The Madrid housing market in 2025

Sales

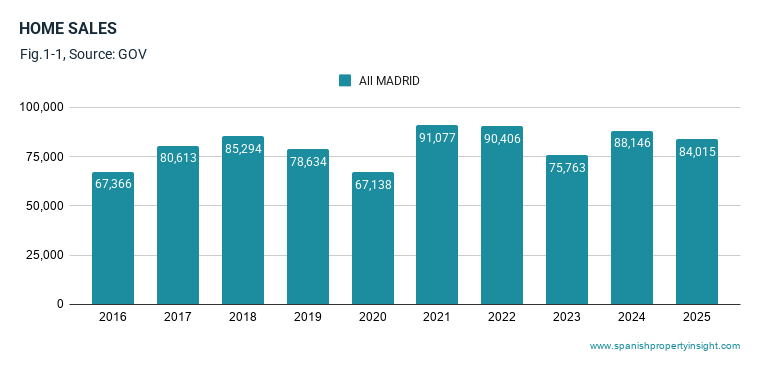

There were 84,015 home sales in the Madrid region in 2025, down 5% year-on-year. Even so, sales remained 7% above the ten-year average and were 46% higher than ten years earlier, suggesting that activity cooled from recent levels but stayed firm in longer-term context, as illustrated in Fig. 1-1.

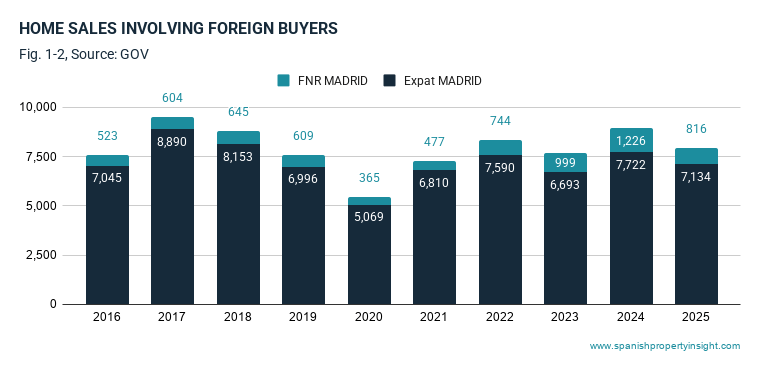

There were 7,950 home sales involving foreign buyers, down 11% year-on-year. These purchases were split between 7,134 expats living in Spain and 816 foreign non-residents buying second homes and investments. Expat demand fell by 8% over the year, while FNR demand dropped by a much steeper 33%. Over ten years, however, expat purchases were up 21% and FNR purchases were up 71%, showing that the long-term trend in foreign demand remains positive despite a weaker year in 2025, as shown in Fig. 1-2.

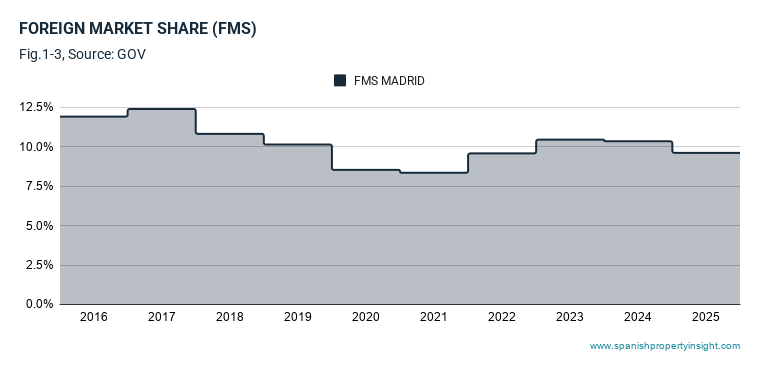

Foreign buyers accounted for just under 10% of the market in 2025, down slightly from just over 10% a year earlier. That underlines that foreign demand is meaningful in Madrid, but far less dominant than in many coastal or island markets, with domestic demand still providing the main support for activity, as illustrated in Fig. 1-3.

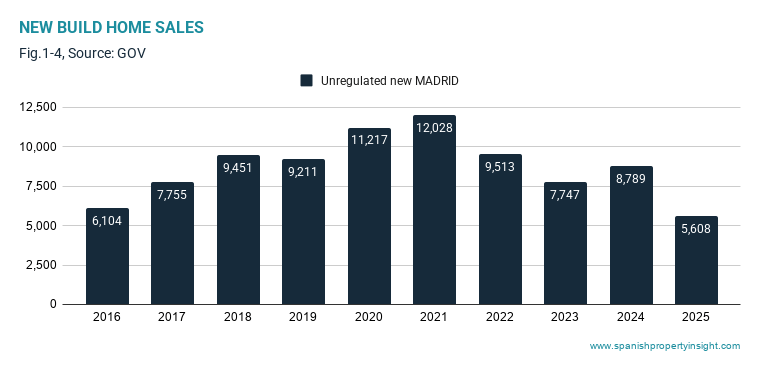

There were 5,608 new-build home sales in Madrid in 2025, a sharp decline of 36% year-on-year. New-build sales were also 36% below the ten-year average, though still 7% higher than ten years earlier. This points to a relatively weak year for new homes after a stronger earlier phase, as shown in Fig. 1-4.

