Tenerife province housing market: First Half of 2025

Home sales broadly stable but foreign demand weakens further

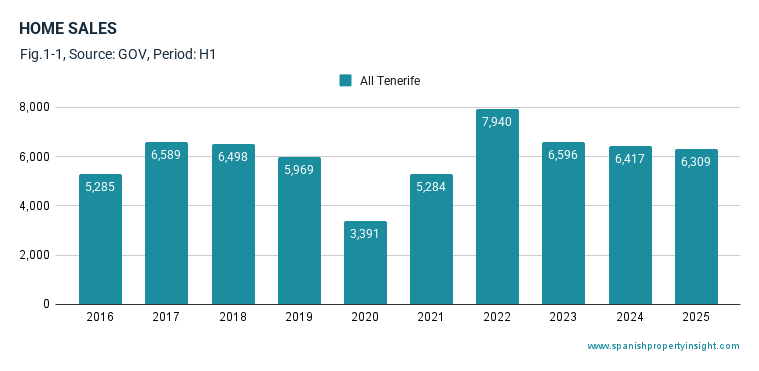

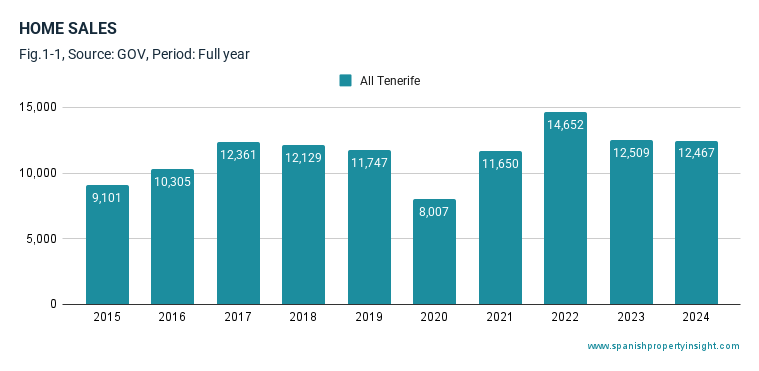

There were 6,309 home sales in the province of Santa Cruz de Tenerife in the first half of 2025, a slight year-on-year decline of 1.7% (Fig. 1-1). However, this result was still 8.2% above the ten-year average and nearly 19.4% higher than volumes a decade ago, confirming a strong long-term trend. Note that the island of Tenerife accounts for more than 90% of sales in the province, and La Palma most of the rest. The small islands of La Gomera and El Hierro play a minor role in the provinces’s housing market.

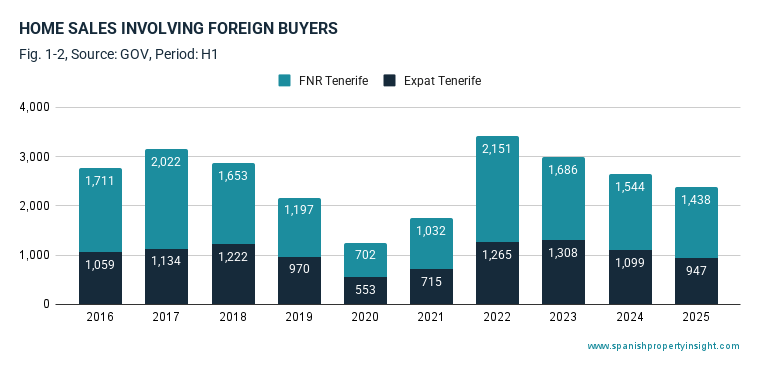

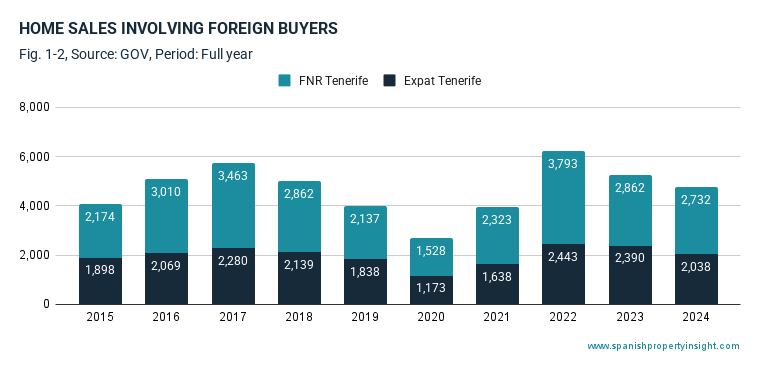

Foreign demand continued to contract more sharply. There were 2,385 sales involving foreign buyers, down 9.8% compared to the same period in 2024, and 13.9% below H1 2015. This total includes 947 expat buyers (foreign residents in Spain) and 1,438 foreign non-residents (FNRs) acquiring second homes or investment properties (Fig. 1-2). Expat purchases fell by 13.8% year-on-year, while FNR demand was down 6.9%. Both sub-segments are well below their peak levels of the past decade.

