Las Palmas housing market update – H1/First half of 2025

Covering the islands of Gran Canaria, Fuerteventura and Lanzarote

Sales remain steady overall, but foreign demand dips again

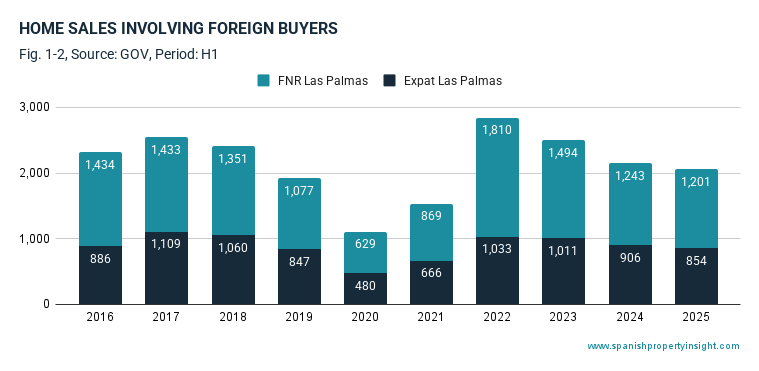

There were 7,260 home sales in Las Palmas province during the first half of 2025 (Fig. 1‑1), broadly in line with the ten-year average, and just 1.8% higher. Over the full ten-year period, sales have grown by 15.8%, confirming the long-term strength of demand in this province of the Canary Islands. However, the pace of foreign demand has slowed. There were 2,055 sales involving buyers from abroad in H1 2025, down 4.4% year-on-year (Fig. 1‑2), with the largest drop coming from expat buyers already resident in Spain (‑5.7%), compared to a smaller fall in foreign non-resident (FNR) buyers (‑3.4%). FNRs—typically second-home and investment buyers—accounted for 1,201 purchases, while expats made 854.

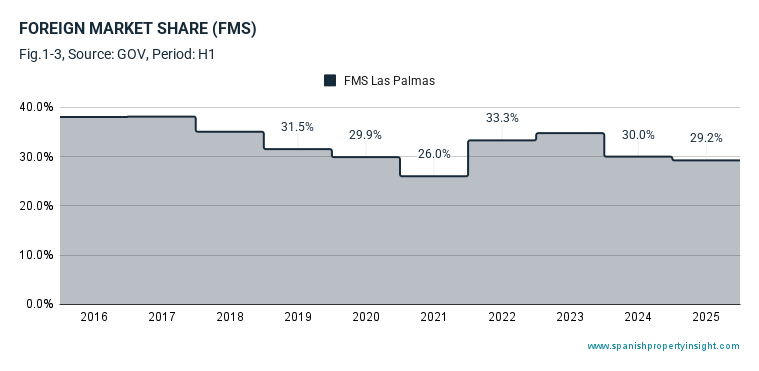

The foreign-buyer share of the market stood at 29.2% (Fig. 1‑3), slightly down on last year and a noticeable drop from the post-pandemic highs of 2022.

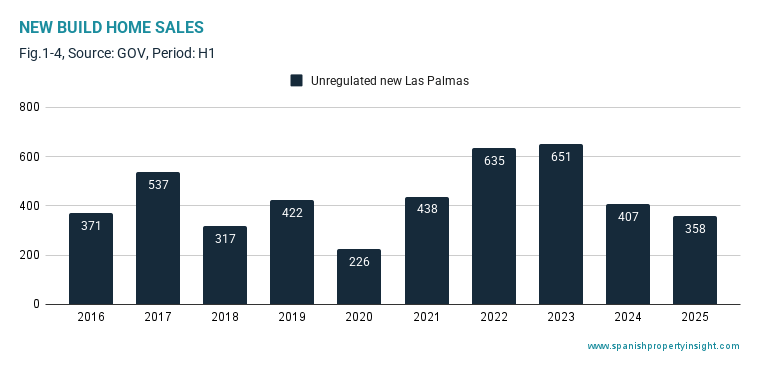

New home sales also softened, falling by 12% year-on-year to 358 transactions (Fig. 1‑4), now more than 21% below the ten-year average and 34% lower than in 2015.

