Eurozone mortgage base rates in March spent a second consecutive month in negative territory and uncharted water, though borrowers are unlikely to enjoy much benefit from negative interest rates (and savers certainly won’t). Where is this leading, and what does it mean for investing in real assets like Spanish property? (short answer, I don’t know).

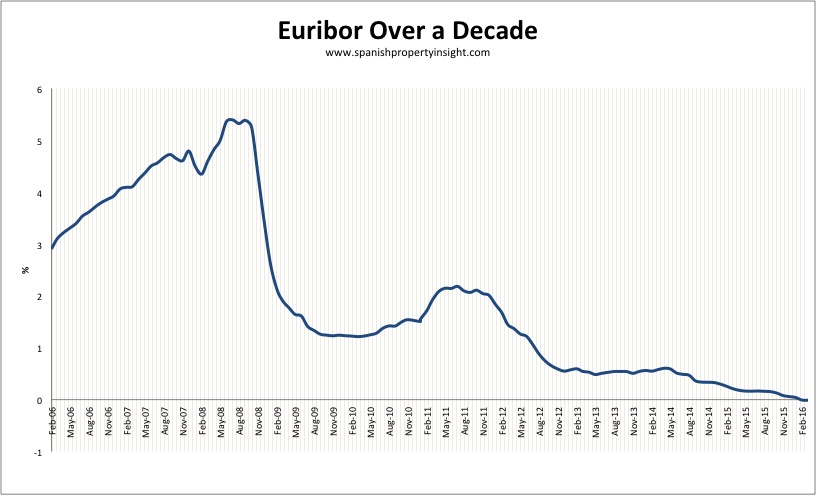

12-month Euribor – the rate used to calculate most mortgage repayments in Spain – came in at -0.013 in March, down from -0.008% in February, meaning another month of negative Euribor interest rates.

Nobody really knows where this leads in the medium to long-term, but in the short term it should mean that existing borrowers with an annually resetting mortgage (and no floor clauses) will see their mortgage payments fall by around €12 per month for a typical €120,000 loan with a 20 year term.

As I have no idea where this policy is taking us all I can do is repeat what I wrote last month, quoting Ambrose Evans-Pritchard (AEP), International Business Editor editor at the Daily Telegraph, who described the situation as “grotesque….devastating for banks….a calamitous misadventure”. He talked to José María Roldán, head of the Spanish Banking Association, who said “It’s not healthy, it’s not sustainable, it’s mad.” Go figure.

Euribor has been below 1% since June 2012, but Euro interest rates were not always so low. Back in July 2008 they peaked at 5.393%, and in the decades before Spain joined the Euro, interest rates above 10% were common.

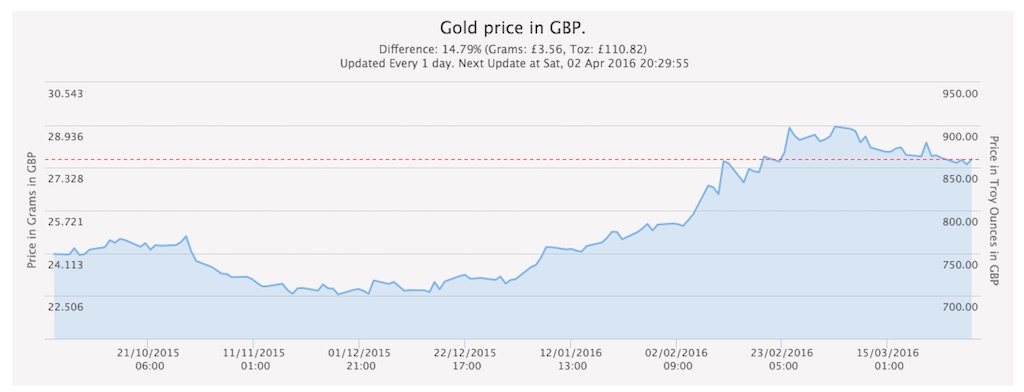

With negative interest rates resulting from quantitative easing (QE) on a mind-boggling scale, how likely is it that paper-money will retain its value over the longer term? I’m sceptical, and I see the price of gold has been creeping up (see below). Perhaps prime property in Spain bought cheap today (prices have bottomed out after seven years on the slide), with a 20-year fixed mortgage around 3% isn’t such a bad idea. At least it’s inflation proof, and has utility value.