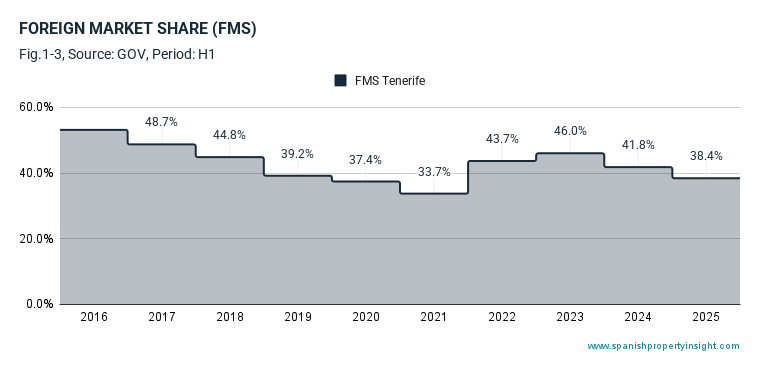

The foreign market share stood at 38.4% in H1 2025, down from 41.8% in H1 2024 (Fig. 1-3). Though still substantial, the data confirm a trend of gradual erosion in international buyer activity.

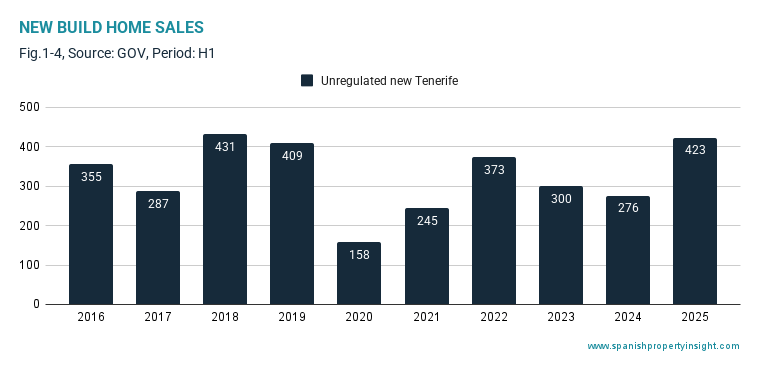

New-build sales were a notable exception, with 423 new homes sold in the period—an increase of 53.3% year-on-year (Fig. 1‑4). Compared to the ten-year average, this was a rise of 33.6%, and sales were 27.8% higher than in the same period a decade ago.

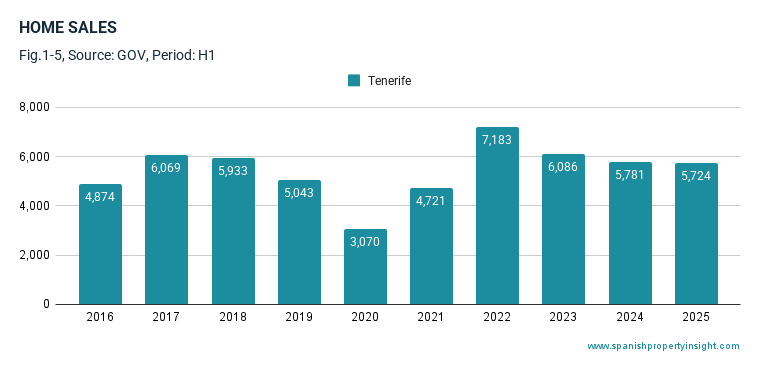

Focusing on municipal-level activity in Tenerife itself (island), there were 5,724 sales in H1 2025, a minimal 1% drop year-on-year, but 17.4% higher than in the same period ten years earlier (Fig. 1-5). Tenerife the island was home to 91% of all home sales in the province during the period.

