At the beginning of the crisis the drama of repossessions was largely limited to immigrants and poorer sections of Spanish society. Now it’s biting deeper into the professional classes.

The risk of default amongst mortgage borrowers is rising in all sections of society, claims an association (AFES) set up to help people at risk of repossession. “There are now pilots and dentists who don’t know how they are going to pay the mortgage because they can’t make it to the end of the month,” says Carlos Baños, President of the association.

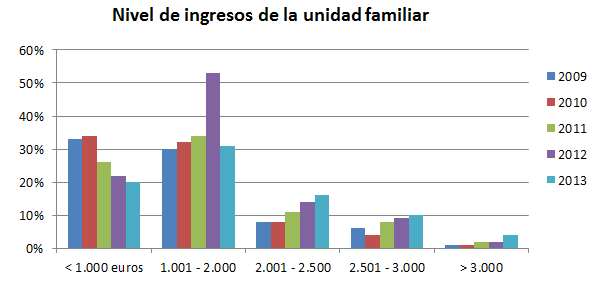

The chart above, prepared by AFES, illustrates how the default rate amongst borrowers earning less than 1,0000 €/month has steadily fallen, whilst rising amongst borrowers with an income of 2,000 €/month or more.

Unless banks take evasive measures now, more than 500,000 families will have defaulted on their mortgages and be at risk of social marginalisation by 2015, warn AFES. 150,000 families have already defaulted and lost their homes, but not their debts, claim AFES.

Since 2009 the number of Spaniards who can’t pay the mortgage has tripled whilst the number of immigrants in the same position has halved. Rising unemployment, now above 26pc, is the main cause of default, and is now as a much a problem for the professional classes as less educated sections of society. In past economic crises, the working class bore the brunt of the pain on their own, but this time the pain is being shared around more equally.

Nevertheless, higher earners are still a small percentage of defaulters, even if there are more of them in this crisis than in previous ones.

At the start of the crisis, 33pc of defaulters were mileuristas, as people who earn €1,000 per month or less are known in Spain. That percentage has now fallen, whilst the number of people earning more than €2,000 in default has risen substantially. Furthermore, 40pc of defaulters now come from better-educated sections of society.

A survey by AFES of 10,000 borrowers revealed that the average debt today stands at €232,000, way above average house prices that have tumbled in the crash. A lot of Spanish borrowers are now deep under water.

In Spain, personal liability mortgages are the norm in Spain. So when borrowers lose their homes, they are often left with debts that will take a lifetime (or more) to pay-off.

The following chart illustrates the principal reasons for default: Blue = unemployment, Red = too much debt, Green = Divorce, Purple = higher mortgage repayments. Rising unemployment is the killer.