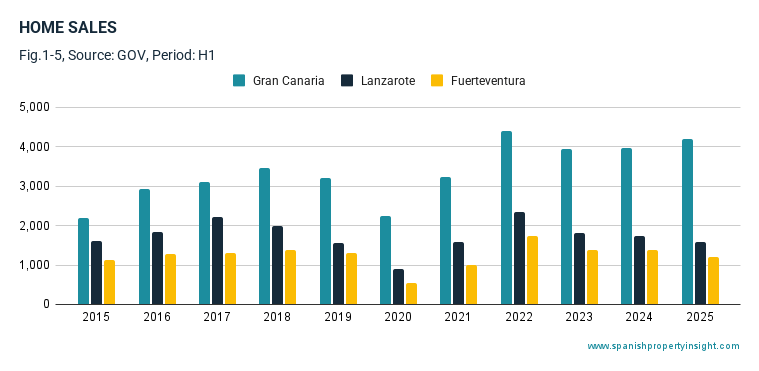

Sales patterns varied by island (Fig. 1‑5). Gran Canaria accounted for the largest share of provincial sales at 55.2%, with 4,189 transactions—up 5.5% year-on-year and 42.9% higher than in 2015. In contrast, Lanzarote (1,584 sales, 25.4% share) and Fuerteventura (1,195 sales, 19.4%) both saw declines. Lanzarote sales were down 8.4% year-on-year and 14.1% below 2015 levels, while Fuerteventura experienced a double-digit fall of 13%, with a 6.6% decline over ten years. These trends suggest a maturing market in the eastern islands, while Gran Canaria maintains a steady growth trajectory.

Prices climb across the board, led by Gran Canaria

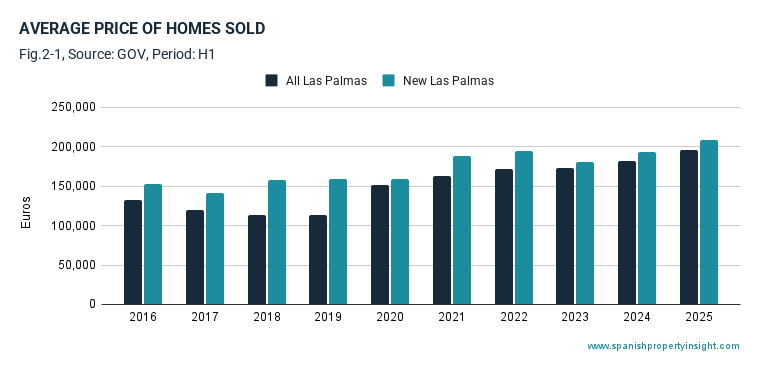

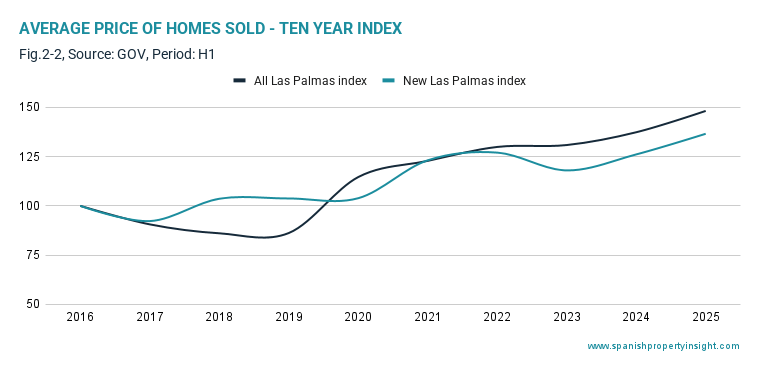

The average price of homes sold in Las Palmas during H1 2025 was €195,786 (Fig. 2‑1), up 7.9% year-on-year. New-build homes averaged €208,705, rising 8.3%. Over the last decade, general house prices in the province have increased by 48.2%, while new-build prices have risen 36.6% (Fig. 2‑2). This suggests that resale homes have gained relatively more in value, possibly due to tight supply and growing demand in established locations.