Prices continue to rise, with new builds commanding a significant premium

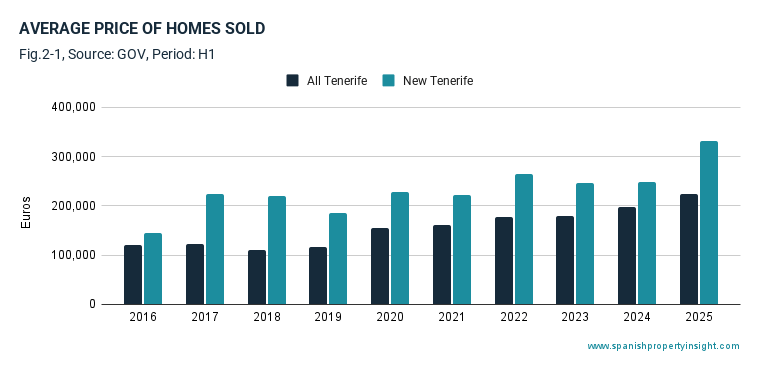

Figures from the Spanish Housing Ministry show that the average price of homes sold in Tenerife in H1 2025 was €223,555, up 12.9% from H1 2024 (Fig. 2-1). Newly-built properties sold for an average of €331,025, a 33.5% increase year-on-year, reinforcing the widening price gap between new and resale stock.

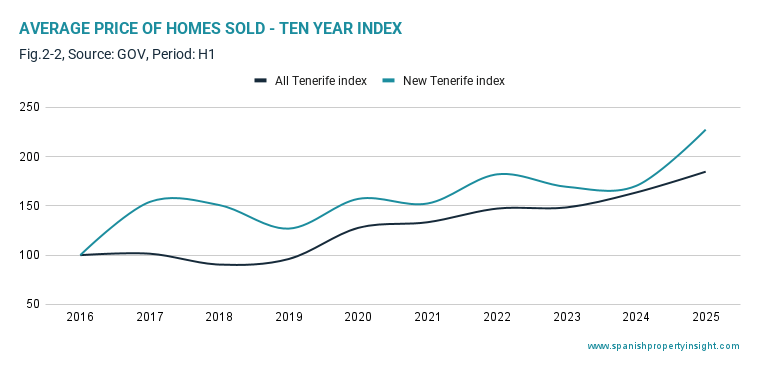

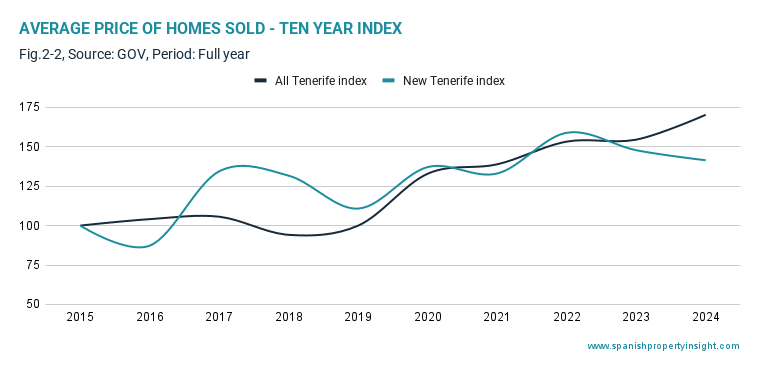

Over the last ten years, the price index for all homes rose from 100 to 192.2, while the index for new homes reached 198.4 (Fig. 2-2). This indicates that new-build prices have almost doubled over the decade—outpacing overall growth—and suggests stronger demand for newer, better-equipped homes, as well as rising development costs.

Five-year growth has been comparable in both segments, with prices up 44.6% for all property and 44.7% for new builds.

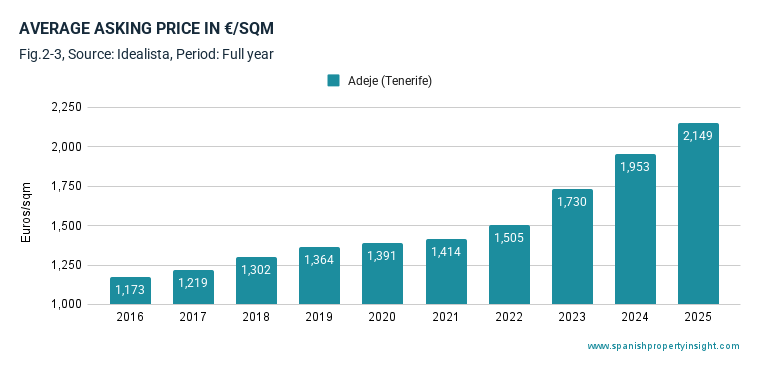

In the resale market, asking prices in Adeje averaged €2,149 per square metre in H1 2025, up 10% year‑on‑year (Fig. 2‑3). Over five years, asking prices have risen by 54.5%. The ten‑year index of asking prices reached 197, meaning prices have nearly doubled since H1 2015—a clear sign of long‑term price appreciation in one of the island’s most popular municipalities.

