The latest data for Q3 2025 confirms what earlier quarters already suggested: Barcelona’s rent controls have coincided with a steep contraction in rental supply, while doing little to ease real market pressure.

With figures now available for the first nine months of 2025 (9M 2025), we now have a clearer picture of how the policy introduced in Q1 2024 is playing out. The results are underwhelming at best.

Declared rents broadly flat

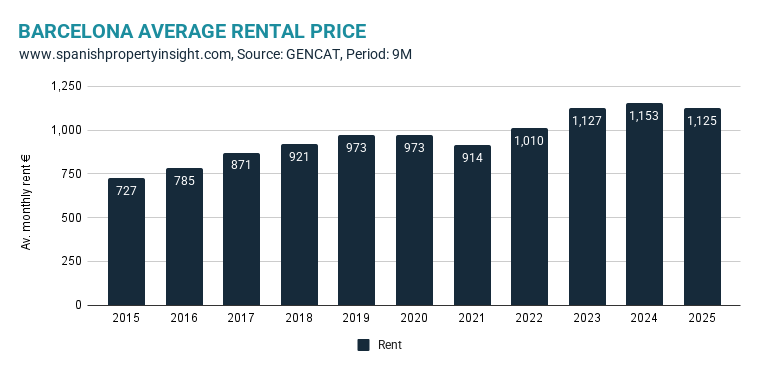

According to INCASOL—the Catalan government agency that registers rental deposits and therefore records actual contract rents—the average rent paid in Barcelona in 9M 2025 was €1,125.30, down 2.4% year-on-year (see chart above).

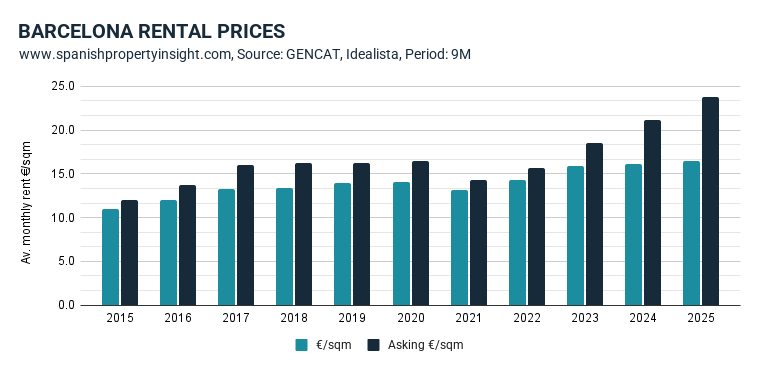

In €/sqm terms, rents were €16.53, up 2.35% compared to the same period last year. Over ten years, contract rents per square metre are up 51% in nominal terms, though the real (inflation-adjusted) increase is closer to 27%.

Since rent controls were introduced in Q1 2024, the average rent in euros has fallen by a modest 3%. However, the price in €/sqm has actually increased by around 1%, reflecting a decline in the size and quality of flats coming onto the market. In simple terms, tenants may be paying slightly less in absolute terms, but they are getting less for their money.

That is a far cry from a structural improvement in affordability.

Asking prices continue to surge

While declared contract rents have been broadly stable, asking prices tell a very different story. According to Idealista, average asking rents rose from €21.18/sqm to €23.73/sqm over the year—an increase of more than 12%. Since rent controls were introduced, asking prices are up roughly 13%.

Over ten years, asking prices are up almost 97% in nominal terms.

The widening gap between declared contract rents and open-market asking prices is now impossible to ignore. When official prices are flat but market prices are surging, it strongly suggests that the published data no longer captures the full economic reality. A growing black economy—where part of the rent is paid in cash and never declared—becomes an increasingly plausible explanation.

