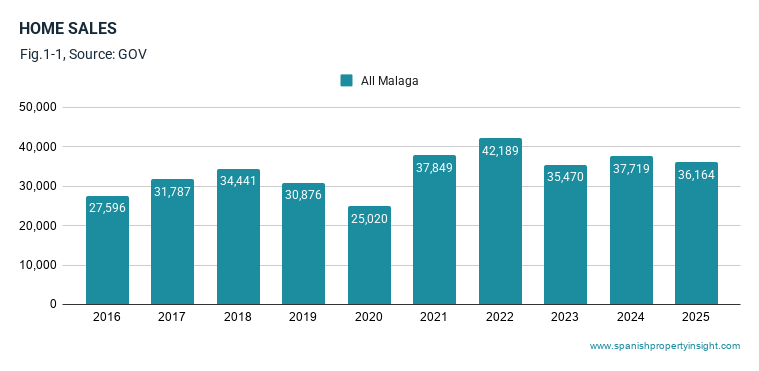

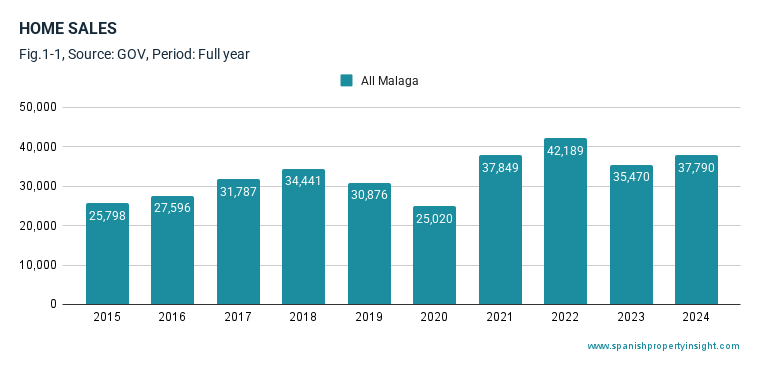

There were 36,164 home sales in Malaga in 2025, a year-on-year change of -4%. Despite this modest decline compared to the previous year, sales remained 10% above the ten-year average, highlighting how activity is still elevated by longer-term standards. Over the last decade the number of transactions has increased by 40%, reflecting the strong expansion of the provincial housing market during this period. As illustrated in Fig. 1-1, Malaga continues to operate at historically high levels of market activity.

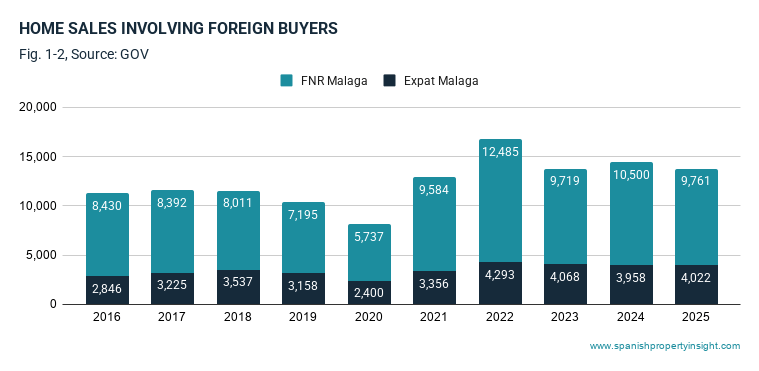

Foreign demand remained a defining feature of the market. There were 13,783 home purchases by foreign buyers, a year-on-year change of -5%. This total includes 4,022 expats (foreigners living in Spain) and 9,761 foreign non-residents (FNR) buying second homes and investment properties. Purchases by expats increased 2% year-on-year, while FNR purchases declined 7%, suggesting some cooling in the second-home segment. Over the past decade, expat purchases have increased 58%, compared with 16% for FNR buyers, indicating stronger long-term growth among foreign residents relocating to the area.

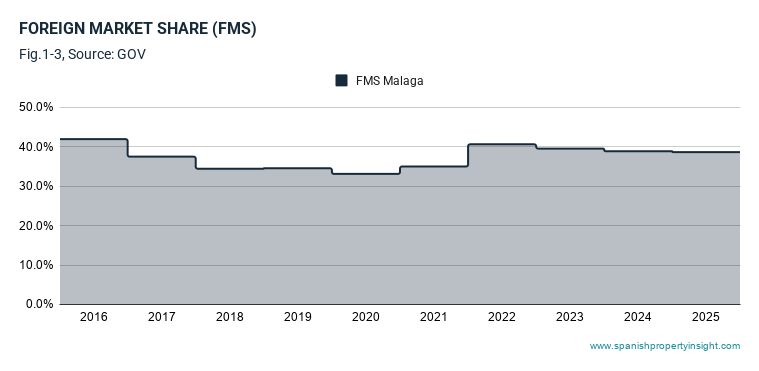

Foreign buyers accounted for 39% of the market, slightly down from 39% a year earlier, but still extraordinarily high by international standards. This sustained level of foreign participation highlights Malaga’s continued appeal to overseas buyers seeking lifestyle, retirement, and investment opportunities on the Costa del Sol. Foreign demand remains a central pillar of the provincial housing market.