Looking at individual islands, Gran Canaria continues to lead on price growth. In Mogán, one of its most sought-after coastal municipalities, asking prices rose by 19.1% in the past year and 58.4% over ten years (Fig. 2‑3). Puerto del Rosario in Fuerteventura saw more moderate price growth of 8.6% year-on-year but a dramatic ten-year increase of 140.9%, likely reflecting catch-up from previously low levels. Teguise in Lanzarote recorded the most subdued performance, with a 4.1% increase over the year and 36.9% over a decade. In the past five years, asking prices have risen by 54.7% in Mogán, 68.5% in Puerto del Rosario, and 28.7% in Teguise.

Mortgage activity recovers modestly, but rates still weigh

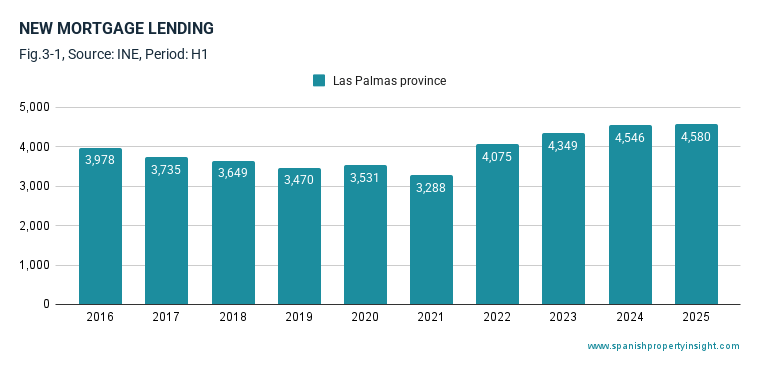

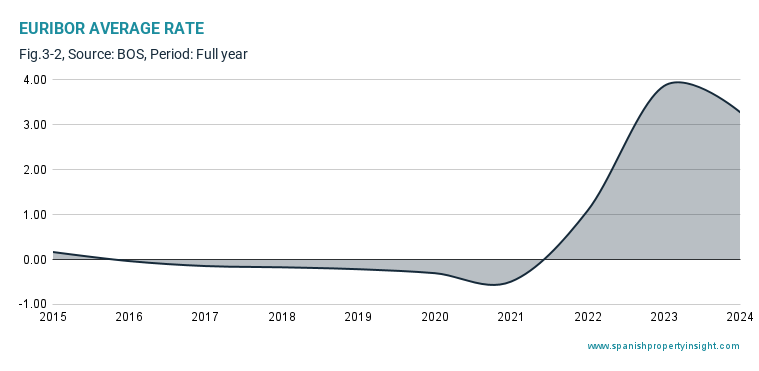

There were 4,580 new mortgages signed in the province during H1 2025 (Fig. 3‑1), up 0.7% year-on-year and more than 40% higher than ten years ago, reflecting the long-term expansion of credit in the market. Compared to the ten-year average, activity was up 20.9%. The average Euribor rate during the period was 2.27% (Fig. 3‑2), well below the peak of 3.69% seen in 2023, but a steep increase from the record low of ‑0.49% in 2021.

Despite the recent decline, Euribor remains elevated compared to the 2015–2021 period. The ECB began easing interest rates in early 2025, responding to cooling inflation, and further cuts are expected in the coming quarters. This could bring renewed tailwinds to mortgage lending and purchasing power in the islands.

