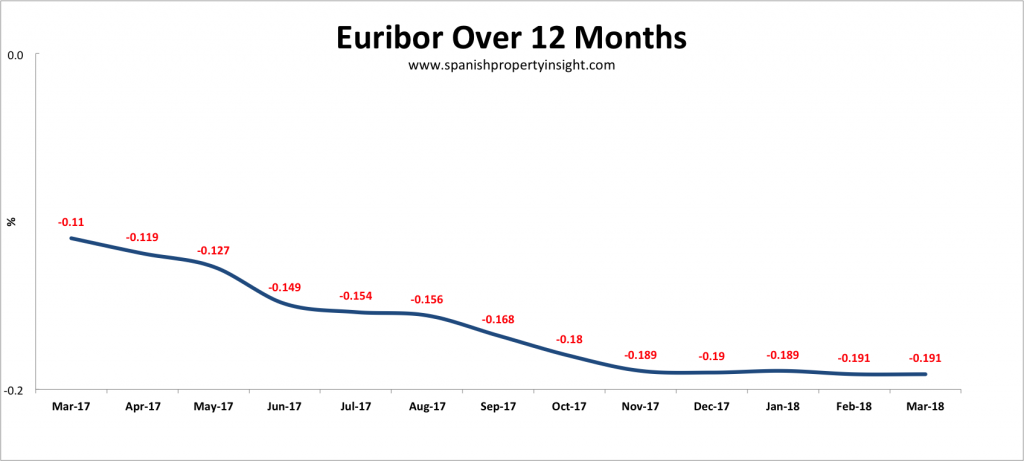

12-month Euribor, the base rate used for most mortgages in Spain, came in at -0.191 in March, unchanged from the month before, and 73.6% lower than the same month last year.

As a result, borrowers in Spain with annually resetting Spanish mortgages will see their mortgage payments fall by around €4 per month for a typical €120,000 loan with a 20 year term.

A brief upturn in 2011 notwithstanding, interest rates have been falling since October 2008, but it’s starting to look like the downward trend has flattened out. In the last four months Euribor has hardly declined at all.

After a decade of ultra-loose monetary policy around the world, central banks in the US and the UK are slowly starting to tighten, which will put pressure on the ECB to follow suit.

The next chart illustrates how interest rates in the Eurozone have fallen to historic lows, which suggests that money has never been this cheap to borrow. For those that can, it looks like a good time to take out a long-term, fixed-interest rate mortgage as money might never be this cheap again in our lifetimes, at least in nominal terms.

If interest rates, inflation, and Spanish property prices rise (as they are), buying a Spanish property today with a fixed-rate mortgage could turn out to be a sound investment.

Whether for investment purposes or otherwise, mortgage borrowing in Spain is rising rapidly, with new loans to home buyers up 14% in January, according to data from the Association of Spanish Notaries. Mortgage borrowing has risen by double digits almost every month for at least a year. The average new loan in January was €130,182, down 4.2% compared to last year.