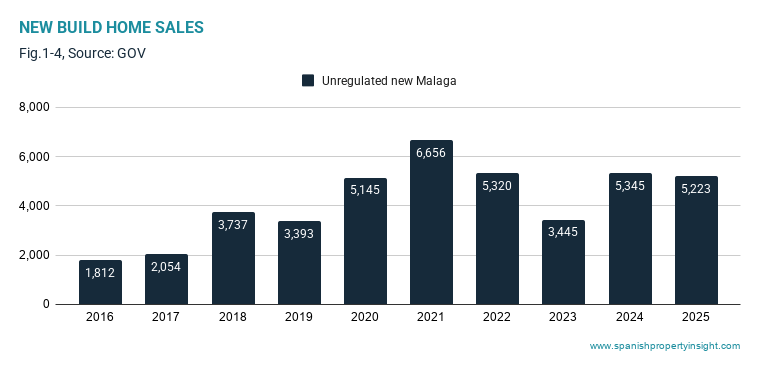

There were 5,223 new-build home sales in the period, a year-on-year change of -2%. Even so, new-build transactions remain 33% above the ten-year average, and have increased by 111% over the last decade. This reflects the growing importance of newly-built housing in Malaga, where strong demand and rising prices have encouraged developers to expand supply.

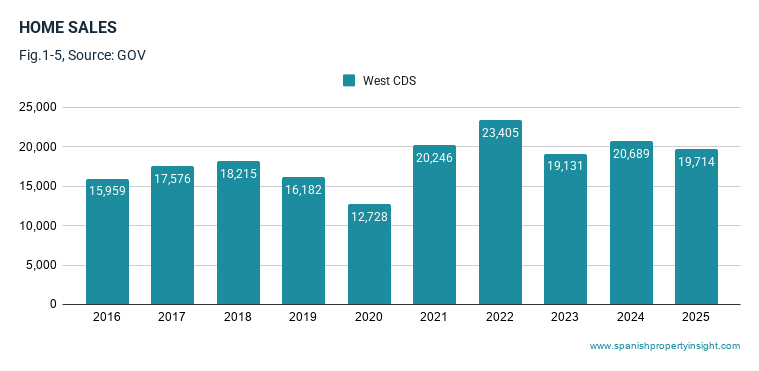

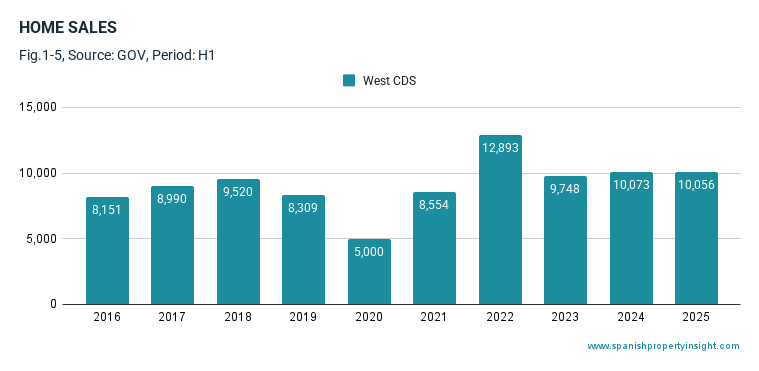

Looking just at sales in the West Costa del Sol municipalities*, there were 19,714 home sales, a year-on-year change of -5% (Fig.1-5). Despite the annual decline, sales in this sub-market remained 7% above the ten-year average, and have increased 24% over the past decade. This highlights the continued structural growth of the western Costa del Sol housing market, which remains one of the most active and internationally driven property markets in Spain.

