Spain’s property meltdown offers once-in-a-cycle investing opportunities through bank repossessions. The following beefed-up article from 2007, by legal expert Raymundo Larraín Nesbitt, offers a complete legal overview.

By Raymundo Larraín Nesbitt

Lawyer – Abogado

21st of February 2014

The amount of home repossessions in Spain has soared to unprecedented levels according to the latest figures of the Bank of Spain. Conservative sources estimate the figure in well over 250,000 repossessions since the real estate market collapsed in 2007. The real number may actually be higher. This tidal wave has in turn spawned and exacerbated other phenomena such a new breed of middle-class squatters in Spain.

The Government, in denial mode, claims it has been overwhelmed and even caught off guard on the wake of recent social events. I beg to differ. Any industry insider would have told you at the time a sharp rise in repossessions was taken for granted for all the reasons collated below.

Underlying Causes of the Bank Repossession Crisis in Spain

The causes underpinning this surge in home repossessions are mainly related to the economic ‘recession’ Spain wades seven years on:

1. High levels of unemployment reminiscent of the Great Depression (an eye-watering 28% and counting) leading to widespread mortgage delinquencies. That is six million people unemployed. 1.8mn families in Spain have all their members unemployed. National youth unemployment (under 25-year-olds) is a staggering 55% and in some communities exceeds well over 60%. This quadruples the world’s average and doubles the European rate. These statistics, a human drama hiding behind each one, eerily echo harsh times straight out of a novel by John Steinbeck. Source: INE (National Institute for Statistics).

2. Aggressive reform in Labour laws which made dismissals less cumbersome and onerous overall. Spanish politicians pursue a ruthless internal devaluation at any cost to regain international competitiveness which translates into severe wage cuts. Less monthly disposable income edge Spanish families closer to the brink.

3. Unparalleled levels of lax lending. Bordering non-existent in the case of Spanish savings banks (‘cajas de ahorros’). Basically anyone with a pulse qualified for a mortgage loan.

4. Irresponsible property overvaluation led by bank-appointed appraisal companies.

5. Reckless over-indebtedness. Families should never spend more than 30% of their disposable income on servicing a mortgage loan.

6. Rising inflation. Traditionally offset by leading monetary institutions by increasing the price of money; that is by increasing the applicable interest rates.

7. Euribor rate poised to increase. It is used as a benchmark index in over 95% of variable interest Spanish mortgage loans reaching an all-time high in 2008. This means mortgage borrowers face the grim prospect of increased monthly repayments.

8. Relentless fall in property prices (on average 50% across the board) have discouraged potential purchasers, who postpone buying expecting even steeper discounts further down the line. Asset depreciation likewise affects existing property owners who find it hard to borrow against their properties unlocking equity through equity release schemes or life-time loans in Spain.

9. Severe credit shortage. The lowest on record on a fifty-year period aggravated by creeping interest rates and Spain’s uncertain financial health. In addition, bad credit for banks stands at a stunning 13%. The former helps to explain, amid other reasons I won‘t delve into, why Spanish lenders are reluctant to lend (unless at exorbitant borrowing costs which act as a deterrent grinding the market into a standstill). Credit is the real estate market’s lifeblood. If this is sapped away it creates huge imbalances. This effectively translates into scores of struggling borrowers being unable to offload a glut of properties in fire sales as keen would-be buyers are themselves turned down by tight-fisted lenders on applying for mortgage loans in a vicious gridlock that eventually drives the former to being repossessed. Mortgage borrowing costs in Spain are now at an all-time high. Cash is king.

10. Additionally, and specifically in the case of non-residents, the strengthening of the Euro against other currencies such as the Sterling Pound or the US Dollar makes it harder for these currency holders to face their monthly mortgage repayments in Euros.

Definition of Negative Equity

A significant fall in property value translates into borrowers no longer being interested in servicing their mortgages as they have run into what’s known as ‘negative equity’ (they owe a lender more than what the property is worth).

How Can One Run into Negative Equity?

This takes place when the asset, or collateral, guaranteeing a mortgage loan is worth less than the loan amount itself.