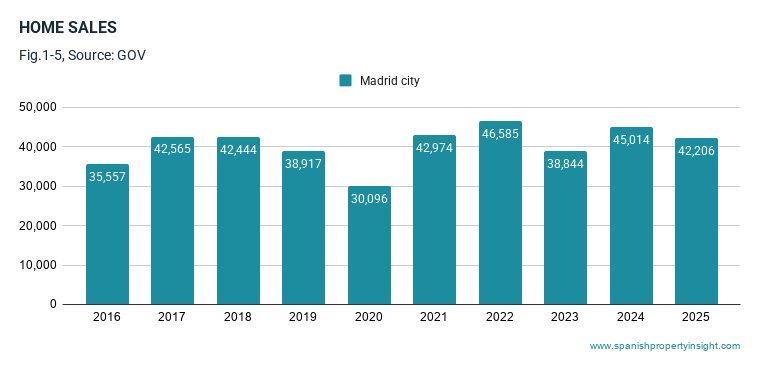

Looking just at sales in Madrid city there were 42,206 home sales in 2025, down 6% year-on-year. Even so, activity remained 4% above the ten-year average and was 19% higher than ten years earlier, indicating that although the city market softened in the latest year it still sits comfortably above longer-term norms, as illustrated in Fig. 1-5.

Prices

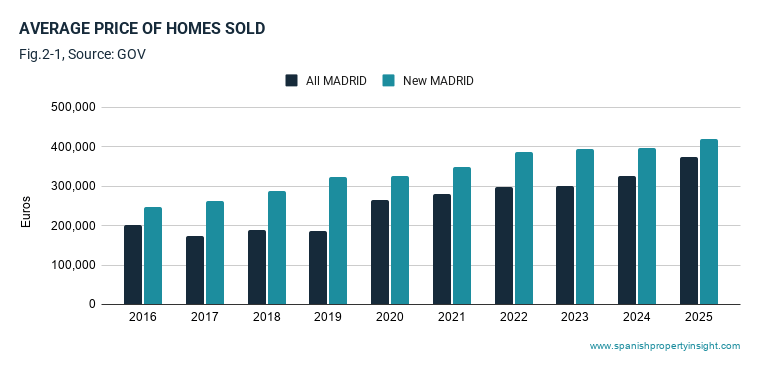

According to figures from the Spanish Housing Ministry, the average price of homes sold in the Madrid region in 2025 was €374,990, up 15% year-on-year. The average price of newly-built homes sold was €419,079, up 6%. So prices rose strongly overall, with the broader market outperforming new homes in annual growth terms, as shown in Fig. 2-1.

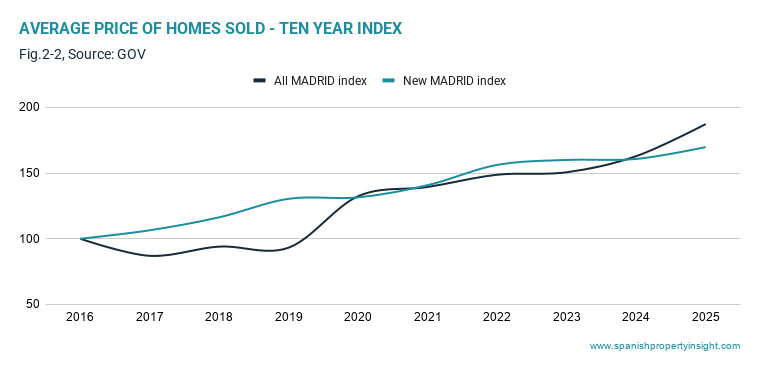

Madrid’s ten-year price index has risen from 100 to 187 for all homes and to 170 for new homes. In other words, average prices for all homes have increased by 87% over the decade, compared with 70% for new homes. Over five years, the increase was 41% for all homes and 29% for new homes. This suggests that the resale market has appreciated more strongly than the new-build segment, likely reflecting the scarcity of established housing in prime urban locations, strong demand for well-located existing stock, and the fact that much of Madrid’s new supply is more limited and unevenly distributed. Construction costs and land constraints have supported new-build prices too, but not enough to match the stronger gains in the wider market, as illustrated in Fig. 2-2.