Prices

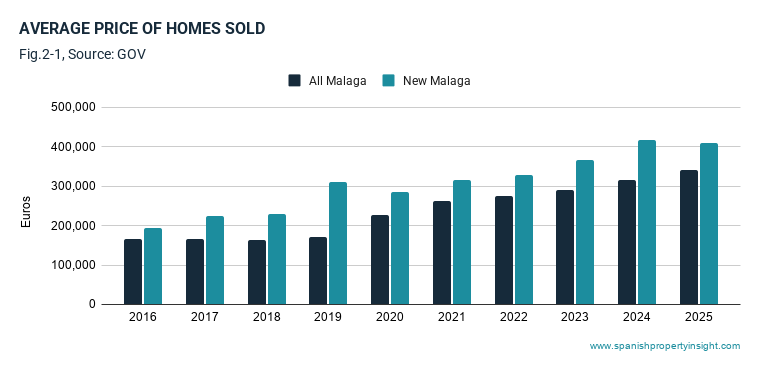

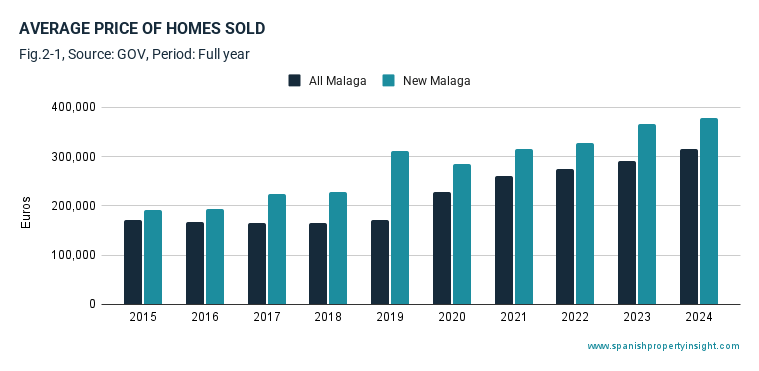

According to figures from the Spanish Housing Ministry, the average price of homes sold in Malaga in the period was €341,638, an annual increase of 8%. By contrast, the average price of newly-built homes was €410,145, representing a -2% year-on-year change. This suggests some stabilisation in the new-build segment after several years of strong growth.

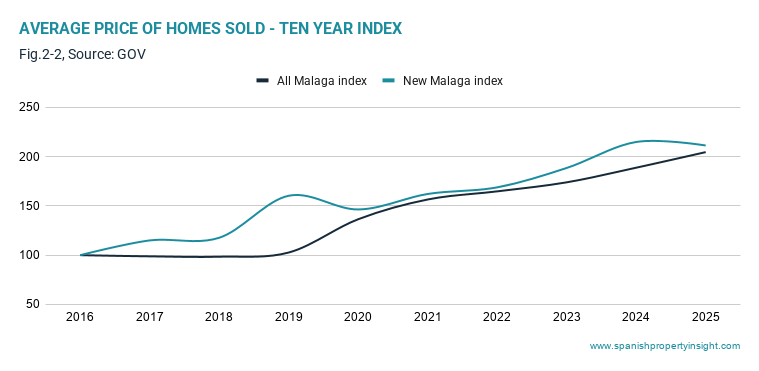

Over the last ten years the price index for all homes has increased from 100 to 205, while the index for new property has risen to 211. Both segments have therefore experienced substantial appreciation, with new homes increasing slightly more overall. Over five years, prices rose 50% for all property and 44% for new homes. The slightly stronger long-term growth of new housing reflects structural factors such as higher construction costs, scarcity of well-located land, and the increasing share of premium developments aimed at international buyers, particularly along the Costa del Sol.

Mortgages and financing conditions

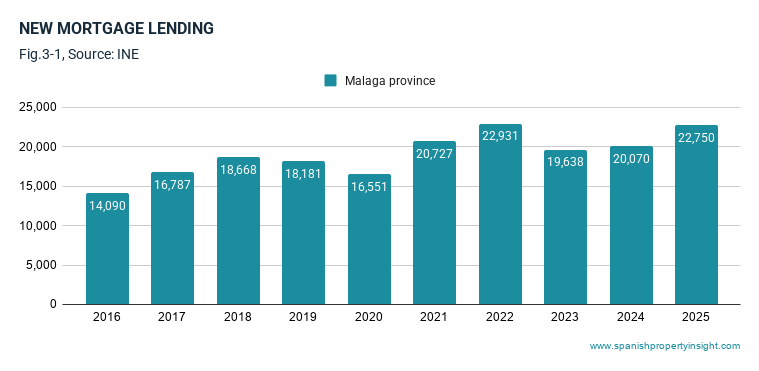

There were 22,750 new mortgages signed in Malaga province during the period, a year-on-year increase of 13%. Mortgage lending was 26% above the ten-year average, and has grown 86% over the past decade, demonstrating the strong expansion of credit supporting housing demand in the province.