Although this may seem difficult at first, the truth is that running into negative equity is surprisingly easy in Spain. In the following sections I explain how one attains negative equity:

i) steep drop in property price

ii) post-auction (repo) property

The reason why in nine out of ten public auctions in Spain no-one bids, besides the ongoing credit-crunch, is precisely negative equity. That is what’s keeping professional bidders at bay in such properties. Not all bank repos are a bargain, some are tripe; beware the hype. One should cherry pick them carefully assisted by a professional worth his salt (reputable estate agent, seasoned lawyer, expert investor).

I. Sharp Drop in Spanish Property Prices

The bank, on deciding if they will grant you a loan, will command an appraisal of the property on issuing a Binding Offer (‘oferta vinculante’). The property will act as collateral of the loan. If the value is unrealistic and is above the current market value of the property, should there be a fall in house prices, then a property may be worth less than the loan it is guaranteeing. This is the current scenario.

All mortgage contracts in Spain have a clause by which if the value of the property falls below 20% of the appraisal value the bank may request at their own discretion additional collateral to offset the financial shortage. In practice banks seldom opt to enforce it but they could legally.

In the event a lender seizes a property, it can auction it off publicly.

II. Public Auctions Mean a Further Drop in Property Price

As the influx of repossessed properties increases in the near future banks will eventually be forced to go through a public auction. In these auctions, should no-one bid, a lender is legally entitled to seize the property for 60% of its appraisal value. This has been recently increased by Law 1/2013 as before it was 50% which left the borrower in an even more precarious state.

Additionally, as I explain in detail further below, the extent of the liability is unlimited and personal. Meaning the lender will actually pursue the borrower for the outstanding unpaid amount (i.e. up to 40% plus associated repossession expenses).

This is precisely why overvaluing properties has turned out to be so harmful. Bloated appraisals have lead trustful borrowers to reel in shock as it dawns on them that the money fetched in a public auction falls well below the amount owed to their lender. On top of this you must also add the legal fees of the bank’s lawyers and the associated costs of a full-blown repossession procedure.

This is simply an injustice. As not only does a borrower stand to lose his property in an auction but must also withstand the additional aggravation of putting up with a lender that will relentlessly pursue him for the unpaid amount as the property value does not suffice to cover the loan amount plus mounting compound interests and associated repossession expenses. The debt will grow over time exponentially creating a debt spiral if left unchecked. This will turn many Spanish families into becoming lifetime financial pariahs; social outcasts with no hope of redemption.

Banks can legally pursue you abroad for a shortfall. Another matter is if it is worth their while.

Wait a Moment. I Have Already Paid X% of the Mortgage Capital During the Equivalent Period of Time!

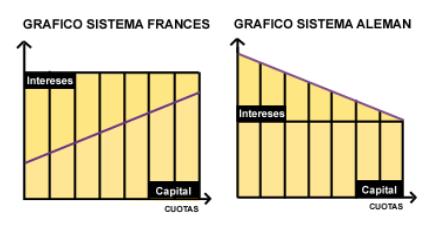

Well, I’m afraid you haven’t! If your mortgage uses the French repayment method (as most of the mortgages granted in Spain do) then you will only have paid a small fraction of the mortgage capital upfront. The reason is that with the French system you pay interest-only during the early stages of a mortgage, as it gradually shifts to capital-only following a lineal sliding scale. This method is devised to allow that monthly payments terms remain fixed and equal throughout the duration of a mortgage.

To put it simply, during the first years of a mortgage you pay interest mostly. So if you default on the first years of a mortgage you practically have all the capital still outstanding to be paid off.

Extent of Liability

Following article 1911 of the Spanish Civil Code on signing a mortgage deed you will be held liable with all your current and future assets. This translates to unlimited personal liability. The debt goes personally against you, not against the property. The mortgage is only a guarantee subject to the financial loan with the property, or underlying asset, acting as collateral.

The above has huge legal implications which borrowers ought to fully understand before signing a Spanish mortgage deed. This means that if you default on servicing your Spanish mortgage, a lender may seize the property acting as collateral. If you fall into negative equity a lender is additionally entitled to pursue you abroad, even in your home country, for the shortfall. This may lead to a debt spiral – a very sticky situation.

Unlike in the UK and the US, most of the time handing back the keys to a lender will not stop them chasing you for the outstanding debt. This can only be achieved through a formal legal procedure known as ‘dación en pago’ which I care to explain further below.