Housing starts surge after prolonged drought

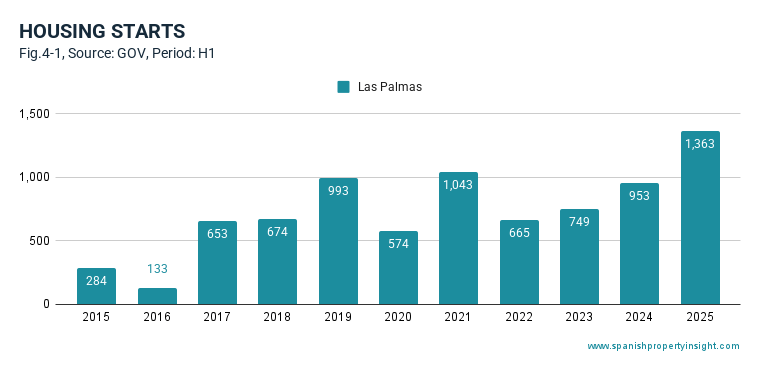

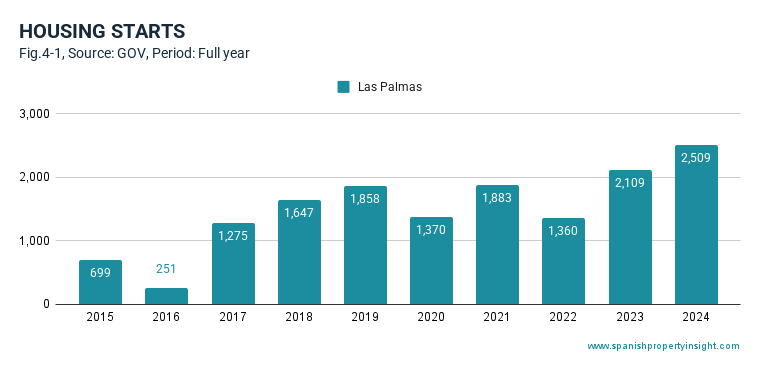

There were 1,363 new housing starts in the province based on planning approvals (Fig. 4‑1), a remarkable 43% increase year-on-year. Starts were more than double the ten-year average and nearly four times higher than in 2015. This jump marks a potential shift in future supply after years of underbuilding and tight inventory. Whether this momentum continues will depend on local planning conditions, developer confidence, and sustained demand—especially from international buyers.

Conclusion: Long-term strength, short-term shifts

The Las Palmas property market remains fundamentally robust, supported by strong long-term growth in sales and prices—especially in Gran Canaria. However, recent trends point to a cooling of foreign demand, particularly from expat buyers, and a dip in sales volumes in Lanzarote and Fuerteventura. Mortgage activity is stabilising, helped by falling interest rates, while the recent surge in housing starts suggests a potential improvement in supply after years of constraint.

Looking ahead, the combination of lower borrowing costs, increased new-build activity, and enduring international appeal—especially in Gran Canaria—should support the market. Even so, continued weakness in foreign demand and affordability challenges in some areas may temper growth in the short term. The next few quarters will show whether the rebound in development and the easing of monetary policy can translate into renewed momentum across all three islands.

Previous reports

You can read reports from previous periods (if available) by clicking on the buttons below.

Gran Canaria’s property market performance in 2024.

The Gran Canaria property market in 2024 showed solid performance, driven by strong local demand and steady overall sales. While international buyer activity declined—especially among non-residents—domestic transactions grew, particularly across key municipalities. Resale properties led the market in both volume and price growth, while new-build sales slowed. Mortgage activity eased under higher interest rates, though a slight drop in the Euribor and expectations of softer ECB policy improved the outlook. Meanwhile, construction remained active, with a strong rise in planning approvals. This report offers a concise analysis of market trends across sales, prices, mortgages, and new developments in Gran Canaria during 2024.

Sales performance

The housing market in Gran Canaria experienced modest overall growth in 2024, with notable variance between market segments and buyer profiles.

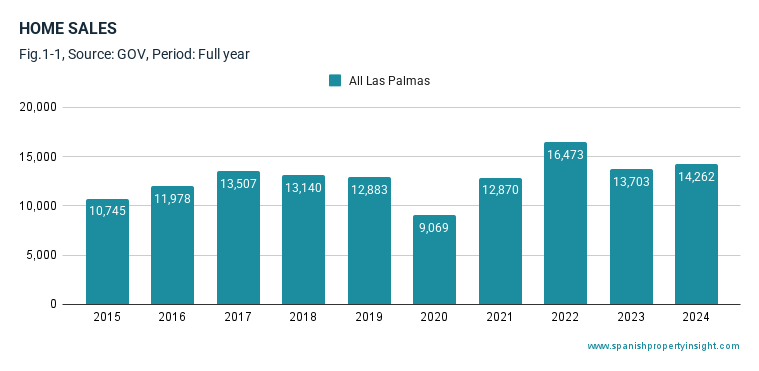

A total of 14,262 homes were sold, representing a year-on-year increase of 4% (Fig. 1-1). This was 11% above the ten-year average and 33% higher than sales levels a decade ago, indicating a steady long-term recovery.