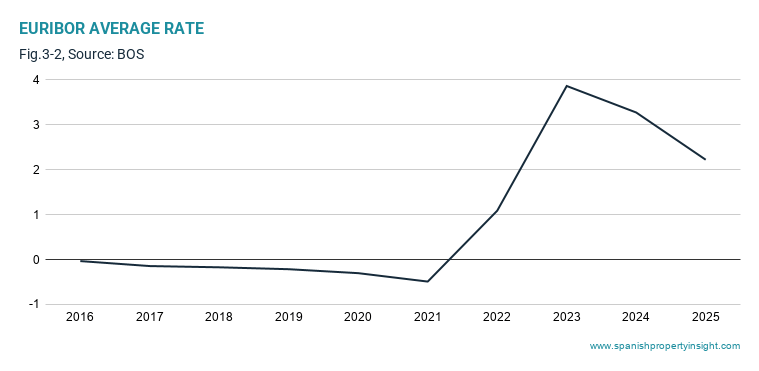

The average Euribor rate during the period was 2.22%, a -32% change year-on-year. Euribor is the benchmark interest rate used for most mortgages in Spain. The current level sits well below the recent peak of 3.86% in 2023, but still far above the historic low of -0.49% recorded in 2021. This suggests borrowing conditions have improved compared to the recent tightening cycle, though they remain more restrictive than during the ultra-low-rate years of the early 2020s. The downward movement reflects easing inflation pressures and the gradual shift in monetary policy expectations for the European Central Bank, with markets anticipating a period of moderate rate cuts rather than a return to the exceptionally low rates seen earlier in the decade.

Housing starts

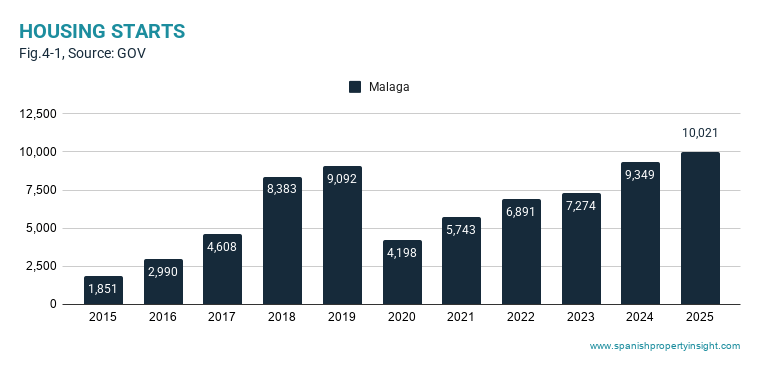

There were 10,021 housing starts in Malaga based on planning approvals, representing a 7% year-on-year increase. Construction activity was 66% above the ten-year average, and has increased by 441% over the past decade. This sharp rise reflects developers responding to sustained demand, particularly from international buyers and higher-income households, though supply still struggles to keep pace with the strongest areas of demand along the coast.

Summary

Overall, the Malaga housing market in 2025 remained robust despite a slight cooling in transaction volumes compared to the previous year. Sales levels remain historically high, foreign demand continues to play a dominant role, and prices have continued to rise strongly over the longer term. Mortgage lending is expanding again as financing conditions gradually ease following the peak in interest rates, while construction activity is increasing to meet demand. Looking ahead, the market’s performance will depend on the balance between sustained international demand, evolving financing conditions, and the ability of new housing supply to keep pace with one of Spain’s most dynamic property markets.

*Municipalities: Benahavís, Benalmádena, Casares, Estepona, Fuengirola, Manilva, Marbella, Mijas, and Torremolinos.

Previous reports

You can read reports from previous periods (if available) by clicking on the buttons below.

West Costa del Sol housing market report: H1 2025

Sales performance

There were 18,360 home sales in Malaga province during the first half of 2025 (Fig. 1‑1), a year-on-year decline of 1%. Compared to the ten-year average, this was an increase of 12%, and over the decade, sales have grown by 32%.

Foreign buyers accounted for 7,103 purchases, a small increase of 0.4% year-on-year (Fig. 1-2).

Compared to the ten-year average, this segment grew by 18%, and over the decade by 21%. By residency:

- 2,104 homes were bought by foreigners living in Spain (expats), up 2% year-on-year.

- 4,999 homes were bought by foreign non-residents (FNR), down 0.3% (Fig. 1‑2).

Over the last ten years, expat purchases have increased by 41%, while FNR purchases are up 14%.

The market share of foreign buyers stood at 39% (Fig. 1‑3), slightly above the same period last year (38%), showing that international demand remains a defining feature of the West Costa del Sol market.