Lending rebounds strongly as borrowing costs ease

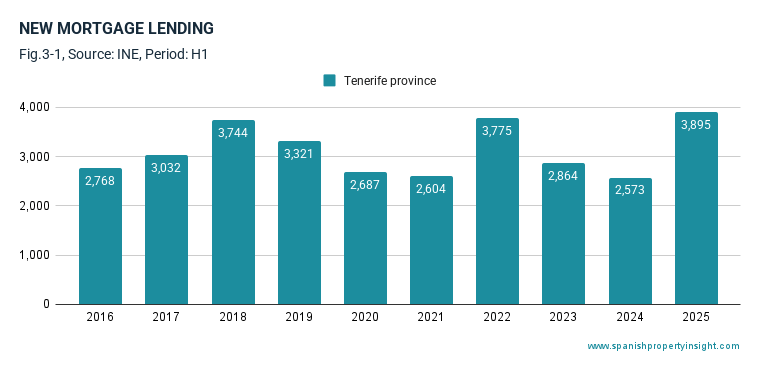

A total of 3,895 new mortgages were signed in the province of Tenerife during H1 2025, representing a year-on-year increase of 51.4% (Fig. 3‑1). This was 31.9% above the ten-year average and 81.5% higher than the volume recorded a decade earlier, indicating a strong recovery in credit activity.

The average Euribor rate during the period was 2.27% (Fig. 3‑2), marking a continued decline from the 2023 peak of 3.69%. This level is well above the historic low of -0.49% seen in 2021, but significantly below the highs of the past two years. The downward shift reflects the European Central Bank’s pivot to monetary easing, having begun cutting rates in early 2024 amid slowing inflation and weaker eurozone growth.

With inflation now broadly under control, markets expect the ECB to continue easing through the second half of 2025. As a result, borrowing conditions are likely to improve further, supporting both demand and affordability in the housing market.

Construction moderates but long-term growth remains strong

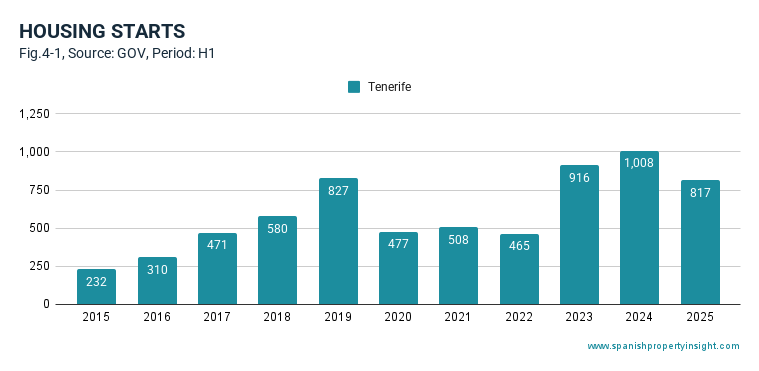

There were 817 new housing starts in H1 2025 based on planning approvals (Fig. 4-1), a decline of 18.9% compared to H1 2024. Despite this, the volume of new starts was still 41% above the ten-year average and more than 2.5 times higher than in H1 2015. While approvals have surged over the long term, the recent drop may constrain future supply if not reversed, particularly in areas of high demand.

Outlook and summary

The Tenerife province housing market in H1 2025 showed overall resilience, with sales volumes broadly stable and prices continuing to rise. However, the underlying dynamics reveal diverging trends: foreign demand—particularly among resident buyers—has weakened significantly, while domestic and new-build segments are gaining ground.

Strong growth in new-build sales and prices points to shifting buyer preferences towards higher-quality, energy-efficient homes, even as overall housing supply remains constrained. Lending activity has rebounded sharply thanks to falling interest rates, and further ECB rate cuts may provide additional stimulus in the second half of the year.