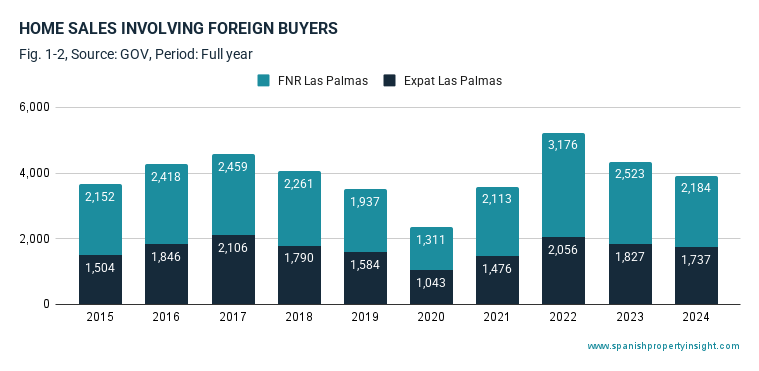

Sales involving foreign buyers amounted to 3,921 transactions, a decrease of 10% on the previous year (Fig. 1-2). This was just below the ten-year average (down 1%) but still 7% above figures from ten years ago.

- Of these, 1,737 homes were bought by foreign residents (expats), a fall of 5% year-on-year.

- Non-resident foreign buyers (FNRs)—often purchasing second homes or investment properties—accounted for 2,184 units, declining by 13% from the previous year.

Over ten years, expat purchases increased by 15%, while FNR transactions rose by only 1%, suggesting a shift in demand towards primary residence purchases.

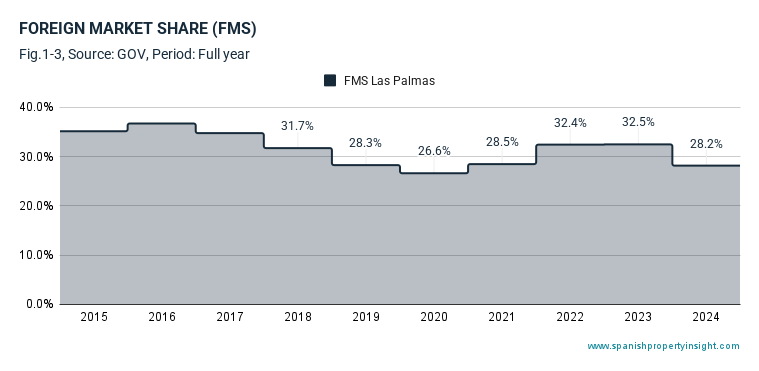

Foreigners made up 28% of the total buyer market share (Fig. 1-3), down from 32% the previous year. This drop reflects both weakening international demand and relative resilience in domestic activity.

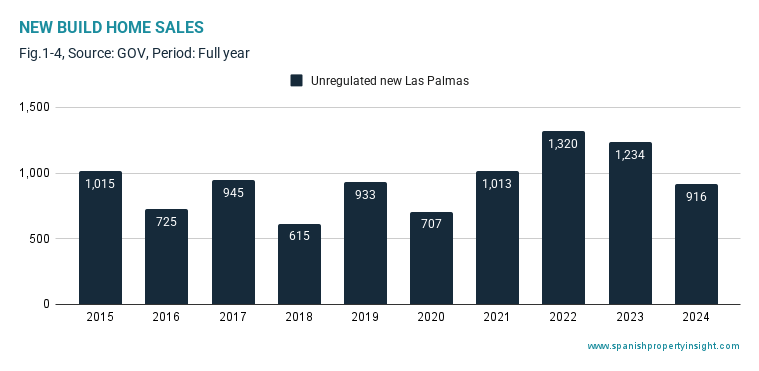

There were 916 newly built properties sold in the year, which amounted to a sharp 26% decline annually (Fig. 1-4). This figure was 10% below the ten-year average and 3% lower than a decade earlier, highlighting a soft patch in demand for new developments.