New-build sales reached 2,296 units, up 12% year-on-year (Fig. 1‑4). Compared to the ten-year average, this represents an increase of 27%, and over the full decade, new-build transactions have risen by 72%—highlighting the growing importance of newly constructed homes in the sales mix, especially in areas with limited resale supply.

Looking just at the West Costa del Sol municipalities*, there were 10,056 home sales, essentially flat compared to a year earlier (Fig. 1‑5). That said, this volume was 10% above the ten-year average and up 23% over the decade, indicating long-term strength in the region.

Price trends

According to the Spanish Housing Ministry, the average sale price in Malaga province reached €337,331, representing an annual increase of 7% (Fig. 2‑1). For newly built homes, the average price was €413,350, down 1% compared to H1 2024.

A ten-year index shows overall property prices have risen from 100 to 202, while new-build prices have increased to 213 (Fig. 2‑2). This indicates that resale properties have caught up with or even outperformed new builds in recent years. While new-build prices surged earlier in the cycle, strong demand and limited stock have driven up prices for existing homes, closing the gap.

Over five years, all property prices have risen by 48%, while new-build prices have increased by 45%.

Asking price trends by municipality

Asking prices continue to rise across the West Costa del Sol, according to Idealista (Fig. 2‑3). In H1 2025:

- Marbella: €5,183/m², up 8% year-on-year, and 71% over five years.

- Estepona: €3,861/m², up 12% year-on-year, and 73% over five years.

- Benahavís: €4,997/m², up 10% year-on-year, and 62% over five years.

Over ten years, asking prices have more than doubled in Marbella (+127%), risen by 155% in Estepona, and by 111% in Benahavís—highlighting the long-term appreciation in some of the coast’s most sought-after municipalities.

Mortgage activity

A total of 10,739 new mortgages were signed in Malaga province during H1 2025 (Fig. 3‑1), an increase of 19% year-on-year. This was 20% above the ten-year average and 82% higher than a decade ago—showing ongoing momentum despite recent rate pressures.

The average Euribor rate in the period was 2.27% (Fig. 3‑2), significantly lower than the 2023 high of 3.69% and well above the 2021 low of -0.49%. This sharp drop reflects a shift in European Central Bank (ECB) policy, with rate cuts introduced in the first half of 2025 as inflation came back under control. Markets expect further easing in the second half of the year, which could support additional lending and demand.

Construction activity

There were 5,157 housing starts approved in Malaga province during H1 2025 (Fig. 4‑1), up 6% year-on-year. This figure is 71% above the ten-year average and 621% higher than the low point of 2015, when only 628 starts were recorded.

Although starts have surpassed recent years, they still lag behind pre-pandemic levels, such as 2019 when there were 5,580 new approvals. The industry continues to face challenges related to build costs, labour shortages, and permitting delays, particularly acute in high-demand coastal areas like the West Costa del Sol.

Conclusion

The West Costa del Sol property market remains on firm footing in H1 2025, with steady sales, strong price growth, and improving financing conditions. Foreign demand continues to anchor the market, particularly in premium locations, while the new-build sector plays an increasingly important role. Falling interest rates and strong underlying demand suggest the market may accelerate in the second half of the year, although supply constraints—especially in prime coastal zones—will continue to shape outcomes.

* The municipalities included in this analysis are: Benahavís, Benalmádena, Casares, Estepona, Fuengirola, Manilva, Marbella, Mijas, and Torremolinos.

West Costa del Sol housing market performance in 2024

The Malaga & Costa del Sol housing market in 2024 presented a picture of upbeat stability, underpinned by steady sales, rising prices, and an increasing supply of new developments. However, activity in the mortgage market contracted, reflecting broader macroeconomic factors such as higher interest rates and tighter monetary policy. The following report explores the key market segments and trends.

Sales performance

Home sales in Malaga province (home to the west Costa del Sol) totalled 37,790 in 2024, representing a reasonable year-on-year increase of 7% (Fig. 1-1). This represented a 15% increase over the ten-year average and an overall increase of 46% over the last decade, highlighting sustained long-term growth in the market. It was the second-best year on record for home sales.