Despite a sharp fall in new planning approvals, long-term construction trends remain positive. If new supply fails to keep pace with recovering demand, upward pressure on prices could intensify—especially in sought-after areas like Adeje.

In summary, the market remains fundamentally strong but is undergoing a shift in composition. The outlook for H2 2025 will depend on the trajectory of foreign demand, the pace of interest rate cuts, and the ability of the supply side to respond to renewed buyer interest.

Previous reports

You can read reports from previous periods (if available) by clicking on the buttons below.

Tenerife’s property market performance in 2024.

The Tenerife housing market in 2024 displayed steady performance despite signs of shifting dynamics, with overall activity remaining resilient in the face of global economic uncertainties. While total transaction volumes held firm, foreign demand—particularly from non-residents and expats—saw a noticeable decline. Resale properties outperformed new builds in both pricing and demand, and key coastal areas continued to attract strong interest. Property prices rose overall, even as new-build values softened slightly. Despite elevated borrowing costs, the mortgage market remained active, and housing starts demonstrated long-term confidence from developers. This report outlines the key data and trends shaping Tenerife’s property market in 2024.

Sales performance

Tenerife recorded a total of 12,467 housing sales in 2024, virtually unchanged from the previous year, representing a year-on-year decrease of just 0.3% (Fig. 1-1). Compared to the ten-year average, transactions were 8% higher, and over the last decade, total sales volume has grown by 37%.

Foreign buyers were responsible for 4,770 of these transactions, a 9% drop from 2023. However, this segment remains slightly above its ten-year average and has grown by 17% over the decade (Fig. 1-2). These foreign transactions split into 2,038 purchases by resident foreigners (expats) and 2,732 by non-resident foreign nationals (FNRs). Expat purchases declined more sharply, by 15% year-on-year, while non-resident purchases fell by 5%. Over the long term, FNR activity has increased more rapidly, rising by 26% over ten years compared to 7% for expats.

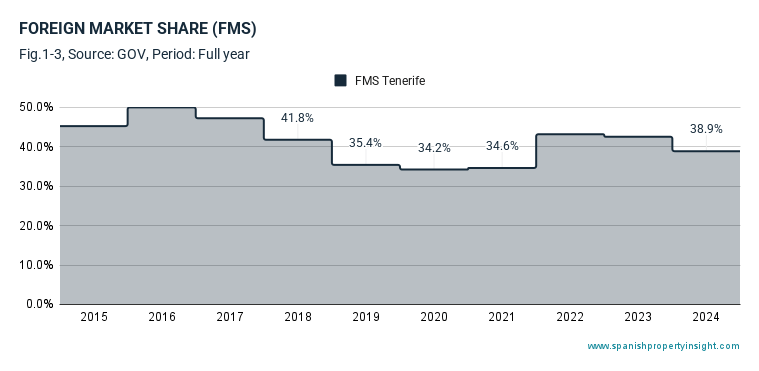

As a result, the foreign share of the local property market declined to 38.9%, down from 42.5% in the same period last year (Fig. 1-3). While still a significant portion of total demand, this marks a shift in the influence of overseas buyers on the market.

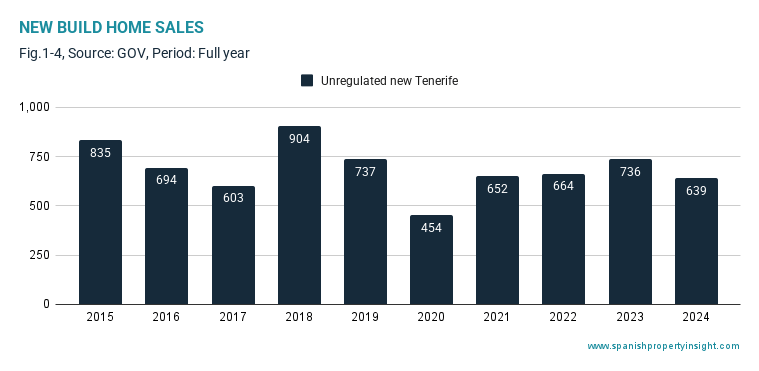

New build sales were also subdued, with 639 new homes changing hands in 2024—a 13% decline on the previous year (Fig. 1-4). This was 23% below the ten-year average, and 8% lower than a decade ago, underlining constrained supply and possibly waning buyer appetite for newly constructed properties.