Mortgages and financing conditions

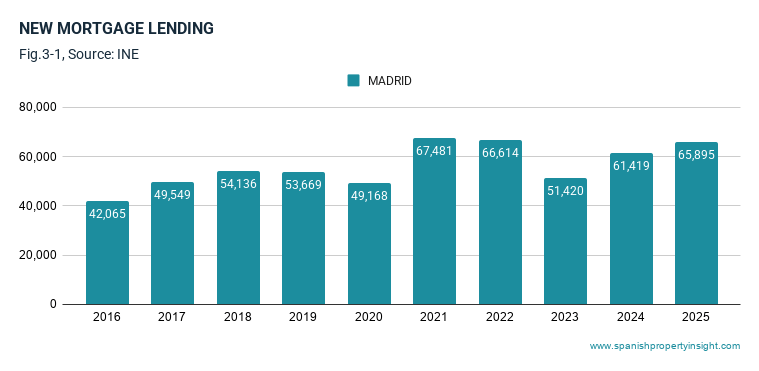

There were 65,895 new mortgages signed in Madrid the region in 2025, up 7% year-on-year. Mortgage activity was 24% above the ten-year average and 85% higher than ten years earlier, indicating a financing market that remained supportive despite the previous interest-rate tightening cycle, as shown in Fig. 3-1.

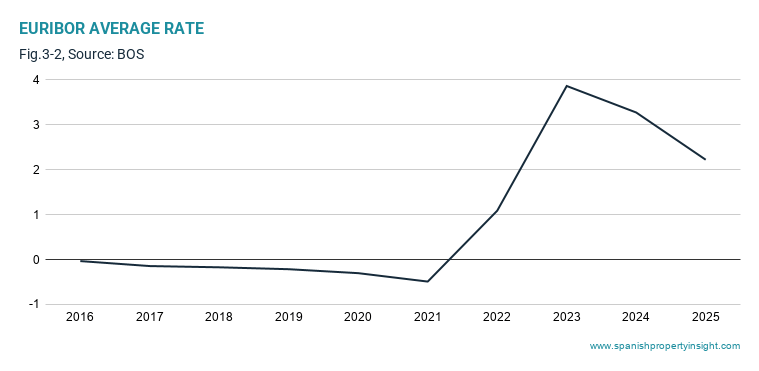

Average Euribor in 2025 was 2.22%, down 32% year-on-year. That placed it well below the recent peak of 3.86% in 2023 but still far above the low of -0.49% in 2021. Borrowing conditions therefore improved meaningfully from the highs of the tightening cycle, though they remained less favourable than in the ultra-low-rate period. The ECB cut rates in March and June 2025, taking its deposit facility rate to 2.00%, and then held rates steady through the rest of 2025 and again in March 2026. As of early April 2026, markets had shifted from expecting stability to pricing in possible further tightening later in 2026, reflecting renewed inflation concerns. As illustrated in Fig. 3-2, that means financing conditions improved during the period under review, but the direction ahead has become less certain.

Housing starts

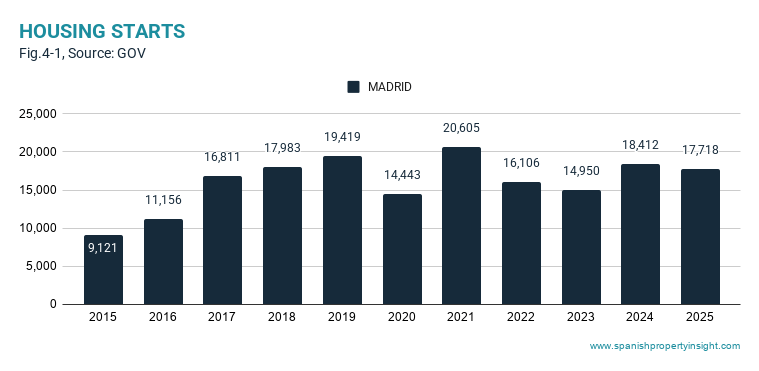

There were 17,718 housing starts based on planning approvals in the Madrid region in 2025, down 4% year-on-year. Even so, starts were 11% above the ten-year average and 94% higher than ten years earlier. That suggests new residential development remains elevated in historical terms, even after a modest annual decline, as shown in Fig. 4-1.

Summary

The Madrid housing market in 2025 showed mixed signals. Overall regional sales declined modestly and foreign demand weakened, particularly among foreign non-resident buyers, while new-build transactions dropped sharply compared with the previous year. Within the region, the Madrid city market also softened, with sales falling year-on-year, though activity remained above the long-term average and significantly higher than a decade earlier. Prices continued to rise strongly, especially in the resale market, highlighting the persistent imbalance between supply and demand in established urban areas. Mortgage lending expanded as financing conditions improved from the highs of the recent interest-rate cycle, while construction activity remained historically elevated despite a small annual decline. Looking ahead, the market’s trajectory will depend on financing conditions, the resilience of domestic demand, and the extent to which new supply coming through the pipeline can alleviate structural shortages in the capital.