Foreign buyers

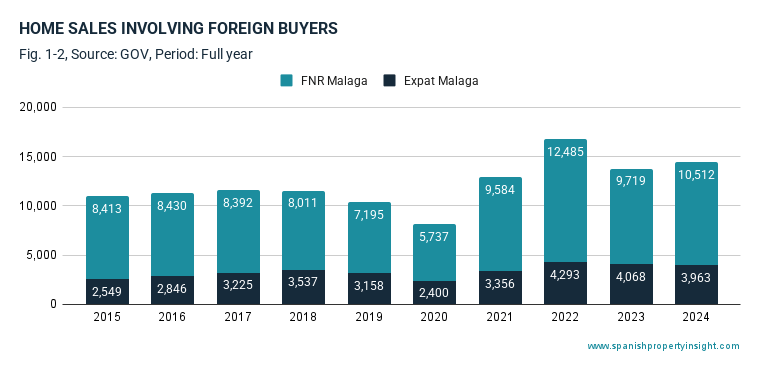

Foreign demand continues to be a crucial driver of housing demand in Malaga. There were 14,475 sales involving international buyers in 2024, up 5% from the previous year. This segment outperformed the ten-year average by 19% and has increased by 32% over the last ten years, reinforcing the province’s position as a leading destination for overseas purchases (Fig. 1-2).

- Of these, 3,963 were by foreign residents (expats), down 3% compared to the previous year but up 55% over the past decade.

- The remaining 10,512 purchases were made by foreign non-residents (FNRs), who typically buy second homes or investment properties. This group recorded an 8% year-on-year rise and a 25% increase over a ten-year period. FNRs are almost two thirds of the foreign market for homes on the Costa del Sol.

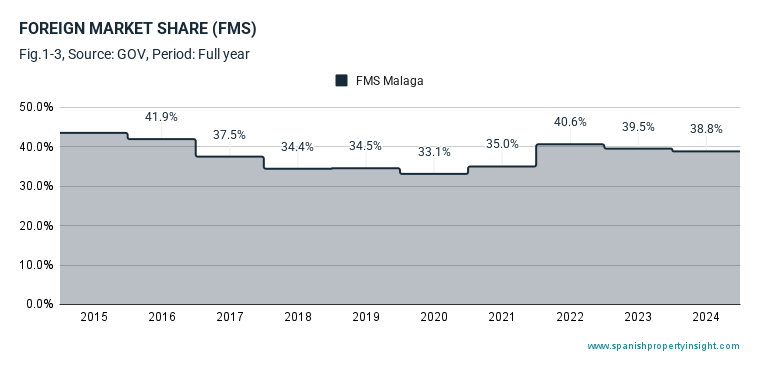

Despite a minor decline in overall market share, foreign buyers still accounted for 39% of all transactions (Fig. 1-3), slightly down from 40% a year ago. This indicates a relative increase in purchases by domestic buyers or a slowing pace of growth among foreign investors. The Malaga province foreign market-share is one of the highest in Spain.

New build homes

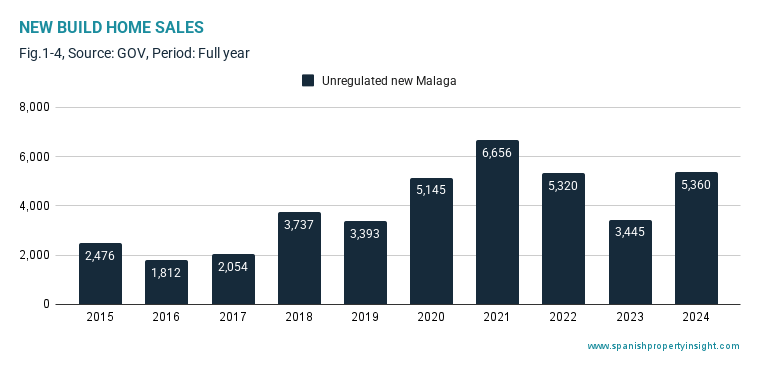

Newly-built home sales saw robust performance with 5,360 units sold in 2024—an impressive year-on-year growth of 56%, and the second-highest sales figures seen in this segment for over a decade (Fig. 1-4). Compared to the ten-year average, new build sales rose by 116%, indicating a major surge in demand for modern housing stock in Malaga province, home to the Costa del Sol.

West Costa del Sol home sales

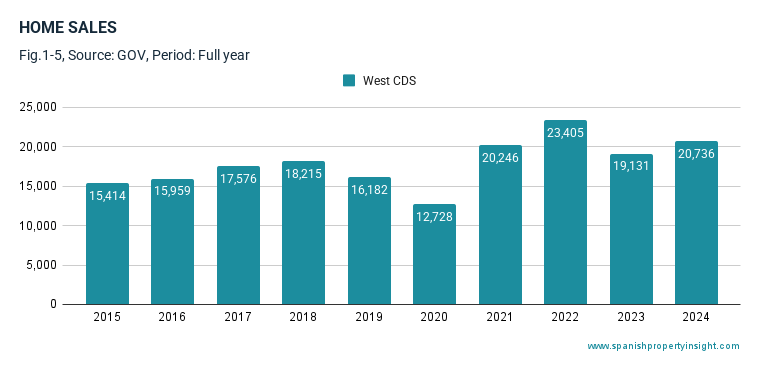

Looking just at home sales in the municipalities* of the west Costa del Sol, there were 20,736 sales—an 8% increase compared to the previous year and a 35% rise over a decade (Fig. 1-5). It was the second-best year on record and 15% higher than the ten-year average, which is a good benchmark for judging the year’s performance.