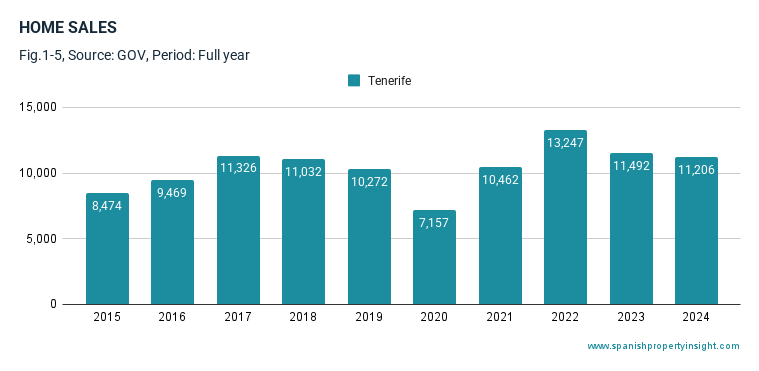

Within Tenerife’s municipalities, there were 11,206 transactions, reflecting a 2.5% drop from 2023 (Fig. 1-5). Compared to the ten-year average, however, this was an improvement of 8%, and total municipal sales have increased by 32% over ten years.

House price trends

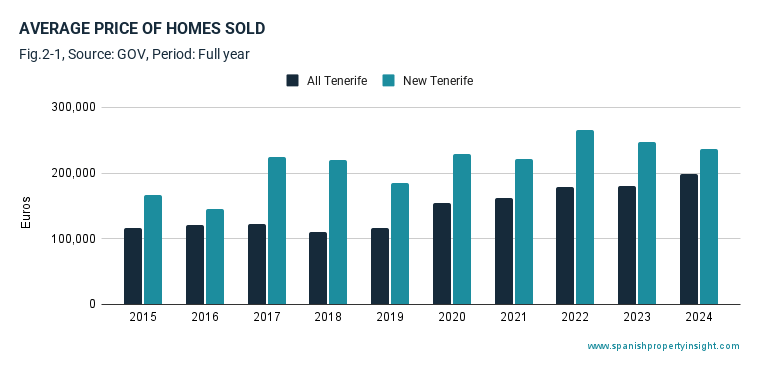

Official data from the Spanish Housing Ministry placed the average sale price of homes in Tenerife at €198,008 in 2024, up 10% from the previous year (Fig. 2-1). In contrast, the average price for newly-built properties was €235,928, down by 4% year-on-year.

These opposing trends are further highlighted by the ten-year price indices (Fig. 2-2). The index for all properties rose from 100 to 170.2 over the decade, a 70% increase, while the index specifically for new properties rose to 141.4—an increase of only 41%. This suggests resale properties have appreciated significantly more than new builds. A likely explanation is limited resale supply and rising demand in central or highly desirable areas, while new build stock is more affected by construction costs, delayed completions, and changing buyer preferences. Over five years, all property prices increased by 70%, compared to just 28% for new properties.

Adeje case study

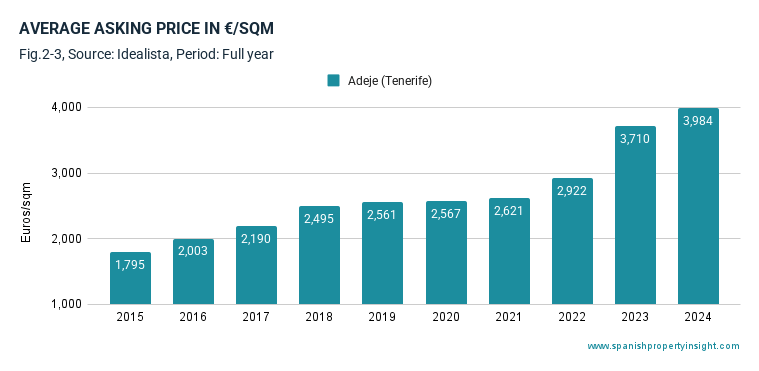

In the municipality of Adeje, one of the most desirable areas in Tenerife, the average asking price on property portal Idealista was €3,984/m² in 2024, representing a 7% annual increase (Fig. 2-3). Over five years, asking prices in Adeje have increased by 56%. A ten-year index of asking prices for this area rose from 100 to 221.9 (Fig. 2-5), implying asking prices more than doubled, growing by 122% over the decade—outpacing general transactional price growth, and highlighting the role of seller expectations, tourism-driven interest, and limited coastal supply.