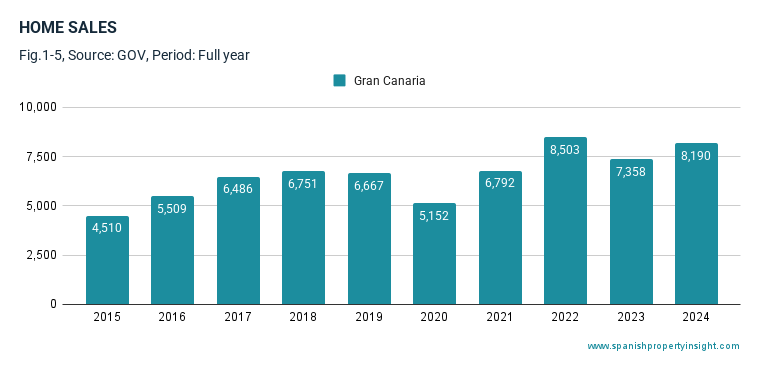

Within the island, Gran Canaria’s municipalities recorded 8,190 home sales, reflecting a strong year-on-year growth of 11% (Fig. 1-5). This segment significantly outperformed other areas, standing 24% higher than the ten-year average and 82% greater than the total sales recorded a decade earlier.

In summary, while internal demand and local municipal markets remain buoyant, foreign demand weakened and new-build transactions lagged behind.

House price trends

Property prices in Gran Canaria and the wider Las Palmas province maintained an upward trajectory in 2024, although the pace of growth was more subdued compared to previous years.

During the period, the average sale price for all residential properties in Las Palmas was €181,496, marking a 5% increase compared to the previous year (Fig. 2-1). In contrast, newly built homes recorded a slightly higher average price of €182,099, but with limited growth of just 1% year-on-year. This suggests a stabilisation in new-build pricing, possibly due to more balanced supply and demand in that segment.

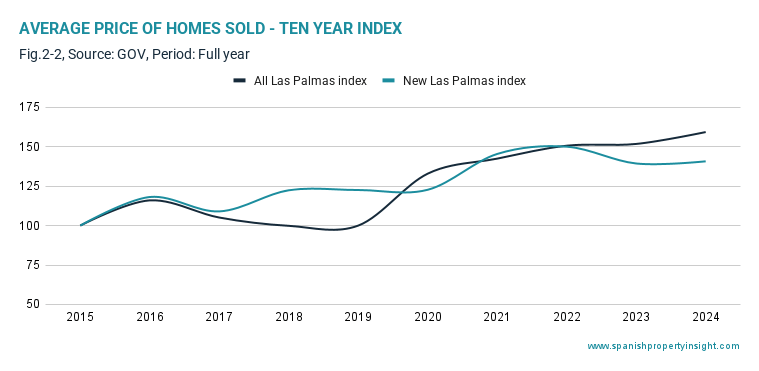

According to a property price index that uses 2014 as a base year (index = 100), prices for all property types have risen to 159 by 2024 (Fig. 2-2), representing a 59% increase over the past decade. In comparison, the index for new-build properties climbed to 141, indicating a 41% rise during the same timeframe. This divergence highlights that resale properties have appreciated more significantly than new homes, likely reflecting stronger demand for established locations or limited availability of quality existing stock.

This divergence suggests that resale properties have outpaced new-build values over the decade. This may be due to growing scarcity of well-located existing homes, stronger resale demand, or slower evolution in buyer preferences for newer inventory. Over the last five years, resale home prices have risen by 59%, while new-build increases have been far more subdued at only 15%.

Mogán case study

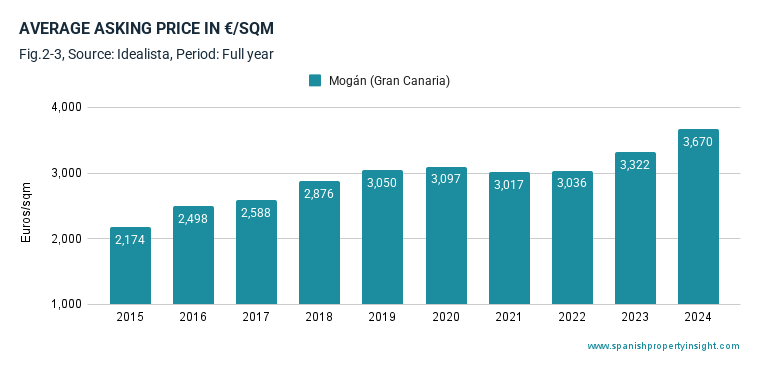

In the island’s popular coastal municipality of Mogán, average asking prices hit €3,670 per square metre in 2024, with a 10% year-on-year increase (Fig. 2-3). Over five years, asking prices have grown by 20%, consolidating Mogán’s position as a sought-after location.