House price trends

Home prices in Malaga province continued to increase in 2024. The average price of all homes sold reached €315,274, up 9% from the previous year (Fig. 2-1). Newly built homes averaged €378,604, marking a smaller annual gain of 3%.

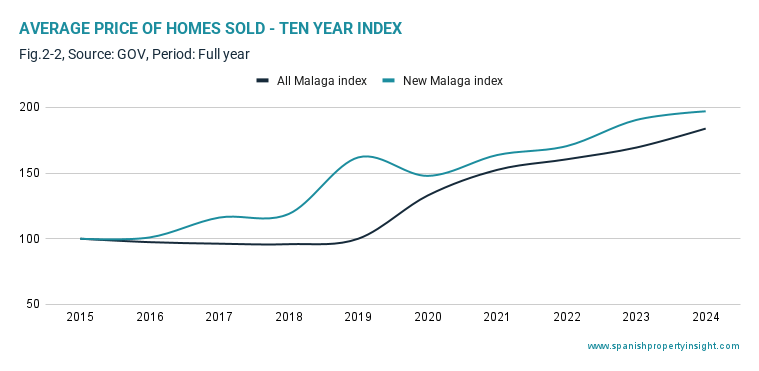

Taking a longer view, price growth has been strong across both property types but significantly higher for new builds. The ten-year price index rose from 100 to 184 for all property types and to 197 for newly built dwellings (Fig. 2-2). This means:

- All property prices have nearly doubled over the last decade (up 84%).

- New build prices have increased by 97% over the same period.

Interestingly, over the last five years, price increases have been more pronounced in the resale segment than in the new build sector. Resale prices rose by 84% compared to just 22% for new properties. This shift may be due to the high base price of new builds in recent years or a narrowing value gap, with buyers increasingly willing to pay premium prices for well-located resales.

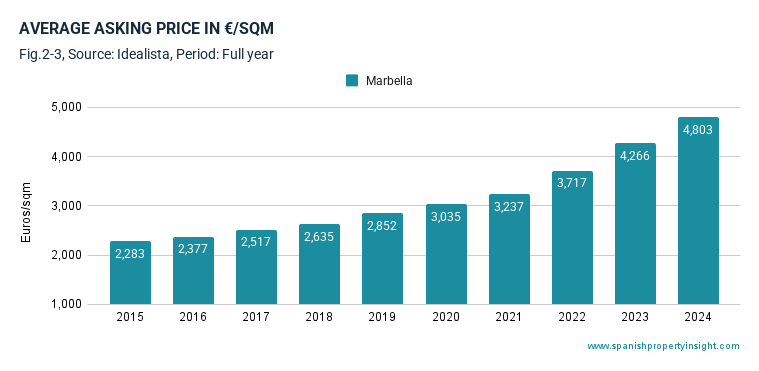

Marbella case study

According to figures from the Spanish property portal Idealista, the average asking price of property for sale in Marbella during the first half of 2024 was €4,803 per square metre, representing an annual increase of 13% (Fig. 2-3). Over the past five years, asking prices have risen by 68%, highlighting strong and sustained demand in the area.

Mortgage market

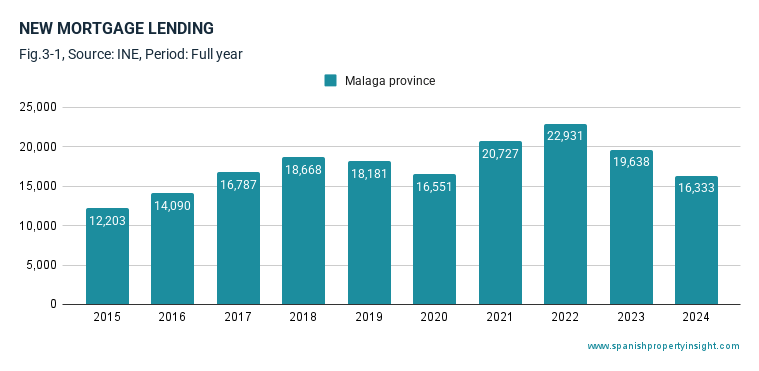

Mortgage activity in Malaga province softened in 2024 in response to higher borrowing costs and tighter monetary conditions. A total of 16,333 new mortgages were signed in the region, down 17% compared to the previous year (Fig. 3-1). Against the ten-year average, mortgages were down by 7%, while the long-run trend remains positive with a 34% increase in the last decade.