Supply collapse: the real story

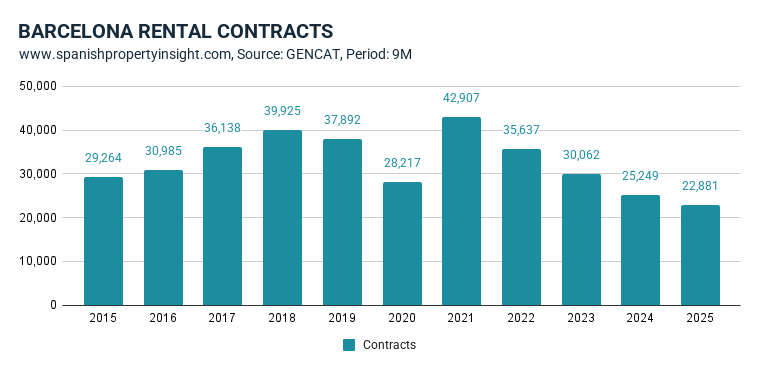

The most striking figure in the 9M 2025 data is not the rent level. It is the number of contracts.

Just 22,881 rental contracts were signed in the first nine months of 2025. That’s down 9.4% year-on-year and almost 25% below the ten-year average. Compared to the long-term norm, 10,746 fewer families found a home to rent this year.

Since Q1 2024, the number of rental contracts signed has fallen by roughly 20%. Compared to the 2021 peak of 42,907 contracts in the same period, we are now almost 50% lower.

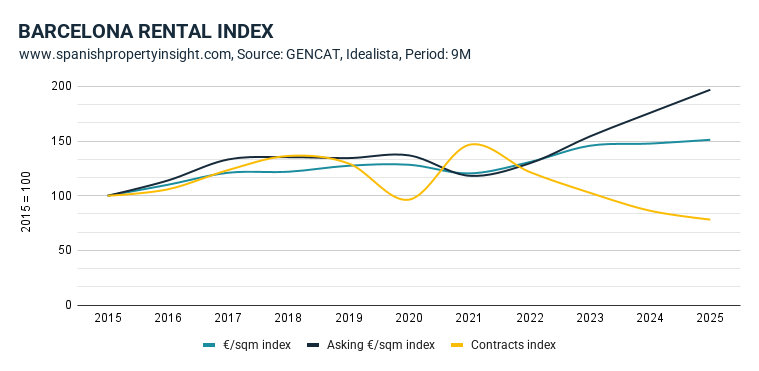

Using 2015 as a base year (100), the divergence is stark:

- €/sqm contract rent index: 151

- Asking price index: 197

- Contracts signed index: 78

All three were broadly aligned in 2022, after the pandemic dip and the suspension of the previous rent control experiment. Since then, rents and supply have diverged dramatically.

This is precisely what economic theory predicts. Rent controls limit supply. They do not eliminate demand.

Who wins and who loses?

The beneficiaries are clear: sitting tenants and applicants with impeccable profiles who manage to secure one of the increasingly scarce regulated contracts.

The losers are equally clear: younger households, migrants, the self-employed, and anyone without a “perfect” income profile. When landlords are forced to rent below market rates, they become more selective, not less. Risk tolerance falls. Access narrows.

Politicians may celebrate a modest 3% decline in headline rents. But when tenants are paying roughly the same per square metre for smaller, lower-quality flats, and thousands fewer homes are available, it is hard to call that a success.

Spin versus substance

Supporters of rent controls will point to “price containment” as proof that the policy is working. But price stability achieved through supply destruction is not a housing solution—it is a housing rationing system.

Nine months into 2025, there are no big wins to boast of—only marginal nominal price restraint alongside a steep contraction in available housing and a surge in asking prices. The benefits are concentrated among the lucky few. The costs are borne by the many who can no longer find a home.

The bottom line is simple. Rent controls in Barcelona have not solved the housing crisis. They have reshaped it—making the market smaller, more opaque, and less accessible. And as the gap between asking and declared rents widens, the suspicion grows that the official figures are telling only half the story.