Five Useful Tips to Avoid Repossession if you cannot Service your Mortgage

If you are struggling to meet your monthly mortgage repayments you should not wait until you have slipped into arrears to start negotiating with your lender. If you foresee falling into arrears, pre-empt the situation by requesting from your lender a debt restructure. After three months of mortgage arrears Spanish banks start to take legal action and initiate repossession proceedings.

Pre-repossession negotiations with a lender may include, but are not limited to, all the following:

1. Extend the mortgage repayments a number of years. The longer the duration, the less you stand to pay a month. The caveat is that you will end up paying considerably more in the long run due to the ‘magic’ of compound interest.

2. Reduce the interest rate or move on to an interest-only mortgage (‘carencia’) for a few years on the hope your economic circumstances will improve over time.

3. Apply for debt consolidation. This immediately reduces your monthly outgoings

4. Swap your mortgage to a new lender with less onerous conditions.

5. Attempt a property fire sale as a distressed asset (offering it at a steep discount).

If a borrower has unsuccessfully pursued any or all the above-listed debt restructuring options, he may consider handing over the keys to a lender only as an option of last resort. In doing this a borrower will avoid the dire consequences of a repossessions procedure; namely still being chased years after for a shortfall in the mortgage loan post-auction as outlined above. This is carried out following an ad hoc legal procedure, explained in the next section, rather than just allowing a lender to unilaterally repossess a property.

Do All Properties End in Repossession?

Not all properties end in a public auction, especially in those few cases in which a borrower is not in negative equity. Those who have slipped into mortgage arrears may strike with their lenders an out-of-court-settlement which basically entails handing back the keys following a legal procedure. This is known as ‘dación en pago’ in Spanish.

This involves signing a deed at a Notary Public relinquishing ownership and in exchange a lender fully discharges a borrower of the remaining mortgage debt, not holding you liable in the future. The catch is that the property must not be in negative equity. This procedure is loosely modelled after article 140 of Spain’s Mortgage Act.

The whole point of following a dación would be to avoid repossession at all costs.

Sadly, as described in my updated article, ‘dación en pago finally a borrower’s right’, lenders no longer offer this option freely.

The Six Stages of a Bank Repossession

A repossession procedure generally follows in 6 steps:

1. The borrower falls into arrears – The borrower fails to service his mortgage repayments. Delay interests (‘intereses de mora’) accrue to cover penalties. The lender contacts the borrower and first attempts an out-of-court settlement.

2. In technical default – Three months from the first arrear (Law 1/2013). After 3 months in arrears a client’s file is passed onto the bank’s legal debt collection department which tries in a last-ditch effort to recover the debt. A lender will then initiate an Executive Procedure against the encumbered property filing it before a local ‘first court’ where the property is located. The bank is then forced to set aside a provision to offset the potential loss. This mandatory provision helps on to explain why lenders are open to negotiate before a default because these must be deposited before the Bank of Spain which undermines lenders’ liquidity ratios. Banks, with the ongoing current credit-crunch, will go to great lengths to avert this as it effectively hampers their own borrowing ability in the money markets. And credit is eventually shut to them leading to unpopular government bail outs.

3. Foreclosure and notary intervention – Depending on the chances of a debt recovery, 15 to 20 days after the technical default. A registered letter is sent by a Notary Public, with acknowledgement of receipt, informing a borrower that a repossession procedure is underway.

4. Repossession order – The court contacts the property owner to pencil a date for the trial. The judge notifies the borrower of impending repossession proceedings. The judge requests from the Land Registry a full report of charges and liens against the property. The value of the asset in the public auction can be either the one that is lodged at the Land Registry in the Mortgage deed or else the bank may command an updated appraisal. This updated appraisal will also be useful for the bank to decide on whether it is worthwhile or not to proceed with the repossession as this has high associated expenses. I must point out that a borrower may still successfully halt repossession at any time before the pencilled date for the auction so long as he pays the outstanding amount plus the full associated repossession expenses (easily over £8,000). These funds (outstanding monthly repayments with accrued delay interests plus the full associated repossession expenses) will have to be lodged both before the court that is ruling on the Executive Procedure before the date set for the auction. So time is of the essence.