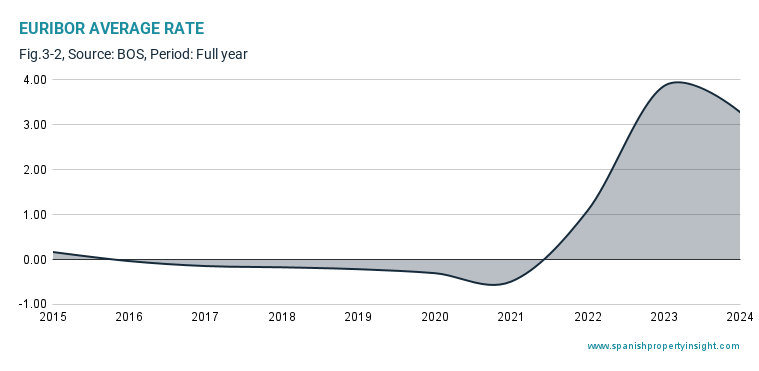

A key driver of the slowdown was the higher Euribor rate, which averaged 3.27% for the year (Fig. 3-2). Although this is slightly lower than the 2023 peak of 3.86%, it still represents a sharp increase from the negative rates seen in 2021 (as low as -0.49%).

The European Central Bank (ECB) began tightening monetary policy in 2022 in response to inflation pressures. With inflation now easing, financial markets expect the ECB to ease rates modestly in the near future, though borrowing costs are likely to remain elevated by historical standards through 2025.

Housing starts

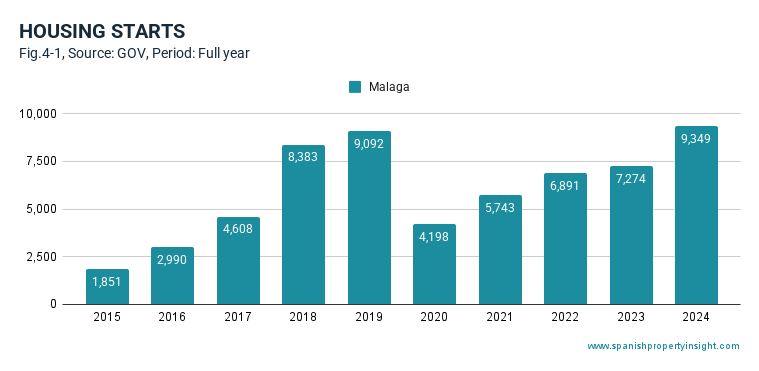

Reflecting developer confidence and robust demand in the new build segment, planning approvals for new housing starts reached 9,349 in 2024 (Fig. 4-1). This is a significant 29% increase over the previous year and 55% above the ten-year average. Over the past decade, approvals have surged fourfold, demonstrating a major rebound in construction activity from post-crisis lows.

This growth aligns with rising demand for modern accommodation, including buyers prioritising energy efficiency, community amenities, and prime locations often found in new developments.

Summary

- Home sales in Malaga rose by 7% to nearly 38,000, with foreign buyers making up 39% of purchases.

- New build sales surged by 56%, boosted by rising demand and a strong pipeline of housing starts.

- Property prices continued upward, rising 9% overall, with new builds commanding a premium.

- Mortgage activity declined by 17% annually due to elevated interest rates.

- Euribor averaged 3.27%, down from the 2023 peak but still historically high.

- Housing starts increased by 29% annually and have grown fourfold in a decade.

Conclusion

The Malaga property market in 2024 remained buoyant, supported by ongoing foreign interest, strong demand for new builds, and long-term price growth. The recent decline in mortgage activity reflects the current interest rate environment, but moderating Euribor levels indicate some relief ahead for borrowers.

Looking forward, Malaga appears well-positioned for continued stability and moderate growth, especially if borrowing conditions ease and international demand remains strong. With new supply expanding to meet demand—particularly in the West Costa del Sol—the market will continue evolving, offering opportunities for both investors and end-users alike.

*The municipalities included in this analysis were as follows: Benahavís, Benalmádena, Casares, Estepona, Fuengirola, Manilva, Marbella, Mijas, and Torremolinos.