The long-term trend of seller expectations in Mogán is reflected in the ten-year asking price index, which rose from 100 to 169. This 69% rise illustrates increasing confidence among owners and developers in the area’s future value.

Mortgage market

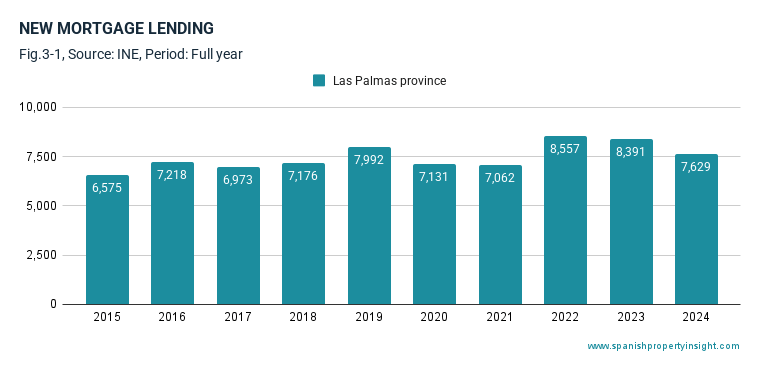

New mortgage activity declined moderately during 2024. Las Palmas province registered 7,629 new mortgages, down 9% on an annual basis (Fig. 3-1). Despite the recent dip, lending levels were still 2% above the ten-year average and 16% higher than in 2014.

The average Euribor rate, the benchmark for most variable-rate mortgages in Spain, stood at 3.27% for the period (Fig. 3-2). This compares with a high of 3.86% in 2023 and a low of -0.49% in 2021. The figure represents a notable decline and points to a potential shift in interest rate trends across the eurozone.

Following the European Central Bank’s tightening policy cycle between 2022 and early 2023, market expectations now foresee stabilisation or even rate cuts in the near term due to easing inflation pressures. Lower rates could eventually support buyer affordability and encourage increased borrowing.

Housing starts

Housing starts experienced strong growth in 2024. There were 2,509 new construction projects approved (Fig. 4-1), reflecting a 19% increase year-on-year.

Compared with the ten-year average, this represents a significant 68% rise, and activity has expanded nearly 259% over the past decade. These figures suggest renewed momentum in development after years of subdued output, as developers respond to sustained housing demand, particularly in urban and coastal zones.

Summary

- Total home sales rose by 4% year-on-year, driven by domestic demand and strong municipal performance.

- Foreign sales dropped by 10%, with FNRs seeing the steepest decline.

- Foreign market share fell to 28%, down from 32% in 2023.

- New-build sales declined sharply by 26%.

- Prices for all homes increased by 5%; new-builds rose marginally by 1%.

- Over ten years, resale home prices have risen faster than their new-build counterparts (59% vs. 41%).

- Euribor fell to 3.27%, following the previous year’s high, with market expectations pointing towards rate cuts.

- New mortgage volumes fell by 9%, despite being higher than the ten-year average.

- Housing starts surged by 19%, continuing a robust recovery in new construction.

Conclusion

Gran Canaria’s property market in 2024 demonstrated stable growth overall, despite headwinds from declining foreign demand and a contraction in new-build purchases. Domestic activity remains solid, particularly in key municipalities. Long-term price trends favour resale homes, while the mortgage market may benefit from falling interest rates as the European Central Bank shifts policy direction.

With housing starts on the rise, the market is poised for further development. However, success will rely on aligning new construction with buyer needs and economic trends. The outlook for 2025 remains cautiously optimistic, underpinned by improving affordability and sustained demand in core locations.