5. The court sets a date for the public auction – Normally between 6 to 12 months after initiating the Executive Procedure. The judge sets the date of the auction. The value for auction purposes cannot fall below 75% of the appraisal value. However if no-one bids the gavel falls and a lender is legally entitled to seize the property for 60% of its appraisal value. The bank tries to recoup the outstanding loan debt instigating a public auction. However, post-repossession, after the property has been assigned to a winning bidder or to the lender; the amount fetched may not be high enough to cover the debt plus all the associated repossession expenses (i.e. because the borrower had run into negative equity). A lender will then be entitled to pursue the rest of the borrower’s assets, even if abroad, due to the personal and unlimited liability of a borrower ex art 1911 of the Spanish Civil Code. Should there be a guarantor on the mortgage deed the bank will chase their assets first it is easier to seize them. The property will now be lodged under the name of the new owner at the local Land Registry (normally the lender).

6. Eviction – In the event the now ex-owner still dwells in the property, after a period that normally spans six months, police officers will arrive at their door step with a locksmith and judicial bailiff to evict them by force, if necessary. There are a few instances in which delaying tactics may be employed albeit ultimately the outcome will be the same so it’s only buying time before the unavoidable.

Interested in Buying Repossession?

Repossessions offer great value for money. They are genuine unique investing opportunities as they have heavily built-in discounted prices for all the legal reasons explained above. Although repossessions offer the highest rewards to the undaunted they also have associated the highest risks. There is a clear correlation between risk and reward which a shrewd investor should ponder carefully in his decision-making before committing. The current market meltdown offers one-time buying opportunities that will likely take decades to be seen again. The timing is ideal for cash buyers who do not need to rely on a mortgage loan to acquire property. You will be spoilt for choice.

For more details read on my article on Buying Distressed Property in Spain which offers a detailed overview. It explains the different types of distressed asset classes, ranging from Non-Performing Mortgage Loans (pre-auction or key-ready properties) to Bank Repossessions (post-repossession properties) as well as the pros and cons of each. Repossessions are the real deal.

Spanish Bank Repossessions – Conclusion

Defaulting on a Spanish mortgage is a serious matter that may jeopardize your assets abroad as well as dealing a major blow to your credit rating score in your home country (hampering your future borrowing ability) as the debt will be against you personally and not against the asset itself.

Unlike in the UK, for example, in which we have a statute of limitations on debt after six years in Spain it works differently in practice. There is a statutory limitation of twenty-year years but it can be renewed at any given moment on the lender contacting a borrower to claim the principal plus compound interests accrued. Lawyers, acting on behalf of creditors, make sure to contact borrowers at regular intervals to avoid the limitation becoming firm. So in practice, never.

If everything else fails, the only option left is to try to negotiate with your lender. Lenders are open to renegotiate the lending terms providing you are not in arrears with them. Even borrowers saddled with debt should try to speak with their lender to find a way out. Lenders are reluctant to add yet another repossession to their books and so are keen to be flexible and accommodating.

To close I would like to imagine that lenders in general, and borrowers in particular, have learnt from the harsh lessons and in future cycles will avoid overstretching their finances saddling themselves with debt. Guessing it’s too much to ask for.

“Never was so much owed by so many to so few” – Sir Winston Churchill.

Eminent British career officer, artist, historian, and laureate writer – awarded the Nobel prize in Literature in 1953. Was even known to dabble in politics in his spare time; nobody’s perfect.

Related articles

- Lifetime Loans or Reverse Mortgages in Spain Explained – 21st February 2011

- Advice to Struggling Mortgage Borrowers in Spain – 8th March 2011

- Spanish Mortgage Loans: Beware of Abusive Clauses – 8th January 2012

- Spanish Mortgage Loans: An Overview – 21st February 2012

- Mortgage Collar Clauses Revisited (‘Cláusulas Suelo’) – 8th December 2013

- Bank Repossessions in Spain – 21st February 2014

- Bad Debtor’s List (‘Fichero de Morosos’) – 8th April 2014

- Spanish Creditors Pursuing Debts Abroad – 8th May 2014

- Dación en Pago Explained or How to Hand Back the Keys – 8th December 2014

Please note the information provided in this article is of general interest only and is not to be construed or intended as substitute for professional legal advice. This article may be posted freely in websites or other social media so long as the author is duly credited. Plagiarizing, whether in whole or in part, this article without crediting the author may result in criminal prosecution. VOV.

2007 and 2013 © Raymundo Larraín Nesbitt. All rights reserved.