Mortgage market

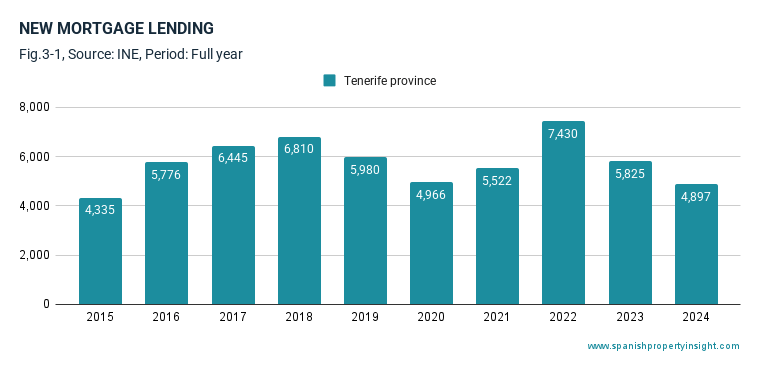

A total of 4,897 new mortgages were registered in Tenerife province in 2024 (Fig. 3-1), down 16% from the previous year. This figure is also 16% lower than the ten-year average, although volumes have still increased by 13% over the entire decade.

The average Euribor rate—used as a benchmark for most Spanish mortgage contracts—was 3.27% in 2024 (Fig. 3-2), falling from 3.86% in 2023, a 15% year-on-year decrease. This decline followed several years of aggressive interest rate hikes by the European Central Bank (ECB), aimed at curbing inflation.

Historically, the Euribor ranged from a low of -0.49% in 2021 to a high of 3.86% in 2023. The 2024 rate sits below this peak, suggesting the ECB may be nearing the end of its monetary tightening cycle. Market speculation in late 2024 pointed toward potential rate cuts in 2025, though persistent inflation and global uncertainty have led to cautious optimism rather than a sharp reversal in policy.

Housing starts

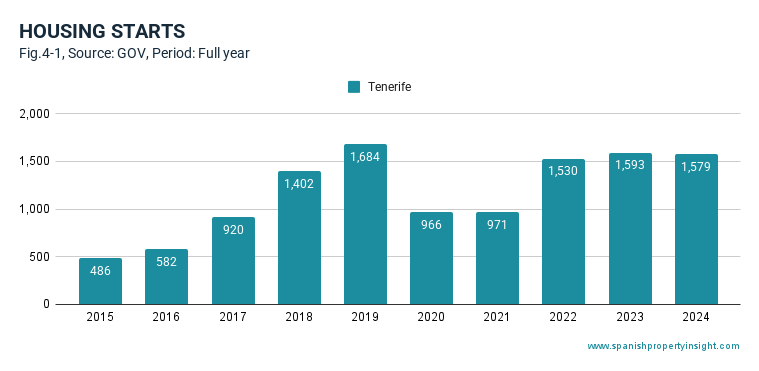

There were 1,579 new housing starts in Tenerife based on planning approvals during 2024 (Fig. 4-1). This number was in line with the previous year—just under 1% lower—and represents a 35% increase compared to the ten-year average. Over the last ten years, housing starts have risen by 225%, highlighting renewed construction activity from a previously low base.

This growth aligns with stronger long-term demand and investor confidence post-pandemic. However, the dip from last year may reflect rising construction costs, tighter lending, or permitting delays within certain municipalities.

Summary

- Total sales were steady year-on-year, but up 37% over ten years.

- Foreign demand dropped 9% and now represents 39% of total buyers.

- New build sales declined 13% and remain below average long-term volumes.

- Average house prices rose 10%, while new home prices fell 4%.

- Asking prices in Adeje increased 7% year-on-year and have more than doubled over ten years.

- New mortgage signings fell 16% amid high interest rates and tighter credit conditions.

- Euribor declined slightly from its peak, suggesting the start of a downward trend.

- Housing starts remain strong, with activity well above the long-term average.

Conclusion

Tenerife’s housing market in 2024 showed mixed signals. While overall transaction volumes and prices generally held up, there was a significant cooling in foreign demand, new build sales, and mortgage activity. Sellers continue to show price ambition, particularly in premium locations like Adeje, though actual price growth is easing outside of the resale sector.

Looking ahead, any further decline in interest rates could offer some relief to buyers and boost mortgage activity, especially among foreign investors and primary homeowners. Supply dynamics, tourism trends, and the global financial backdrop will all play crucial roles in shaping the market direction through 2025.